Corporate Finance

Overview unavailable.

The Vernimmen Finance Legacy

- The text serves as a collection of high-level endorsements for 'Corporate Finance: Theory and Practice', commonly known as 'The Vernimmen'.

- Industry leaders from organizations like the World Bank and Apax Partners highlight the book's long-standing relevance across decades of their careers.

- The manual is praised for its unique ability to merge rigorous theoretical frameworks with practical, real-world applications and common-sense reasoning.

- Academic and professional experts emphasize the book's comprehensive coverage, ranging from basic financial analysis to complex M&A transactions.

- The authors maintain the book's relevance through a monthly newsletter and regular updates that reflect evolving market developments.

- The text is positioned as an essential 'bible' for a diverse audience, including students, investment bankers, and industrial chairmen.

The Vernimmen is a true bible of corporate finance. With regular updates through their monthly newsletter and upgrades, the authors have made it applicable to any place, any time.

Publication and Copyright Information

- This text represents the fourth edition of 'Corporate Finance: Theory and Practice' published in 2014 by John Wiley and Sons.

- The publisher asserts strict copyright protections under the UK Copyright, Designs and Patents Act 1988, prohibiting unauthorized reproduction.

- The book is available in multiple formats, including print, electronic, and print-on-demand, with some variations in supplemental media.

- A legal disclaimer clarifies that neither the publisher nor the authors provide professional services or warranties regarding the book's contents.

- The work is cataloged by both the Library of Congress and the British Library, identifying it as a comprehensive resource on business enterprise finance.

It is sold on the understanding that the publisher is not engaged in rendering professional services and neither the publisher nor the author shall be liable for damages arising herefrom.

Corporate Finance Foundations

- The text introduces a prestigious team of authors including Pascal Quiry, Maurizio Dallocchio, Yann Le Fur, and Antonio Salvi, all of whom bridge the gap between high-level academic finance and professional M&A practice.

- It honors the legacy of Pierre Vernimmen, a legendary dealmaker who advised on the creation of LVMH and authored the definitive French financial textbook that serves as the foundation for this work.

- The comprehensive table of contents outlines a structured journey from fundamental financial analysis and cash flow mechanics to complex market theories and investment rules.

- The curriculum covers the diverse landscape of financial securities, including bonds, shares, options, and hybrid products, emphasizing the calculation of risk and required rates of return.

- The final sections focus on strategic corporate policies such as capital structure, dividend practices, and advanced financial engineering including IPOs, LBOs, and mergers.

Pierre Vernimmen, who died in 1996, was both an M&A dealmaker (he advised Louis Vuitton on its merger with Moët Henessy to create LVMH, the world luxury goods leader) and a finance teacher at HEC Paris.

The Philosophy of Corporate Finance

- The book integrates financial analysis with strategic and economic evaluation as a prerequisite for valuation.

- The authors bridge the gap between academic theory and professional practice based on their experience in M&A and investment.

- A primary focus is placed on enduring conceptual frameworks rather than transient technical methods.

- Corporate financiers are described as intermediaries who market financial securities to investors and bankers.

- The text emphasizes a value-oriented mindset over a traditional focus on costs or earnings.

A good financial manager listens to customers and sells them good products at high prices.

The Return to Reason

- Financial analysis is re-emerging as the cornerstone of economic decision-making following periods of market euphoria.

- A firm's long-term survival depends strictly on its ability to remain solvent and create value for shareholders.

- The text outlines a rigorous framework for analysis including financial mechanics, accounting standards, and wealth generation.

- Section IV critiques the modern obsession with earnings per share and return on equity, which can distract from true value creation.

- The curriculum integrates theoretical concepts like agency theory and signal theory into practical corporate financial policies.

When share prices everywhere are rising, why stick to a rigorous approach? For one thing, to avoid being caught in the crash that inevitably follows.

Corporate Finance Learning Resources

- The book covers advanced corporate finance topics including mergers, LBOs, restructuring, and the intersection of finance and strategy.

- Pedagogical features include over 800 problems with solutions, a comprehensive index, and a one-page 'crib sheet' summarizing the entire 1000-page text.

- The companion website vernimmen.com offers free access to financial data for over 16,000 global companies and an Excel file with detailed problem solutions.

- Authors provide a direct communication channel via a letterbox, promising responses to reader questions within 72 hours.

- A free monthly newsletter supplements the text by analyzing topical financial problems, research papers, and current market statistics.

We’ve used the last page of the book to provide a crib sheet (the nearly 1000 pages of this book summarised on one page!).

Acknowledgements and Financial Symbols

- The authors express gratitude to a wide network of contributors, including academic peers, MBA students, and technical staff who refined the manuscript.

- A heartfelt dedication is made to the authors' families and friends for their patience during the long years of the book's production.

- The text transitions from personal acknowledgements to a comprehensive glossary of corporate finance abbreviations and symbols.

- The symbols list covers essential valuation metrics such as DCF, EBITDA, and NPV, alongside complex financial instruments like DECS and CVRs.

- The section establishes the book's dual purpose as both a foundational textbook for students and a reference guide for practicing professionals.

And last but not least to Françoise, Anne-Valérie, Enrica and Annalisa; our children Paul, Claire, Pierre, Philippe, Soazic, Solène and Aymeric and our many friends who have had to endure our endless absences over the last years.

The Role of Corporate Finance

- The financial manager serves as a vital intermediary between the real economy of goods and services and the complex world of financial markets.

- Traditional views define the financial manager as a buyer of capital focused on minimizing costs from bankers and shareholders.

- A modern perspective frames the financial manager as a seller of financial securities who aims to maximize their market value.

- The text distinguishes between the business manager, who handles operations and physical assets, and the financial manager, who manages capital supply.

- Corporate finance operates within a capital market economy where money is treated as the primary commodity for transaction.

The financial manager is at the crossroads of the real economy, with its industries and services, and the world of finance, with its various financial markets and structures.

The Financial Manager's Dual Role

- The traditional view defines the financial manager as a purchaser of capital whose primary goal is to minimize the cost of funds.

- This procurement role involves negotiating interest rates, value dates, and commissions with bankers and intermediaries.

- An alternative perspective frames the financial manager as a salesman who seeks to maximize the selling price of financial securities.

- In this 'salesman' model, the focus shifts from minimizing interest rates to maximizing the market value of the company's instruments.

- The capital market can be viewed symmetrically: the supply of securities equals the demand for capital, and vice versa.

- Ultimately, the equilibrium price in this market can be expressed either as the cost of funds or as the value of the security.

That said, let’s now take a look at the financial manager’s job from a different angle: he is not a buyer but a seller; his aim is not to reduce the cost of the raw material he buys but to maximise a selling price.

The Financial Manager as Salesman

- Interest rates and security values move in opposite directions, establishing a fundamental theorem that minimizing financing costs is synonymous with maximizing security value.

- Viewing the financial manager as a seller of securities shifts the focus toward understanding and satisfying the specific needs of capital suppliers.

- Financial markets are subject to trends and fashions, requiring managers to repackage financial products like convertible bonds or syndicated loans to meet current demand.

- Relying solely on the lowest cost of capital as a decision-making criterion is flawed because it ignores the varying risk levels faced by different investors.

- Short-sighted decisions, such as over-leveraging short-term debt or granting mortgages for minor rate decreases, can jeopardize a company's long-term survival.

- The phrase 'it doesn't cost anything' should be banished from corporate finance and replaced with an analysis of an action's impact on total value.

The most dangerous thing a financial manager can say is, “It doesn’t cost anything.”

The Essence of Financial Instruments

- A financial instrument is fundamentally a contract defined as a schedule of future cash flows executed over time.

- Holding a security represents the right to receive cash flows, while issuing one represents a commitment to pay them.

- The transition from paper documents to intangible book entries highlights that the core of finance is the underlying information and contract.

- Time is the critical element that introduces risk, as various external factors can disrupt promised payments regardless of a borrower's intent.

- Financial logic transforms physical goods and services into cash flows, allowing real assets like sugar or property to be traded as fungible financial instruments.

