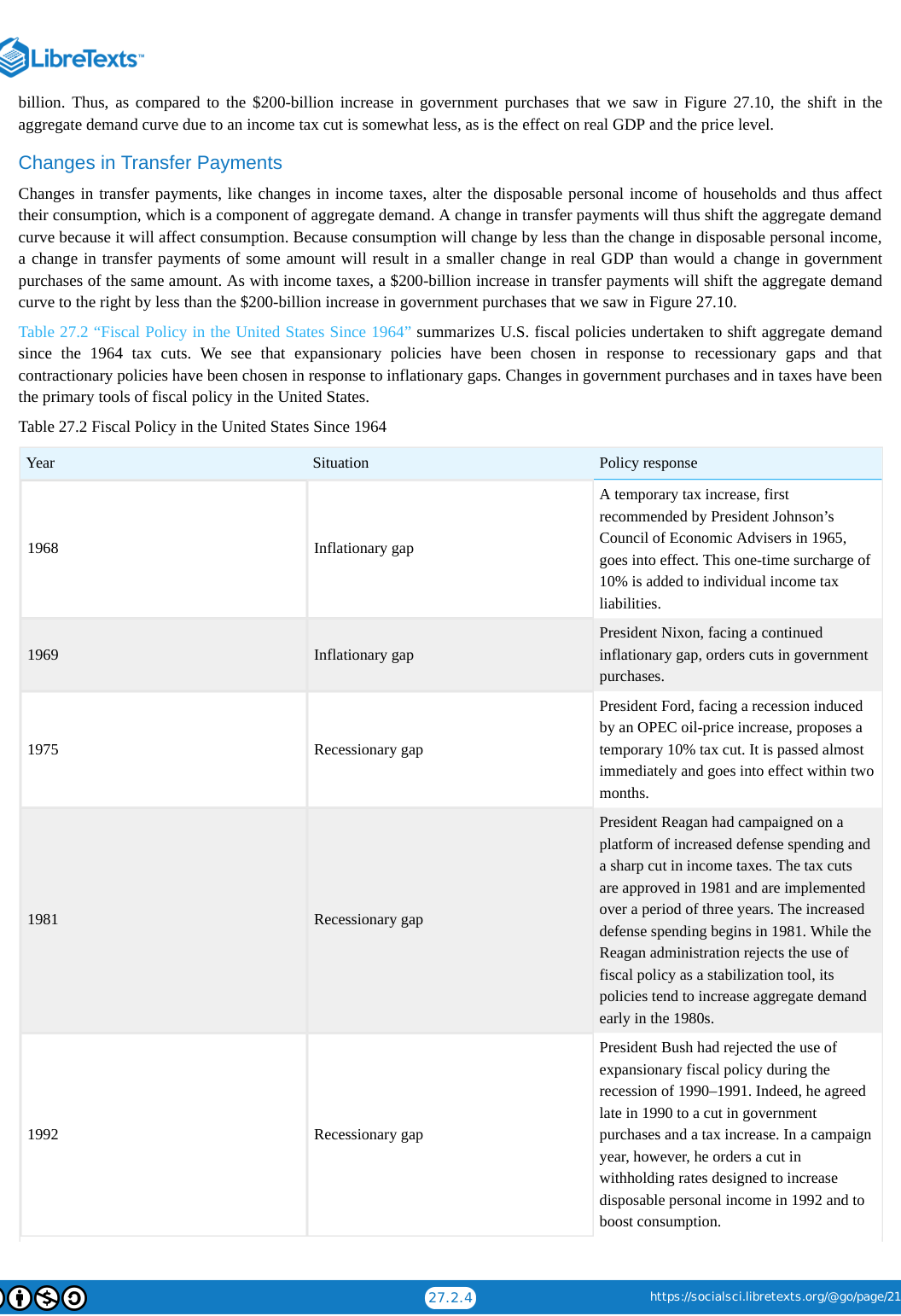

Principles of Economics

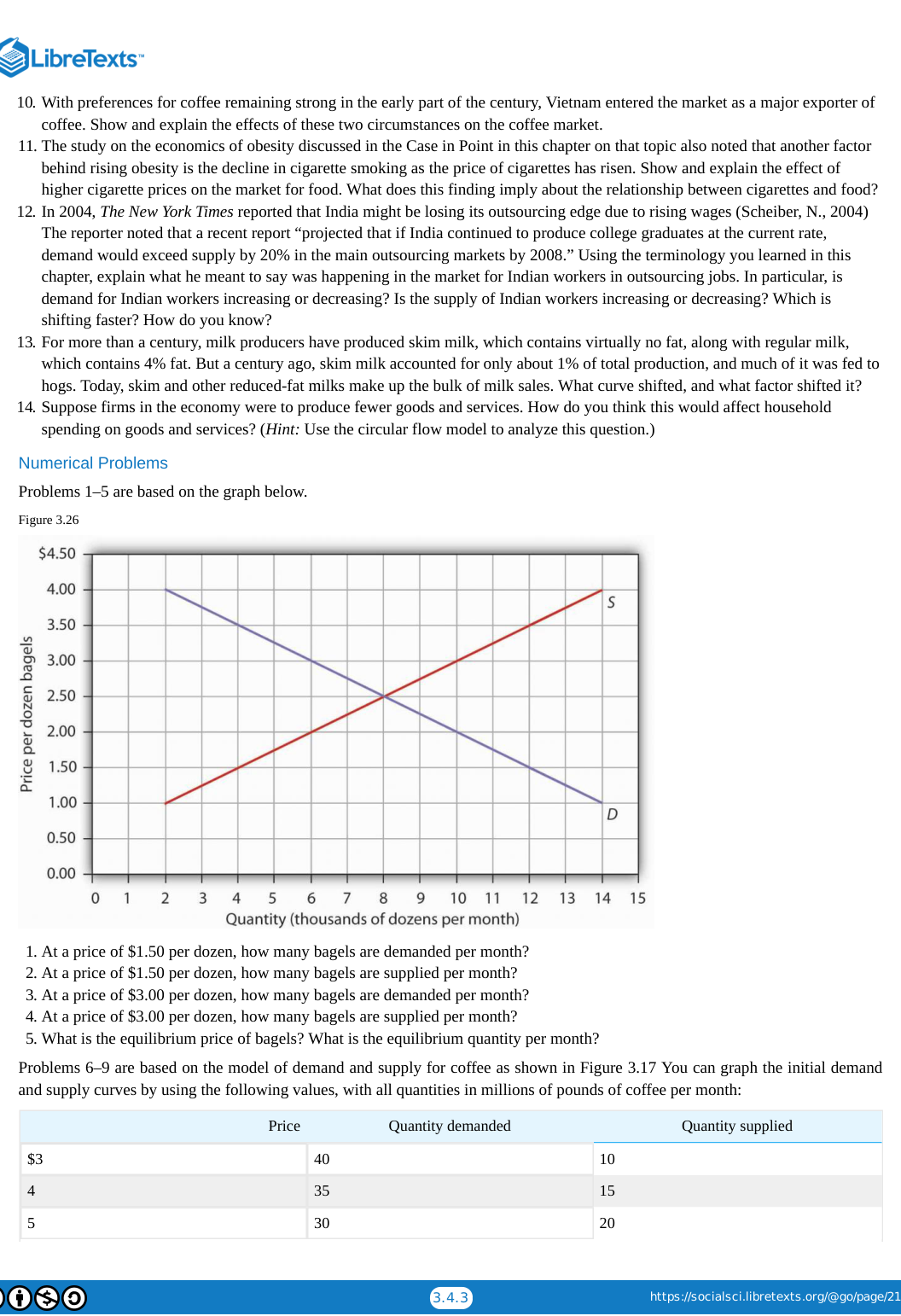

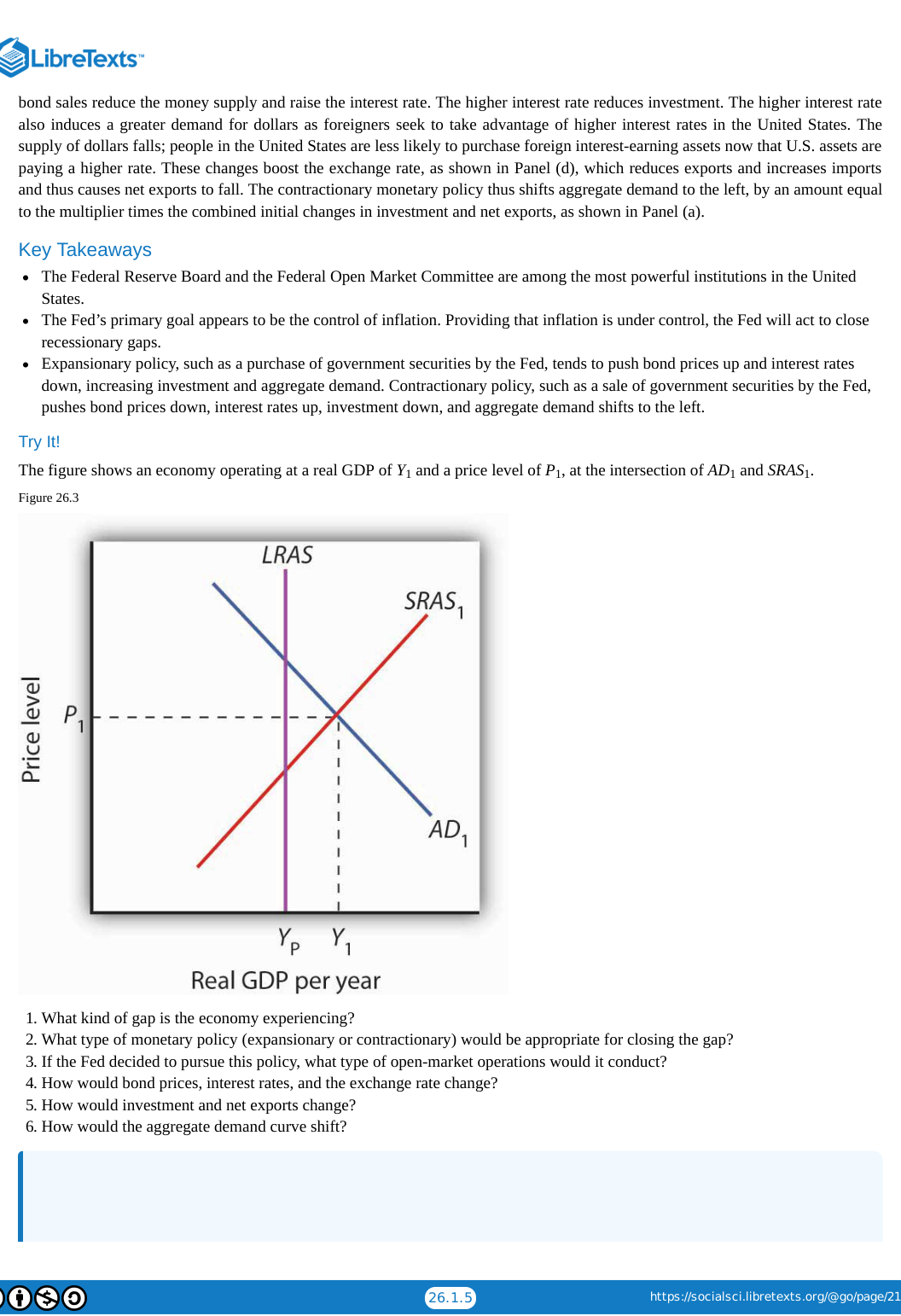

Overview unavailable.

LibreTexts Economics Overview

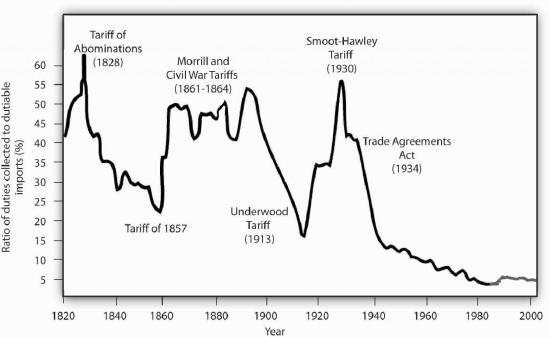

- Introduces Principles of Economics as a freely available LibreTexts Open Educational Resource, with licensing guidance for use, printing, adaptation, and remixing.