- Markets facilitate the negotiation between issuers seeking funds and investors seeking rights to future obligations.

Time, or the term of the financial security, introduces the notion of risk.

Defining Financial Instruments

- The distinction between a real asset and a financial asset often depends on the investor's motivation rather than the physical object.

- Financial securities are undifferentiated and can be held by many investors simultaneously, unlike unique physical assets like specific buildings.

- Mathematically, every financial instrument is defined as a series of future cash flows scheduled over a specific timeframe.

- Debt instruments represent a binding commitment from a borrower to repay a lender with interest.

- Loans transform into financial securities when they become negotiable and listed on secondary markets, such as bonds or commercial paper.

The distinction between a real asset and a financial asset is therefore subtle but fundamental.

Types of Financial Instruments

- Debt securities like commercial paper and treasury bills represent short-term loans where returns are contractually fixed or floating rather than profit-dependent.

- Equity securities represent capital contributions where investors bear industrial risk in exchange for profit shares and corporate voting rights.

- Limited liability structures protect shareholders by capping their potential losses at the amount of their initial investment.

- Hybrid securities created through financial engineering blur the lines between debt and equity to meet specific corporate and investor needs.

- Options represent a unique class of instruments that provide the holder with rights rather than obligations regarding future financial actions.

- Financial instruments exist on a broad spectrum ranging from strict commitments to flexible rights, all valued within the context of active markets.

Financial imagination knows no bounds. Keep in mind that these instruments are like the cherry on the top.

Primary and Secondary Markets

- A financial security exists independently of its issuer once launched, serving as a vehicle for various investor strategies.

- The primary market is the venue for 'newly-minted' securities where entities like corporations and governments raise fresh capital.

- The secondary market facilitates the trading of 'used' securities, allowing assets to change hands without creating new financial instruments.

- Liquidity is the defining feature of the secondary market, allowing investors to convert assets into cash quickly without significant price disruption.

- The secondary market is essential for long-term investments like equity, as it provides the only exit strategy for shareholders.

- While conceptually distinct, the two markets are functionally integrated, together balancing financing needs with available capital.

Once launched by its issuer, a financial security lives a life of its own.

Secondary and Derivative Markets

- Secondary markets operate independently of issuers, allowing investors to trade existing securities without affecting the company's capital formation statistics.

- The quality and liquidity of a secondary market directly dictate the success and pricing of the primary market for new securities.

- Financial managers must monitor secondary markets because they price the company's 'raw material' and facilitate the trading of voting rights and corporate control.

- Derivative markets, including futures and options, allow managers to hedge financial risks or take leveraged speculative positions with limited initial capital.

- The financial manager ultimately sells the management's reputation as the core value proposition behind any security issued.

Think about it: who would want to buy a financial security on the primary market, knowing that it will be difficult to sell it on the secondary market?

The Financial Manager's Mandate

- The financial manager's primary role is transforming industrial and commercial assets into financial instruments for diverse investor groups.

- A company's ability to distribute cash is strictly limited by its business operations; paying creditors or dividends without profit jeopardizes long-term health.

- Market perception acts as a real-time valuation of management quality, where poor performance leads to prohibitive yields and falling security prices.

- Investors are driven by expected rates of return rather than altruism, requiring the company to meet or exceed specific financial benchmarks.

- Value creation occurs only when investment returns exceed the cost of capital, while falling short leads to 'corporate purgatory' and value destruction.

- The financial manager must act as a strategic dealmaker, balancing the competing motivations and power dynamics of various capital providers.

If not, if the company is consistently falling short of this goal, it will destroy value, turning what was worth 100 into 90, or 80. This is corporate purgatory.

The Strategic Financial Manager

- The financial manager acts as a 'party-pooper' by rejecting projects that fail to meet profitability thresholds.

- A core responsibility is ensuring the company's assets generate a rate of return equal to or greater than investor requirements.

- Financial managers must act as strategists, recommending the sale of underperforming units to reallocate capital to efficient divisions.

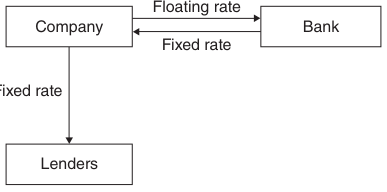

- Modern financial management requires mitigating external risks such as interest rate fluctuations and currency volatility.

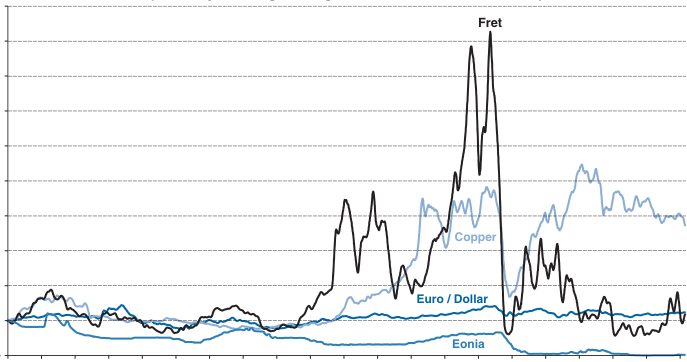

- Global operations create a 'multi-headed dragon' of risk where commodity prices and exchange rates dictate performance.

Its performance depends not only on the price of copper but also on the exchange rate of the US dollar vs. the Swiss franc, because it uses the dollar to make purchases abroad and receives payment in dollars for international sales.

The Evolving Role of CFOs

- Managing interest rate and exchange rate risks is essential as inaction can lead to severe financial consequences.

- Derivative markets allow treasurers to manage long-term risk efficiently without inflating the company balance sheet.

- The modern CFO has transitioned from a traditional accountant to a strategic leader skilled in marketing, negotiation, and risk management.

- Former CFOs are increasingly becoming top candidates for CEO positions at major global corporations like Siemens and Michelin.

- Effective financial management focuses on selling financial securities at high values rather than simply minimizing the cost of funds.

- A comprehensive understanding of corporate finance requires mastering financial analysis, market valuation, and value creation.

We are far from the CFOs of the sixties who were mainly top-of-the-class accountants!

The Roles of Financial Management

- The financial manager acts as a salesman who must understand investor needs to successfully market the company's securities.

- Value creation depends entirely on generating a rate of return that meets or exceeds the rate required by investors.

- A critical role of the manager is acting as a 'party-pooper' by rejecting investment projects that do not meet the cost of funds.

- The manager must transform real assets into financial assets while ensuring operational performance is protected from financial volatility.

- Failure to create value leads to declining security prices, management turnover, or eventual bankruptcy.

He must be a “party-pooper”, a “Mr No” who examines every proposed investment project under the microscope of expected returns and advises on whether to reject those that fall below the cost of funds available to the company.

Foundations of Financial Analysis

- Financial securities are defined as tradable contracts representing a series of future cash flows to be received according to a specific timetable.

- The secondary market vastly outweighs the primary market in volume, with trillions in shares exchanged compared to billions in new issuances.

- Risk and return are inextricably linked, with shares carrying higher risk than debt because returns are not guaranteed and creditors have priority.

- Market anticipation is the most critical factor in valuing securities, often outweighing current automatic reactions to interest rate changes.

- Firms face a strategic trade-off between lower short-term interest rates and the significant liquidity risk of constant refinancing.

- Cash flow is established as the fundamental building block for both security valuation and corporate financial analysis.

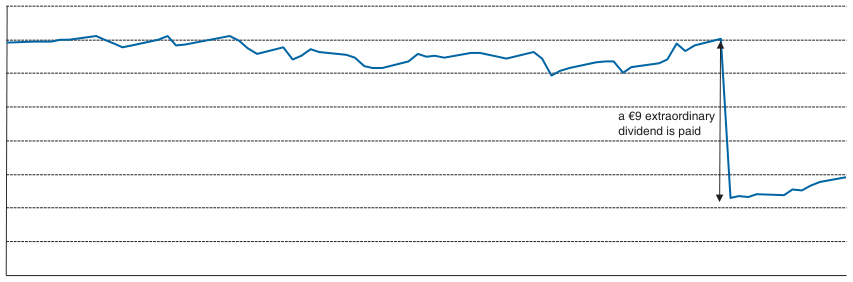

In 2013, worldwide, listed companies issued $191bn worth of new shares, whereas the value of shares exchanged was $52 467bn.