- Describes LibreTexts’ mission to provide customizable, low-cost open-access educational materials through a collaborative online platform.

- Acknowledges institutional and grant support, including the Department of Education, UC Davis, CSU Affordable Learning Solutions, Merlot, and the National Science Foundation.

- Provides contact and social media information for questions about adoption or adaptation, and notes the text compilation date of 04/16/2025.

- Lists the full table of contents, covering microeconomics, macroeconomics, international economics, public policy, development, appendices, glossary, index, and detailed licensing.

Economics: The Study of Choice

- Economics is defined as a social science that investigates how individuals and societies make decisions among available alternatives.

- The discipline is categorized as a science because it employs a systematic, scientific approach to study human behavior and decision-making.

- The core of economic theory rests on the relationship between scarcity, choice, and the resulting opportunity costs.

- Every economic system must address three fundamental questions: what to produce, how to produce it, and for whom it is produced.

- Scarcity necessitates choice, meaning that selecting one option inherently requires the sacrifice of another alternative.

Economics is a social science that examines how people choose among the alternatives available to them.

The Reality of Scarcity

- Human wants are unlimited while the resources available to satisfy them are finite.

- Economics is defined by the necessity of making choices between competing alternatives.

- A good is considered scarce if choosing one use for it requires giving up another use.

- Even seemingly infinite resources like air are scarce because they have alternative uses, such as breathing versus pollution.

- Free goods, like gravity, are rare because one person's use does not diminish the availability for others.

- The increasing utilization of outer space demonstrates how free goods can become scarce as human activity expands.

The fact that gravity is holding you to the earth does not mean that your neighbor is forced to drift up into space!

Scarcity and Opportunity Cost

- Every society must address three fundamental questions: what to produce, how to produce it, and for whom it should be produced.

- Scarcity necessitates trade-offs, such as choosing between better education and healthcare or preserving wilderness versus industrial land use.

- The concept of opportunity cost is defined as the value of the best alternative forgone when making a specific choice.

- Opportunity cost differs from purchase price because it includes the value of time and other non-monetary resources sacrificed.

- The most significant cost of a college education is often the value of the time spent studying rather than the direct cost of tuition.

- A good is considered scarce if choosing one alternative requires that another must be surrendered.

Opportunity cost is the value of the best alternative forgone in making any choice.

Scarcity and Opportunity Cost

- Opportunity cost is defined as the value of the best alternative forgone when making a specific choice.

- Economic decisions involve trade-offs between competing interests, such as environmental preservation versus urban housing development.