Cash Flow and Operating Cycles

- Financial managers reclassify cash flows into specific categories to analyze past trends and project future budgets.

- Company activities are divided into industrial/commercial processes (operating and investment) and financing activities (debt and equity).

- The operating cycle involves a time lag between the purchase of raw materials and the final sale of goods, which varies by industry.

- The length of the operating cycle can range from a single day in the newspaper business to seven years in the cognac industry.

- Credit terms from suppliers and to customers further complicate cash flow, as daily receipts rarely match daily sales.

A company processes raw materials as part of an operating cycle, the length of which varies tremendously, from a day in the newspaper sector to seven years in the cognac sector.

Operating and Investment Cash Flows

- Operating cash flow represents the net balance of cash generated by a company's day-to-day activities within a specific period.

- The length of an operating cycle varies by industry, typically increasing in duration as the end product becomes more sophisticated.

- Operating cash flow is uniquely objective because it remains independent of accounting policies like depreciation or inventory valuation.

- Investment outflows are distinguished from operating outlays by their long-term perspective, higher risk, and role as prerequisites for new activities.

- While operating cycles involve recurring timing differences, investments are intended to span and support multiple future operating cycles.

The outlay on the chest freezer seems to be a prerequisite. It forms the basis for a new activity, the success of which is unknown.

Investment and Free Cash Flow

- Investment is defined as the deliberate decision to forgo immediate gratification and consumption in exchange for greater future returns.

- The investment cycle is distinguished from the operating cycle by its significantly longer duration and its goal of enhancing future operating cash flows.

- Capital expenditures are financially justified only if the resulting inflows exceed the initial outlays by a margin that meets the investor's expected return.

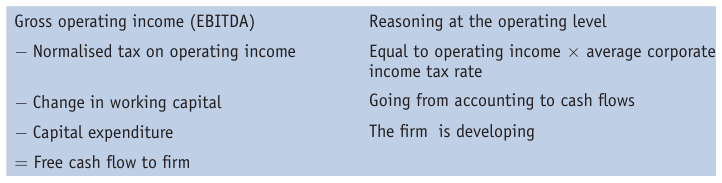

- Free cash flow, the difference between operating cash flow and net capital expenditure, is a primary metric for valuation and determining funding needs.

- Financial resources, provided by shareholders and debtholders, exist to bridge the timing gaps between cash outflows and subsequent receipts.

Only the very puritanically minded would take more pleasure from buying a microwave than from spending the same amount of money at a restaurant!

The Dynamics of Financing Cycles

- Financial resources are provided with the expectation of rewards such as dividends, interest payments, or capital gains.

- Shareholders' equity serves as the cornerstone of the financial system, bearing the primary business risk in exchange for decision-making control.

- Debt capital involves firm commitments to repay principal and interest regardless of the company's operational success or failure.

- The financing cycle acts as the 'flip side' of investment and operating cycles, bridging the gap when free cash flow is negative.

- Lenders prioritize financial health and certainty of repayment, seeking to avoid direct exposure to the company's inherent business risks.

- Surplus cash flows are typically directed into short-term marketable securities to ensure liquidity and generate modest financial income.

The debt cycle is the following: the business arranges borrowings in return for a commitment to repay the capital and make interest payments regardless of trends in its operating and investment cycles.

Cash Flow and Debt Dynamics

- Short-term financial investments should be viewed as the opposite of debt rather than independent assets.

- Financial analysis is most effective when reasoning in terms of debt net of short-term investments and financial income.

- A simplified cash flow statement tracks the net decrease in debt by balancing operating, investment, and financing flows.

- Capital expenditures are strategic outlays designed to enhance the operating cycle and generate higher long-term profitability.

- Free cash flow is defined as the operating cash flow remaining after accounting for capital expenditure outlays.

- The operating cycle is defined by the inherent time lag between production costs and commercial receipts.

As a result, investors forego immediate use of their funds in return for higher cash flows over several operating cycles.

Financing Cycles and Debt Dynamics

- Companies with negative free cash flow must bridge funding gaps by raising equity or debt capital through the financing cycle.

- Equity returns are inherently unpredictable and tied to business success, whereas debt requires fixed repayments regardless of performance.

- Debt is conceptualized as an advance on future operating receipts, fundamentally guaranteed by the company's existing shareholders' equity.

- Financial analysis should focus on net debt and net financial expense by accounting for cash and marketable securities.

- Operating cash flow is distinct from accounting profit and serves as the primary source for satisfying both lenders and shareholders.

Accordingly, debt represents an advance on the operating receipts generated by the investment that is guaranteed by the company’s shareholders’ equity.

Cash Flow and Wealth Creation

- The text outlines a practical exercise for calculating monthly and annual cash flow requirements for a subsidiary with specific inventory and payment cycles.

- It emphasizes that negative free cash flows from operations and investments must be bridged by resources from the financial cycle, such as debt or equity.

- Operating cash flow is identified as the company's 'raison d'être,' which must remain positive in the long term to ensure business survival.

- Free cash flow represents the surplus available to lenders and shareholders after all operating and investment outlays have been settled.

- The transition from cash flow analysis to the income statement marks a shift toward understanding how various business cycles create accounting wealth.

- A distinction is made between cash flow and accounting profit, noting that insolvency is the inability to meet financial obligations regardless of theoretical profit.

If it is not positive in the long term, the company will be in trouble.

Wealth Versus Cash Flow

- Wealth and cash are distinct financial concepts that students and professionals often confuse.

- Purchasing an asset at market price or taking out a loan does not change net worth, only the composition of assets and liabilities.

- The income statement measures additions to and deductions from wealth, whereas the cash flow statement tracks the movement of liquid funds.

- Earnings represent the net change in wealth over a specific period, resulting from the difference between revenues and costs.

- The operating cycle is the primary engine for wealth creation, involving the transformation of resources into market-recognized value.

- Some financial transactions impact cash without affecting wealth, while others destroy wealth without immediate cash consequences.

Spending money does not necessarily make you poorer. Likewise, receiving money does not necessarily make you richer.

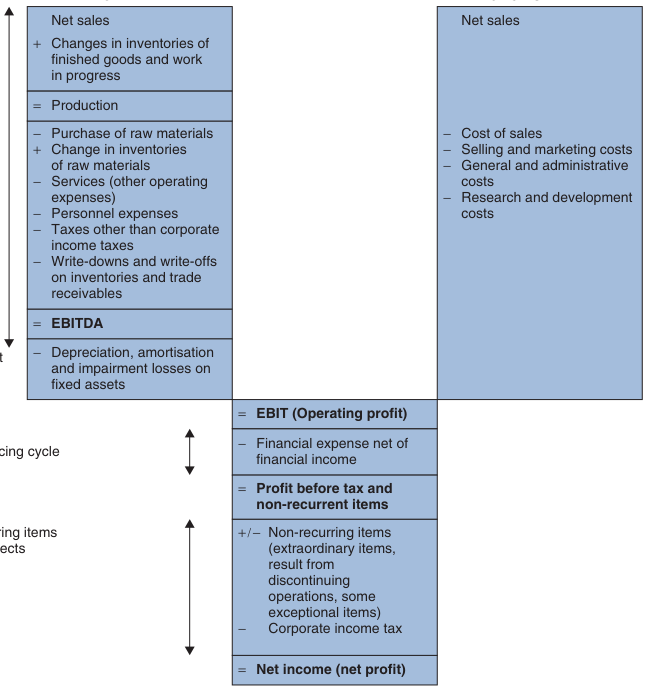

Earnings and the Investing Cycle

- Gross operating profit, or EBITDA, represents the balance of revenues and cash costs before non-cash expenses like depreciation.

- Investing activities are distinct from the income statement because they represent a use of funds that retains value rather than destroying wealth.

- Fixed assets undergo depreciation and amortization to account for the loss of value through use, which are considered non-cash costs based on accounting assessments.

- Impairment losses recognize unforeseen diminutions in value for tangible and intangible assets that are not related to daily operations.

- The fundamental distinction between operating costs and fixed assets lies in whether a resource is consumed during production or used repeatedly without being destroyed.

- Practical accounting often struggles to categorize certain outlays, such as advertising, which could be viewed as either a periodic charge or the creation of a long-term brand asset.

Without wishing to philosophise, we note that the act of creation always entails some form of destruction.

Operating Income and Financing Cycles

- Operating profit or EBIT represents the wealth generated by a company's core industrial and commercial activities, excluding financial operations.

- A fundamental distinction is made between the 'real world' of operations and the 'realms of finance' when calculating earnings.

- Repayments of debt principal are not considered expenses on the income statement because they do not decrease the company's net wealth.

- Interest payments on debt are recorded as expenses because they represent a genuine outflow of wealth to creditors.

- Net earnings and financial interest are both methods of distributing the wealth created by the company to different stakeholders.

- Dividends and share buy-backs are treated as cash position choices for shareholders rather than costs that measure wealth creation.

Just as common sense tells us that securing a loan does not increase wealth, neither does repaying a borrowing represent a charge.

Extraordinary Items and Income Formats

- Extraordinary items like natural disasters or government expropriations are categorized separately because they are infrequent and beyond management's control.

- Disinvestment is a strategic entrepreneurial activity that generates exceptional inflows and capital gains or losses, often complicating financial forecasting.

- Net income serves as a wealth indicator rather than a cash indicator, incorporating non-cash items like depreciation while ignoring unrealized value increases.

- Income statements are primarily formatted either 'by function' (e.g., cost of goods sold) or 'by nature' (e.g., personnel expenses and raw materials).

- While different countries favor specific formats, such as the US preferring 'by function,' the resulting operating profit remains identical regardless of the method used.

The best-laid plans may fail, while others may lead down a strategic impasse. Put another way, disinvesting is also a key part of an entrepreneur’s activities.

Income Statement Presentation Formats

- The 'by-function' income statement format allocates costs to specific corporate departments such as production, marketing, R&D, and administration.

- Global adoption of these formats varies significantly by country, with the UK and Morocco favoring 'by-nature' reporting while Germany and Japan lean toward 'by-function'.

- In a by-function model, personnel and depreciation expenses are fragmented across different categories based on the employee's role or the asset's use.

- A primary advantage of the by-function approach is that it clearly identifies the gross margin by subtracting the cost of sales from net sales.

- A significant drawback for analysts is that the by-function format obscures the distinction between operating and investment processes by hiding total depreciation.

On the other hand, it does not differentiate between the operating and investment processes since depreciation and amortisation is not shown directly on the income statement.

The By-Nature Income Format

- The by-nature income statement format is traditional in continental Europe and categorizes costs as they are incurred rather than by their function.

- This format is simpler for small companies to implement because it requires no complex allocation of expenses across departments.

- To maintain the accrual principle, adjustments must be made for changes in inventory to ensure the statement compares like with like.

- The format focuses on total production for the period rather than just the cost of goods sold.

- A logical disadvantage is that inventory changes can be misinterpreted as independent revenue or expenses rather than mere cost adjustments.

The transfer of these purchases to inventory does not destroy any wealth. Instead, it represents the formation of an asset, albeit probably a temporary one, but one that has real value at a given point in time.

Accounting Formats and EBITDA

- The by-nature format records all costs incurred during a period and adjusts for inventory changes, while the by-function format focuses on the cost of goods sold.

- EBITDA serves as a measure of profit generated by the operating cycle, independent of fixed asset valuation or taxation systems.

- A fundamental distinction exists between cash flow and wealth creation; spending money on assets does not necessarily reduce net worth.

- Inventory valuation methods significantly impact EBITDA, making the by-nature format useful for highlighting the magnitude of inventory changes.

- EBIT represents the profit from both operating and investment cycles, which is then allocated to financial expenses, taxes, and net income.

Spending money does not necessarily make you poorer and neither does receiving money necessarily make you any richer.

Accounting Principles and Wealth Creation

- The text explores the fundamental distinction between cash flow and wealth creation through complex R&D and acquisition scenarios.

- It challenges the assumption that EBITDA or net income directly translates to liquid cash or immediate shareholder enrichment.

- The section highlights the accounting treatment of inventories, depreciation, and non-cash expenses in different income statement formats.

- It examines the impact of asset sales and debt repayment on various levels of profitability, from operating profit to net income.

- The exercises require distinguishing between 'by-nature' and 'by-function' income statements to assess a company's financial health.

Analyse the similarities and the differences between cash and wealth, looking at, for example, investment in real estate and investment in research.

Financial Analysis and Reporting Exercises

- The text presents practical accounting exercises involving the creation of income statements using both 'by-nature' and 'by-function' formats.

- A case study of an Indian barrel manufacturer illustrates how inventory changes and production costs impact the calculation of EBIT.

- A magazine startup scenario explores the divergence between accounting profit and cash flow statements during the initial years of operation.

- The material distinguishes between wealth creation (accounting profit) and cash liquidity, noting that borrowings do not constitute income.

- The exercises emphasize that depreciation is a non-cash charge that reduces taxable income without requiring an immediate cash outflow.

- The text highlights that different asset classes, such as real estate versus R&D, have vastly different implications for wealth versus cash flow.

Confusion between additions to and deductions from wealth (which is an accounting issue) and cash: in the former, new borrowings do not add wealth to cover the losses.

Earnings and Income Statement Analysis

- The text distinguishes between cash receipts and accounting revenues, highlighting that non-cash expenses like depreciation represent an accounting valuation of destroyed wealth.

- Inventory adjustments are used to counterbalance costs in the income statement, ensuring that unsold products do not unfairly impact the current year's net income.

- Capital gains from the sale of fixed assets are typically treated as exceptional or non-recurring items unless the company's primary business is the regular sale of such assets.

- Financial managers face a measurement dilemma regarding non-cash and deferred charges because these figures are based on subjective accounting decisions rather than direct cash flow.

- A comparison of 'by-nature' and 'by-function' income statements demonstrates that while presentation formats differ, the resulting EBIT remains identical.

- Small company margins can appear artificially high when owners opt for lower wages and higher dividends to take advantage of more favorable tax rates.

A non-cash expense is a charge which does not reflect a specific expense, but an accounting valuation of how much wealth has been destroyed.

Earnings and Balance Sheet Fundamentals

- The text illustrates the 'by-function' income statement, categorizing costs into sales, marketing, and administrative buckets to arrive at EBIT.

- A practical example of a magazine startup demonstrates how advance subscription payments can serve as a primary financing mechanism for a project.

- Financial analysis transitions from a dynamic view of inflows and outflows to a static 'snapshot' of balances at a specific point in time.

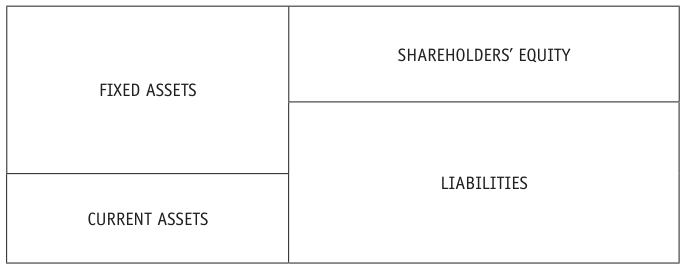

- The balance sheet is defined as the arithmetic sum of all historical inflows and outflows since the inception of the business.

- Assets are categorized into fixed or non-current assets, representing items required for the operating cycle that are not consumed immediately.

If you can convince your clients to pay their subscription before they get the first issue, they will basically finance the project!

Anatomy of the Balance Sheet

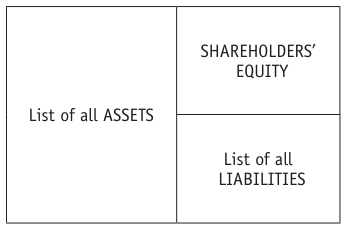

- The balance sheet is structured around the fundamental principle of double-entry accounting, where assets must always equal the sum of equity and liabilities.