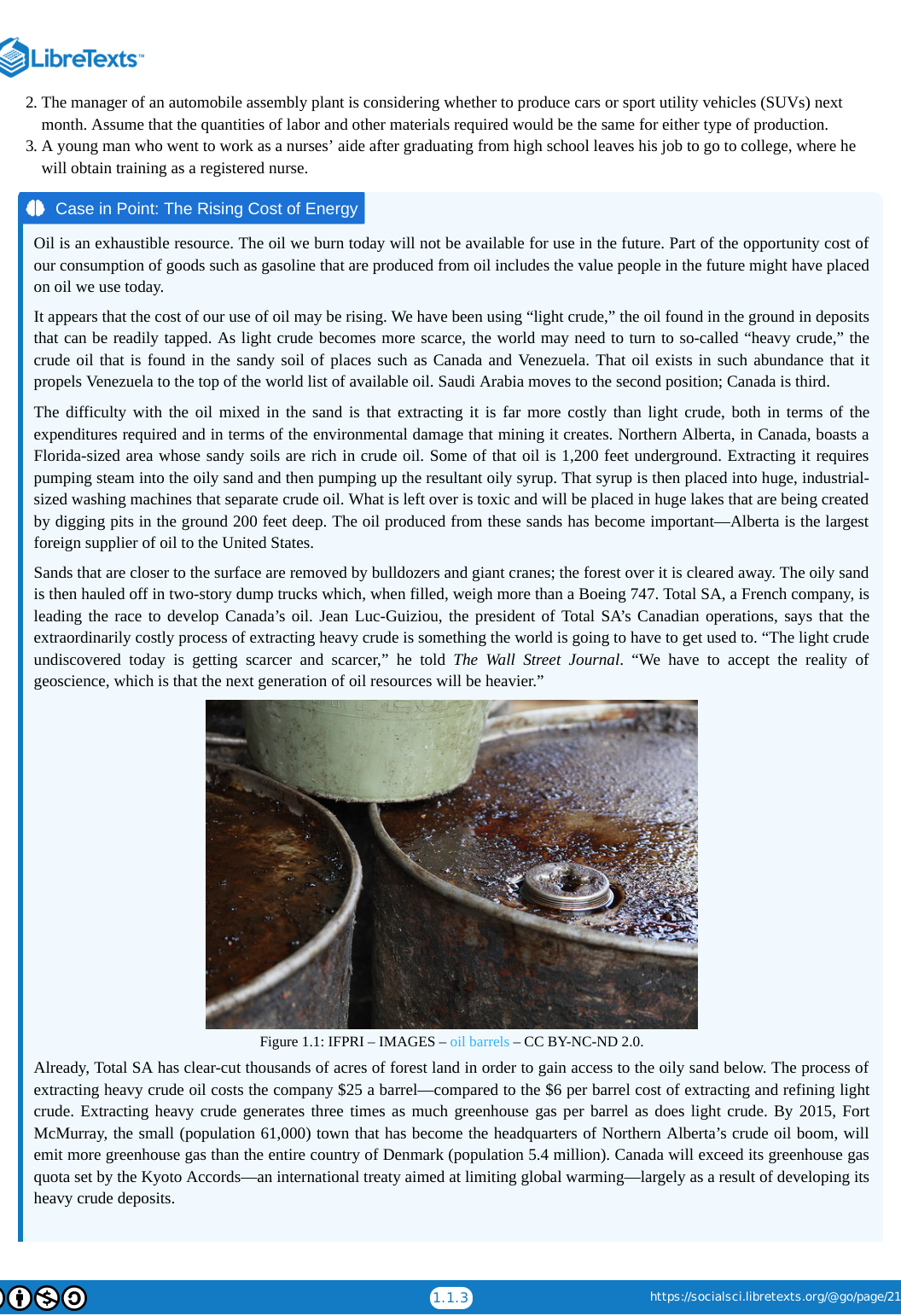

- The consumption of exhaustible resources like oil imposes an opportunity cost on future generations who will no longer have access to those resources.

- As easily accessible 'light crude' oil diminishes, the global economy is shifting toward 'heavy crude' found in sandy soils.

- Extracting heavy crude from oil sands is significantly more expensive and causes greater environmental degradation than traditional drilling.

- The transition to heavier oil resources represents a new geological reality where energy production requires more labor, capital, and ecological sacrifice.

The oily sand is then hauled off in two-story dump trucks which, when filled, weigh more than a Boeing 747.

The Cost of Heavy Crude

- Extracting heavy crude oil from Alberta's oil sands costs $25 per barrel, significantly higher than the $6 required for light crude.

- The environmental impact is severe, with heavy crude production generating three times the greenhouse gas emissions of light crude.

- By 2015, the town of Fort McMurray was projected to emit more greenhouse gases than the entire nation of Denmark.

- Economic viability for oil sands shifted in the mid-2000s as global oil prices surged from $12 to over $70 per barrel.

- The development creates a sharp conflict between economic benefits and the permanent destruction of boreal forest ecosystems.

- The situation illustrates the economic concept of opportunity cost, where resource use requires choosing between competing values like industry and preservation.

“You see a lot of the land dug up, a lot of the boreal forest struck down and it’s upsetting, it fills me with rage,” he says.

The Economic Way of Thinking

- Economics is distinguished from other social sciences by its specific approach to analyzing human choice.

- A core pillar of economic thought is the heavy emphasis placed on opportunity costs when evaluating alternatives.

- Economists operate on the assumption that individuals are rational actors seeking to maximize their own self-interest.

- The discipline focuses on marginal decision-making, where individuals evaluate the consequences of small changes in activity levels.

- Economic theory suggests that as the cost of alternatives changes, individual behavior changes in predictable ways.

- The economic perspective forces a systematic evaluation of the value of foregone opportunities in every decision.

A rainy day could change the opportunity cost of reading a good book; we might expect more reading to get done in bad than in good weather.

The Logic of Economic Choice

- Economists define human motivation as the pursuit of maximum value for a specific objective within given constraints.

- The assumption of self-interest does not equate to selfishness; it includes any activity that provides personal satisfaction, such as charitable giving.

- Predictive modeling in economics relies on the premise that firms aim to maximize profit and consumers aim to maximize satisfaction.

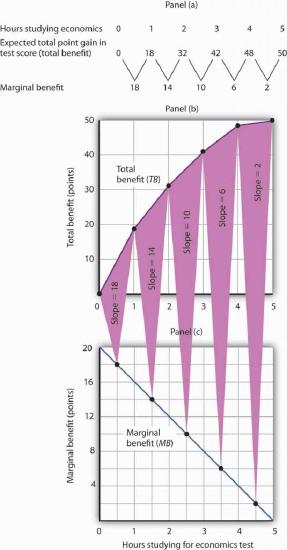

- Most economic decisions occur 'at the margin,' meaning individuals decide to do a little more or a little less of an activity rather than making all-or-nothing choices.

- The marginal perspective explains why price increases can reduce the consumption of necessities like water, as users adjust usage at the edges of their habits.

- The core principles of opportunity cost, maximization, and marginalism form the foundation of both microeconomics and macroeconomics.

The margin is the current level of an activity. Think of it as the edge from which a choice is to be made.

Microeconomics vs Macroeconomics

- Microeconomics examines the specific choices of individual consumers and firms and their effects on particular markets.

- Macroeconomics analyzes aggregate economic activity, including total output, national inflation rates, and overall unemployment.

- While both branches study markets, microeconomics views them as an end in themselves, whereas macroeconomics uses them to explain broad national trends.

- The economic way of thinking is a versatile tool applicable to diverse fields beyond traditional financial roles.

- Professional economists are primarily employed by government agencies, followed by private business firms and academic institutions.

- Economics majors enjoy a broader distribution of career paths compared to more specialized degrees like accounting or engineering.

Why do tickets to the best concerts cost so much? How does the threat of global warming affect real estate prices in coastal areas? Why do women end up doing most of the housework?

The Versatility of Economics

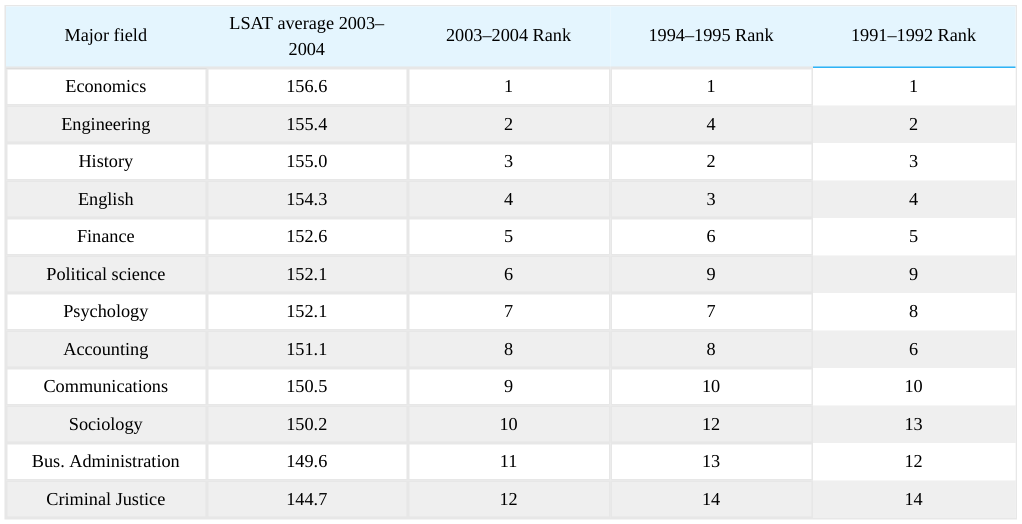

- Studying economics provides a significant advantage for students pursuing law school by sharpening essential analytical skills.