- Assets are categorized into fixed assets (tangible and intangible) and current assets, which represent items that 'turn over' during the operating cycle like inventory and cash.

- Global accounting standards vary in presentation, with Europeans typically listing fixed assets first while North American and Japanese firms prioritize liquidity by starting with cash.

- A capital-employed perspective focuses on how a company uses and sources funds to drive its operating cycle and calculate rates of return.

- A solvency-and-liquidity perspective views the balance sheet as a list of everything owned versus everything owed to assess bankruptcy risk and net book value.

According to the algebra of accounting, assets and resources (equity and liabilities) always carry the opposite sign, so the equilibrium of the balance sheet is always maintained.

Capital Employed Balance Sheet Analysis

- Capital-employed analysis focuses on the 'stocks' of capital within an operating cycle rather than just cash inflows and outflows.

- Fixed assets should be categorized into operating and non-operating assets to identify core business investments versus disposable resources.

- Working capital represents the net balance between operating costs incurred but not yet used (inventories/receivables) and charges not yet paid (payables).

- A positive working capital balance indicates a need for financing, while a negative balance represents a rare source of funds generated by operations.

- The text argues against defining working capital as current assets minus current liabilities, as this conflates operating and financing cycles.

If negative, it represents a source of funds generated by the operating cycle. This is a nice – but rare – situation!

Working Capital and Capital Employed

- Operating working capital is calculated by combining inventories and trade receivables, then subtracting trade payables.

- Financial analysis requires adjusting working capital to exclude abnormal or speculative inventory levels and unusually long supplier payment periods.

- Working capital is independent of fixed asset valuation but is heavily influenced by inventory methods and provisioning policies.

- Non-operating working capital acts as a catch-all category for non-recurring items like amounts due on fixed assets and extraordinary items.

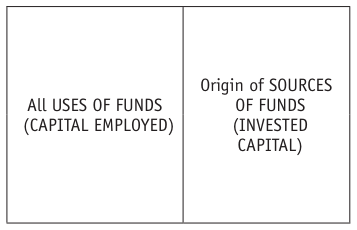

- Capital employed represents the total net amounts devoted to both operating and investing cycles, financed by equity and net debt.

Where it is permanent, the abnormal portion should be treated as a source of cash, with the suppliers thus being considered as playing the role of the company’s banker.

Debt and Capital Analysis

- Gross debt is defined as the sum of all medium-term, long-term, and short-term financial borrowings regardless of maturity.

- Net debt is calculated by subtracting cash, equivalents, and marketable securities from the total gross debt.

- A company with negative net debt is described as having 'net cash,' indicating its liquid assets exceed its total borrowings.

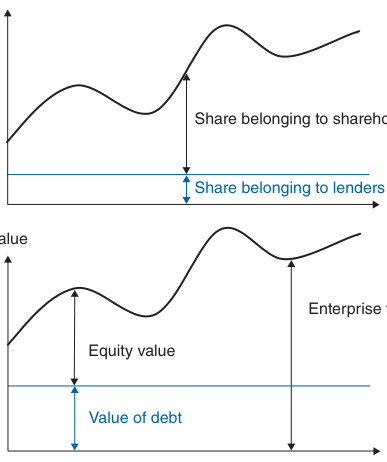

- Capital employed is the sum of fixed assets and working capital, which must equal the total invested capital (equity plus net debt).

- Solvency and liquidity analysis serves as a risk assessment tool for creditors and a valuation checklist for shareholders.

- In a liquidation scenario, shareholders' equity acts as the ultimate guarantee because creditors' claims are prioritized.

In a capitalist system, shareholders’ equity is the ultimate guarantee in the event of liquidation since the claims of creditors are met before those of shareholders.

Liquidity and Solvency Fundamentals

- Balance sheet items must be reclassified by duration to assess liquidity, distinguishing between short-term and long-term obligations based on a one-year threshold.

- Liquidity is defined by the speed at which assets are monetized through the operating cycle compared to the contractual maturity of liabilities.

- A fundamental rule of finance dictates that current assets must exceed short-term liabilities to provide a margin of safety for creditors.

- There is a structural tension between the predictable, contractual maturity of liabilities and the unpredictable, risk-prone liquidity of assets.

- Solvency is the measure of a company's ability to honor commitments during liquidation, occurring when shareholders' equity remains positive.

- The book value of equity represents the net asset value, calculated as the sum of all assets minus all existing and potential liabilities.

Consequently, the clearly defined maturity structure of a company’s liabilities contrasts with the unpredictable liquidity of its assets.

Capital Employed and Balance Sheets

- Acquirers often apply stricter valuation methods by including contingent liabilities and excluding intangible assets of zero value.

- The capital-employed balance sheet provides a snapshot of a company's cumulative inflows and outflows, categorized into assets and resources.

- Operating working capital is calculated by netting trade receivables and inventories against trade payables and social security liabilities.

- Invested capital is the sum of group equity and adjusted net debt, which must equal the total capital employed by the firm.

- Fixed assets represent the long-term investments made by a company, including tangible assets, goodwill, and equity in associated companies.

This very often applies to most intangible assets owing to the complexity of the way in which they are accounted for.

Capital Employed and Liquidity

- Capital employed is defined as the sum of fixed assets and working capital, representing the total resources used by a business.

- Invested capital, consisting of shareholders' equity and net debt, serves as the financing counterpart to capital employed.

- Net debt is calculated by subtracting cash, equivalents, and marketable securities from total bank and financial borrowings.

- Solvency analysis evaluates a company's ability to honor commitments during liquidation, while liquidity focuses on meeting obligations through ordinary business operations.

- The text distinguishes between operating working capital, driven by the business cycle, and non-operating working capital.

- A series of practical exercises challenges the reader to classify financial items and differentiate between accounting 'stocks' and 'flows'.

Solvency measures the company’s ability to honour its commitments in the event of liquidation, whereas liquidity measures its ability to meet its commitments up to a certain date by monetising assets in the ordinary course of business.

Reconciling Earnings and Cash Flow

- The text distinguishes between capital-employed analysis for fund usage and solvency-and-liquidity analysis for asset listing.

- It highlights that while income statements and cash flow statements use different methodologies, they must eventually converge over time.

- Specific industry dynamics, such as movie rights or pay TV, significantly alter the timing between invoicing and actual cash inflow.

- The transition from earnings to net debt change is identified as a fundamental step in understanding a company's financial mechanics.

- Assets are categorized by liquidity, ranging from listed securities to specialized physical plant equipment.

But common sense tells us that a rich woman will sooner or later have cash in her pocket, while a poor woman is likely to be strapped for cash – unless she should make her fortune along the way.

Earnings to Cash Flow

- Operating receipts differ from sales figures because of payment terms granted to customers and the timing of invoice settlements.

- Changes in inventories of finished goods are accounting entries that must be reversed in cash flow analysis because they have no immediate cash impact.

- Operating payments are derived from operating costs by adjusting for supplier credit terms and the difference between materials purchased versus materials used.

- The gap between accounting earnings and actual cash flow is primarily composed of timing differences related to deferred payments and deferred charges.

- The transition from EBITDA to operating cash flow is calculated by subtracting the change in operating working capital.

But this is merely an accounting entry to deduct from operating costs, those costs that do not correspond to products sold. It has no impact from a cash standpoint.

Earnings to Cash Flow

- The change in operating working capital represents the timing difference between wealth created (EBITDA) and actual operating cash flows.

- A positive change in working capital indicates a financing requirement, while a negative change acts as a source of funds.

- Capital expenditures impact the cash flow statement immediately upon purchase but are spread across the income statement via depreciation.

- The income statement and cash flow statement diverge significantly because accounting depreciation involves no actual cash outflow.

- Financing cycles involve inflows like new borrowings and outflows like dividends, which are treated differently in accounting versus cash analysis.

- Analyzing changes in working capital is considered a fundamental pillar of financial analysis due to the potential scale of timing differences.

As we shall see, it is important to remember that timing differences may not necessarily be small, of limited importance, short or negligible in any way.

From Earnings to Cash Flow

- Distinguishes between financial expenses that affect both earnings and cash versus capital movements that only impact cash.

- Explains that corporate income tax is a charge for state-provided infrastructure and services despite being a cash outflow.

- Provides a structural bridge between the income statement and the cash flow statement to calculate the decrease in net debt.

- Highlights the necessity of adding back non-cash charges like depreciation and amortization to net income to determine actual cash flow.

- Identifies the timing differences in the operating cycle, specifically working capital, as a key factor in cash availability.

- Notes that investing and financing cycles create fund movements that do not immediately impact net income.

Lastly, corporate income tax represents a charge that appears on the income statement and a cash payment to the State which, though it may not provide any financing to the company, provides it with a range of free services and entitlements, e.g. police, education, roads, etc.

Defining and Calculating Cash Flow

- Cash flow is calculated by adding non-cash charges like depreciation and amortization back to net income to show total internal financing.

- Traditional accountants distinguish between financial expenses and debt repayments, viewing the former as wealth reduction and the latter as liability management.

- To maintain relevance and avoid artificial volatility, cash flow should ideally exclude non-recurring items and capital gains or losses on asset disposals.

- The calculation of cash flow differs in consolidated accounts, where equity-accounted income is replaced by actual dividends received from associates.

- There is no universal definition of 'cash flow,' and the term is often used interchangeably with free cash flow or operating cash flow, requiring careful verification.

Lastly, readers should beware of cash flow as there are nearly as many definitions of cash flow as there are companies in the world!

Analyzing Cash Flow Cycles

- Cash flow from operating activities is derived by adjusting raw cash flow for timing differences in the operating working capital cycle.

- The investment cycle tracks capital expenditures, asset disposals, and changes in long-term financial assets.

- The financing cycle encompasses capital increases, dividend payments, share buy-backs, and changes in net debt.

- Net debt is presented as a superior metric for assessing a company's true indebtedness compared to simple cash and equivalents.

- Most corporate cash flow statements utilize the indirect method, starting with net income and reconciling down to cash position changes.

- The Indesit case study illustrates how free cash flow is calculated by subtracting investing activities from operating activities.

Net debt reflects the level of indebtedness of a company much better than cash and cash equivalents or than cash and cash equivalents minus short-term borrowings, since the latter are only a portion of the debt position of a company.

From Earnings to Cash Flow

- The transition from income statement to cash flow perspective requires recreating operating cash flows by adjusting for timing differences and inventory changes.

- Operating working capital accounts for the gap between the generation of wealth (EBITDA) and actual operating cash flow.

- Capital expenditures create a disconnect between cash and income because the former records immediate payment while the latter spreads costs over a useful life.

- The cash flow statement treats capital and remuneration for financing differently than the income statement, which only shows interest and taxes.

- Net debt must be managed globally because increasing cash through long-term debt does not improve a company's actual net financial position.

- Cash flow only translates into actual cash on hand once adjusted for operating working capital, investment cycles, and financing cycles.

Cash on the balance sheet has increased but net debt is still the same.

Cash Flow vs Accounting Profit

- The text distinguishes between accounting wealth (net income) and cash position, noting that non-cash expenses like depreciation reduce profit but not cash.

- Cash flow is not a direct measure of wealth creation because it ignores the 'wealth destruction' caused by the wear and tear of fixed assets.

- Operating cash flow differs from EBITDA primarily due to changes in working capital, such as unpaid invoices and inventory fluctuations.

- Net debt is identified as a more reliable metric than cash position because year-end cash balances are easily manipulated compared to total indebtedness.

- Pure accounting entries, such as capital increases via incorporation of reserves, have no impact on the cash flow statement.

- The provided financial forecast illustrates how a company can experience negative cumulative cash balances despite consistent sales and production.

No, cash flow is not a measure of increase in wealth because it does not take into account depreciation, which reflects the wear and tear of fixed assets and thus a source of wealth destruction.

Earnings to Cash Flow

- The text provides a detailed walkthrough of financial statements for a Spanish subsidiary, illustrating the transition from net earnings to cash flow.

- Two different formats for the cash flow statement are presented, highlighting how EBITDA and net income serve as different starting points for analysis.

- The subsidiary demonstrates rapid financial recovery, with capital expenditures and working capital increases nearly repaid within three years.

- The balance sheet data tracks the evolution of capital employed and net debt, showing a shift from initial investment to a net cash position by 2016.

- The transition to Chapter 6 introduces the concept of consolidated accounts, which treat a group of companies as a single economic entity.

This outfit is profitable the first year, and capital expenditure and increase in working capital (30 + 36) are nearly entirely paid back at end-2016 after only three years of activity. It is almost too good to be true!

Principles of Consolidated Accounts

- Consolidated accounts aim to present a group of companies as a single financial entity rather than a collection of separate book values.

- Any firm exercising exclusive control or significant influence over other companies is generally required to prepare and certify group-level reports.

- Since 2005, listed European companies and many global groups have been mandated to follow IFRS accounting principles for consolidation.

- The scope of consolidation is determined by the parent company's material influence, typically assumed at a threshold of 20% of voting rights.

- Consolidation replaces the historical cost of a parent's investment with the actual assets, liabilities, and equity of the subsidiary.

- Two primary methods exist for reporting: full consolidation for controlled subsidiaries and the equity method for associates with significant influence.

The basic principle behind consolidation consists of replacing the historical cost of the parent’s investment in the company being consolidated with its assets, liabilities and equity.

Mechanics of Full Consolidation

- Full consolidation is triggered by control, defined as the power to direct strategic policies to access benefits, often through majority voting rights or board control.

- Under IFRS, exclusive control is the primary criterion, whereas US GAAP traditionally focuses on majority voting rights but can encompass minority-held entities.

- The process involves transferring all of a subsidiary's assets, liabilities, revenues, and costs directly onto the parent company's financial statements.

- Parent company investments in the subsidiary are eliminated and replaced by the subsidiary's actual accounts to avoid double counting.

- Minority interests represent the portion of equity and net income belonging to third-party shareholders and are reported separately from the parent's equity.

- While minority interests count as equity for solvency analysis, they are excluded from the group's valuation as they belong to external parties.

Nevertheless, the definition is broader and can encompass companies in which only a minority is held (or even no shares at all!).

Consolidation and Equity Accounting

- Full consolidation assumes a parent company economically controls 100% of a subsidiary's assets and liabilities, regardless of the legal ownership percentage.

- Minority interests represent the specific portion of equity and net income belonging to outside shareholders in a partially-owned subsidiary.

- The equity method is required when a parent company exerts significant influence, typically defined as holding at least 20% of voting rights.

- Significant influence is evidenced by board participation, strategic decision-making, or technical dependence rather than just ownership stakes.

- The International Accounting Standards Board (IASB) views the equity method as a valuation tool rather than a true consolidation method.

- Under the equity method, the carrying amount of shares is replaced by the group's proportional share of the associate's equity and net income.

This is true from an economic, but not from a legal, perspective.

The Equity Method and Control

- The equity method replaces the historical cost of an investment with the parent company's share of the associate's equity and net income.

- Accounting for associates via the equity method is described as a reevaluation of participating interests rather than a full consolidation of assets and liabilities.

- A significant limitation of the equity method is that it fails to reflect the group's total risk exposure or liabilities regarding the associate.

- The scope of consolidation is determined by the level of control, which is primarily measured by the percentage of voting rights held.

- Control is generally assumed at a 50% voting threshold or through de facto control, distinguishing it from the simple level of ownership.

The equity method of accounting is more a method used to reevaluate certain participating interests than a genuine form of consolidation.

Ownership Levels and Consolidation Scope

- Ownership level is a financial concept representing the parent company's claim on capital, distinct from the power-related concept of control.

- The ownership level is calculated as the sum of the products of direct and indirect percentage stakes across a corporate hierarchy.

- Full consolidation uses ownership levels to allocate net income and reserves between the parent company and minority interests.

- Excluding subsidiaries from consolidation can be a tactic to hide losses or liabilities, often utilizing Special Purpose Vehicles (SPVs).

- Modern accounting standards like IFRS and US GAAP require consolidation of SPVs if the parent company bears the residual risks or enjoys the majority of benefits.

- Proforma financial statements are essential for analysts to compare performance consistently when the scope of consolidation changes.

These techniques have been developed to make certain consolidated accounts look more attractive.

Understanding Goodwill and Acquisitions

- Acquisition prices often exceed a target company's book value due to unrecorded assets like patents, market share, or brand reputation.

- Buyers may pay a premium to capture potential synergies, such as cost reductions or revenue enhancements, or to block competitors from entering a market.

- The difference between the purchase price and equity is split into latent capital gains on specific assets and a residual amount known as goodwill.

- Under the purchase method, acquired assets and liabilities are revalued to fair market value and aligned with the parent company's accounting policies.

- Goodwill is not amortized but must undergo an annual impairment test to ensure its market value remains at least equal to its recorded book value.

The buyer may be ready to pay a high price for a target just to prevent a new player from buying it, entering the market, and putting the current level of the buyer’s profitability under pressure.

Goodwill and Acquisition Accounting

- The acquisition of Bulgari by LVMH illustrates how the purchase price is allocated between tangible assets, brand revaluation, and residual goodwill.

- LVMH paid a significant premium over Bulgari's equity, resulting in the creation of €1,375m in new goodwill after adjusting for brand value and liabilities.

- Under IFRS, negative goodwill is treated as an immediate profit in the income statement, though it occurs only under specific circumstances.

- Financial analysts are advised to treat goodwill impairment as a non-recurring item and exclude it from earnings per share or return calculations.

- Goodwill is viewed as having a limited lifespan because market competition eventually erodes the high profitability initially gained through an acquisition.

- While impairment charges are non-cash items, they represent a genuine decrease in company wealth and shareholder equity value.

As we know, goodwill has a limited lifespan in view of the competition prevailing in the business world that will, sooner or later, erode too high a profitability obtained after an acquisition.

Acquisitions and Consolidation Mechanics

- Overpaying for acquisitions with shares is just as detrimental as using cash, as it results in shareholder dilution without proportional growth.

- The 'cake and guests' analogy illustrates how wealth diminishes when asset growth fails to outpace the increase in the number of shares issued.

- Financial analysts use 'adjusted income' in specific sectors to neutralize the P&L impact of asset revaluations following a merger.

- Consolidation requires harmonizing accounting data across subsidiaries to eliminate discrepancies caused by local tax laws or varying valuation methods.

- The consolidation process is simplified by the fact that consolidated accounts are generally not used for calculating taxable income.

They accept this dilution because they take the view that the size of the cake will grow at a faster rate (e.g. by 30%) than the number of guests invited to the party (e.g. by over 25%).

Mechanics of Financial Consolidation

- Consolidation requires the elimination of intra-group transactions to prevent the reporting of fictitious gains or double-counting profits.

- Significant transactions affecting net income, such as intra-group inventory profits and dividends, must be reversed to maintain financial accuracy.

- Non-fundamental transactions, including parent-to-subsidiary loans, are eliminated through netting to reflect the group's true debt levels.

- Translating foreign subsidiary accounts is complicated by fluctuating exchange rates and varying inflation rates that can distort asset values.

- Fixed assets in soft-currency countries may maintain their value due to inflation offsetting devaluation, whereas liquid assets depreciate in tandem with the currency.

An entirely fictitious gain would show up in the group’s accounts if the relevant products were merely held in stock by the subsidiaries rather than being sold on to third parties.

Foreign Subsidiary Consolidation Methods

- The closing rate method is the standard for economically independent subsidiaries, translating all assets and liabilities at the balance sheet date exchange rate.

- The temporal method is used for integrated subsidiaries, distinguishing between monetary items at closing rates and non-monetary items at historical rates.

- Currency translation differences are handled differently across methods, appearing either in shareholders' equity or directly on the income statement.

- Hyperinflationary environments require a specialized method involving restatements via a general price index to account for chronic currency devaluation.

- Consolidation is mandatory for groups where a parent company holds at least 20% of voting rights, aiming to present the group as a single financial entity.

A hyperinflationary country is one where inflation is both chronic and out of control.

Mechanics of Consolidated Accounts

- Full consolidation replaces parent company investments with the subsidiary's total assets and liabilities when voting rights exceed 50%.

- The equity method is applied for associates where the parent holds significant influence, typically between 20% and 50% of voting rights.

- A critical distinction exists between the level of control (voting rights) and the ownership level (capital share) for accounting purposes.

- Goodwill is recorded as an intangible asset when a parent pays more than the book value for a company's equity.

- Consolidation requires the elimination of intra-group transactions, such as dividends and internal profits, to ensure data consistency.

- Foreign subsidiary accounts are translated using either the closing rate or temporal method, with special rules for hyperinflationary economies.

The level of control is used to determine which consolidation method is applied. The ownership level is used to separate the group’s interests from minorities’ interests in equity and net income.

Consolidation Methods and Complex Accounting

- The text provides a practical exercise comparing full consolidation (80% stake) with the equity method (20% stake) for a group's financial statements.

- Full consolidation results in the inclusion of minority interests, reflecting the portion of a subsidiary's equity and earnings not owned by the parent group.

- Goodwill is defined as the premium paid over the fair value of a subsidiary's net assets and must be tested annually for impairment.

- The equity method is described not as a consolidation of line items but as a method for revaluing the investment asset based on the associate's performance.

- A paradox exists where a group can register a profit or loss without receiving cash due to changes in their share of a subsidiary's equity.

This chapter is rather different from the others. It is not intended to be read from start to finish, but consulted from time to time, whenever readers experience problems interpreting, analysing or processing a particular accounting item.

Navigating Complex Financial Accounts

- The text outlines a three-pronged methodology for analyzing complex financial issues: economic substance, accounting treatment, and financial resolution.

- A comprehensive list of complex line items is provided, ranging from accruals and deferred taxes to off-balance sheet commitments and stock options.

- Accruals are defined as mechanisms to transfer revenue or costs between the profit and loss statement and the balance sheet to ensure they match the correct period.

- Prepaid costs and deferred income are identified as key components of operating working capital rather than just static accounting entries.

- Cash assets are strictly defined as highly liquid, short-term investments with negligible risk of value change to qualify as cash equivalents.

- The methodology encourages readers to develop independent problem-solving skills for financial issues not explicitly covered in the text.

To accrue basically means to transfer revenue or costs from the P&L to the balance sheet.

Accounting for Complex Assets

- The 2007-2008 liquidity crisis revealed that many supposedly safe monetary investments were actually volatile and illiquid.

- Financial analysts must distinguish between assets contributing to operating earnings and those that are purely financial investments to properly calculate net debt.

- Construction contracts are typically accounted for using the percentage of completion method to spread profits across the duration of long-term projects.

- The completed contract method, used in some US contexts, is more conservative as it defers revenue recognition until project completion but provisions for all anticipated losses immediately.

- Analysts monitor changes in construction accounting methods because shifts can be used to artificially manipulate a company's reported net income.

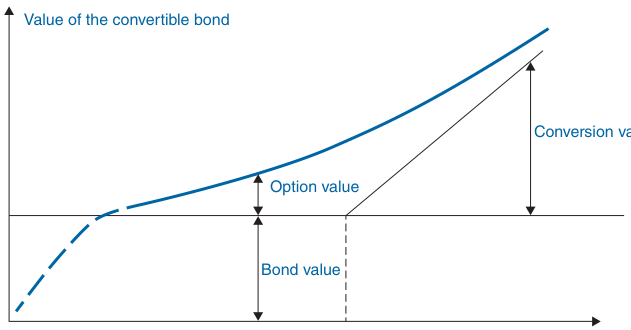

- Convertible bonds are treated as compound financial instruments under IFRS, requiring allocation between debt and equity accounts upon issuance.

Analysts should be aware of changes in accounting methods for construction contracts as such changes may indicate an attempt to artificially improve the published net income for a given year.

Accounting for Convertible Bonds

- Convertible bonds are hybrid instruments composed of a straight bond component and a call option.

- Initial accounting splits the instrument into debt based on fair borrowing rates and equity for the remainder.

- Financial analysts should classify convertibles based on the likelihood of conversion rather than fixed labels.

- If the share price exceeds the conversion price, the bonds should be treated as equity and interest expenses reversed.

- When the share price is below the conversion price, the instruments are treated as standard borrowings.

- Deferred tax assets and liabilities arise from temporary differences between taxable and book values of assets.

For instance, if the share price already lies well above the conversion price, the bonds are very likely indeed to be converted, so they should be treated as equity.

Managing Deferred Tax Accounting

- Accounting profit and taxable profit often diverge due to timing differences in when revenues and charges are recognized.

- Permanent differences occur when specific items, such as tax penalties or fines, are never considered for tax purposes and thus do not trigger deferred tax.

- Temporary differences between an asset's book value and its tax base create deferred tax liabilities or assets on the balance sheet.

- Deferred tax liabilities often arise from asset revaluations during consolidations or capitalized costs that are immediately tax-deductible.

- Deferred tax assets can be generated from tax-loss carryforwards or provisions that only become deductible when a liability actually materializes.

- Companies are required to recognize all deferred tax liabilities, but assets are only recognized if it is probable they will be used to reduce future payments.

Deferred tax assets arising from tax losses should be recognised when it is probable that the deferred tax asset can be used to reduce tax to be paid.

Mechanics of Deferred Taxation

- IFRS standards strictly prohibit the discounting of deferred tax assets and liabilities to their net present value.

- Contingent taxation, such as taxes triggered by future asset sales or dividend distributions, is not recorded on the balance sheet.

- Deferred tax assets often lack economic underpinnings and do not represent actual cash flows or amounts currently due from tax authorities.

- Tax-loss carryforwards are recognized as assets only if there is a reasonable expectation of future profits to offset them.

- Financial analysts should treat deferred tax assets as fixed assets rather than working capital, as they cannot be sold for cash.

- Discrepancies between real cash flows and accounting entries often arise from provisions like retirement benefits that are not immediately tax-deductible.

It is important to recognise that deferred taxation does not represent an amount of tax currently due to or from the tax authorities, but consists of accounting entries with, most of the time, no economic underpinnings and with no corresponding cash flows.

Accounting for Deferred Taxes

- Deferred tax assets and liabilities arise from timing differences between accounting recognition and actual tax payments.

- A deferred tax credit on a balance sheet represents tax already paid that is considered a future expense from an accounting perspective.

- Unlike physical inventories, deferred tax assets have no intrinsic monetary value and are often viewed as accounting constructs rather than liquid assets.

- Asset revaluation during consolidation creates deferred tax liabilities to account for the gap between book value and tax basis.

- The authors advocate for simplifying financial analysis by canceling deferred tax assets against provisions or deducting liabilities from goodwill.

Unlike inventories of raw materials which have been paid for and which are also a future expense, deferred tax has no monetary value.

Dilution and Hedging Accounting

- Dilution profits occur when a subsidiary issues new capital at a valuation higher than its book value without the parent company participating.

- Accounting for dilution results in a non-recurrent gain on the parent's books, representing the implicit profit of a partial deemed sale.

- Financial analysts should disregard dilution gains as they do not involve cash flow and do not reflect a company's recurring earning power.

- Financial hedging instruments like swaps and options are used to mitigate risks from fluctuating exchange rates, interest rates, or commodity prices.

- Under IFRS, derivatives must generally be recorded at fair value on the balance sheet, with value changes impacting the income statement.

- Hedge accounting is a complex system that allows companies to offset these value changes, provided they can prove the hedge is perfectly adjusted to the risk.

They are, by their very nature, non-recurring. Otherwise, the group would soon not have any subsidiaries left.

Fair Value and Cash Flow Hedges

- Fair value hedges protect against changes in the value of existing assets or liabilities, such as fixed-rate debt.

- Cash flow hedges secure the value of future transactions, such as a chocolate producer fixing the price of cocoa.

- IFRS rules allow companies to offset gains and losses on the income statement to prevent accounting distortions.

- Financial analysts must distinguish between speculative transactions and genuine hedging operations.

- Operating hedges should be integrated into EBIT and capital employed, while financial hedges are attached to net debt.

The application of these principles could lead to an absurd situation.

Impairment and Intangible Assets

- Impairment losses are capital reserves set aside to cover anticipated decreases in the value of tangible and intangible assets.

- The recoverable value of a Cash Generating Unit (CGU) is determined by the higher of its value in use or its net selling price.

- Financial analysts typically treat impairment on tangible assets as non-recurring, while impairments on goodwill are viewed as non-operating items.

- Intangible assets like brands and customer lists cannot be recognized if they are internally generated; they must be expensed as incurred.

- Start-up costs, including incorporation and advertising, are expensed under IFRS and should be deducted from equity by analysts as they hold no intrinsic value.

Internally generated goodwill, brands, mastheads, publishing titles and customer lists should not be recognised as intangible assets.

Accounting for Intangible Assets

- Research costs are generally expensed immediately under IFRS due to their unpredictable nature, while development costs can be capitalized if specific feasibility and marketability criteria are met.

- US GAAP maintains a stricter stance than IFRS, generally prohibiting the capitalization of research and development costs except for specific web developments.

- Financial analysts are cautioned to monitor capitalized development costs closely, as they can sometimes be used to mask operational losses.

- Brands and market share are only recorded on balance sheets when acquired from third parties, creating a valuation gap for companies with internally grown brands.

- Major luxury groups like LVMH carry massive brand values on their balance sheets, often treating them as assets with indefinite lives that are tested for impairment rather than amortized.

- While some conservative analysts value brands at zero, the text argues that brands are essential components of a company's true economic value.

For instance, what value would a top fashion house or a consumer goods company have without its brands?

Intangibles and Inventory Valuation

- The book value of intangible assets often inversely correlates with their actual market value due to tax minimization strategies and accounting policies.

- Ailing companies may inflate intangible assets to artificially maintain positive net profit and shareholders' equity.

- Inventories are categorized into raw materials, work in progress, and finished goods, each with specific valuation rules based on acquisition or production costs.

- Production costs must be calculated based on normal activity levels to avoid deferring losses and artificially inflating current year profits.

- IFRS and US GAAP differ slightly on the inclusion of interim interest payments in inventory costs, though general administrative costs are typically excluded.

- The choice between weighted average cost, FIFO, and identified purchase cost methods significantly impacts a company's reported net income.

To sum up, our approach to intangible fixed items is as follows: the higher the book value of intangibles, the lower their market value is likely to be; and the lower their book value, the more valuable they are likely to be.

Inventory Valuation and Financial Analysis

- The IASB prohibits the LIFO method for interchangeable items, while US GAAP continues to permit it alongside FIFO and weighted average cost.

- During inflationary periods, the FIFO method results in higher reported net income compared to LIFO by valuing withdrawals at the oldest, lowest costs.

- Changes in inventory valuation methods must be disclosed as they can artificially inflate profits or mask losses, complicating period-to-period comparisons.

- Managers may be reluctant to scale down production during low demand because running down overvalued inventory leads to a decrease in net income.

- Analysts are advised to prioritize cash flow from operating activities over net income when inventory valuations are speculative or lack market benchmarks.

- Inventory valuation methods generally have no impact on a company's actual cash position, excluding tax-related effects.

Inventories are merely accruals (deferred costs), which are always slightly speculative and arbitrary in nature, even when accounting rules are applied bona fide.

Inventory Valuation and Leases

- The text advocates for replacement cost accounting to recognize inventory gains and losses immediately rather than waiting for sales.

- Delayed recognition of losses, as seen in the Japanese banking crisis, can exacerbate financial instability compared to immediate write-downs.

- Leases are categorized into operating leases and finance leases, with the latter transferring most ownership risks and rewards to the lessee.