- Data from 1991 to 2004 consistently shows that economics majors achieve the highest average LSAT scores among all major undergraduate fields.

- The success of economics students is likely a combination of the field attracting naturally analytical minds and the curriculum further developing those traits.

- Beyond law, an economics background serves as a foundation for high-level research positions and competitive roles in business and industry.

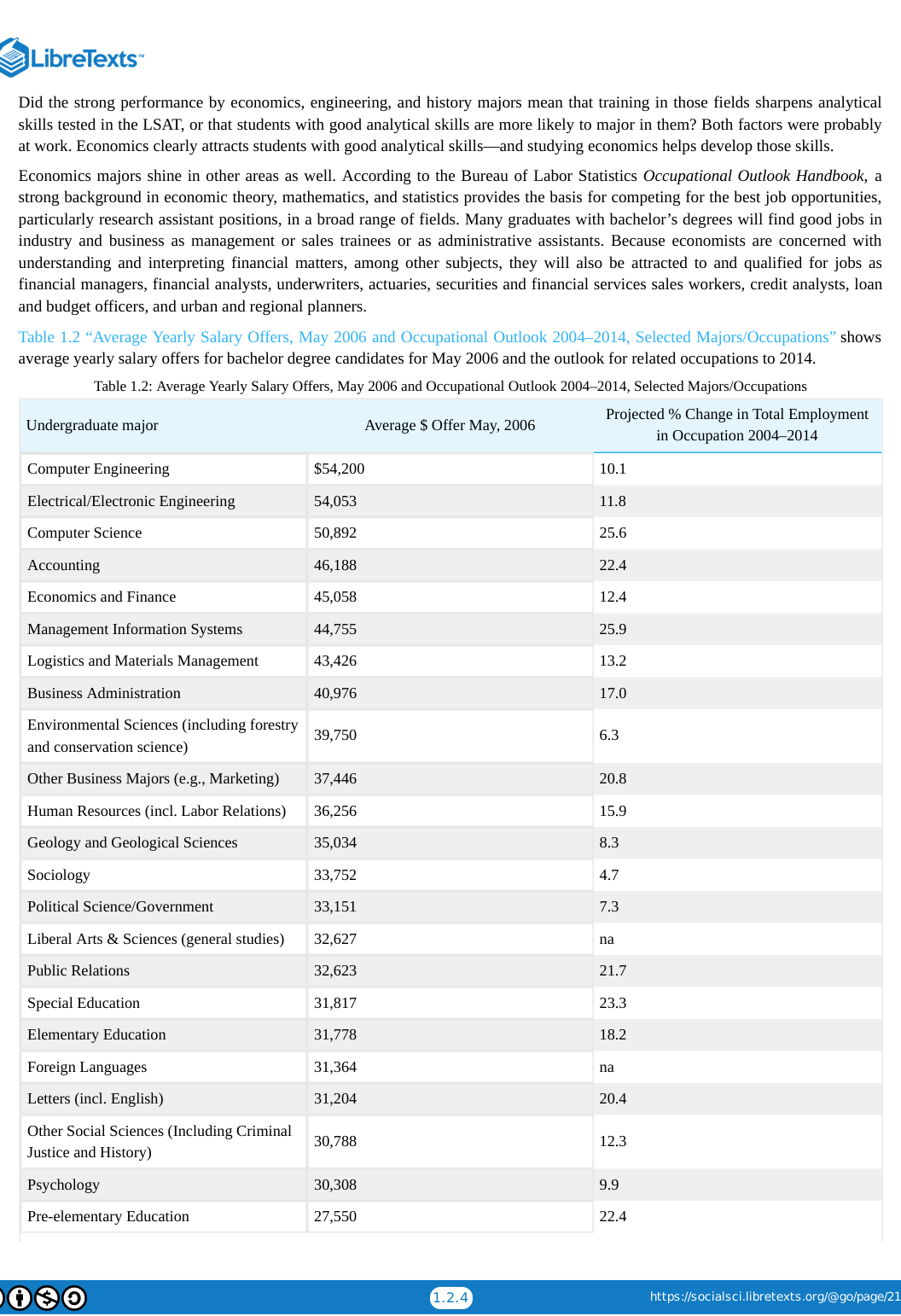

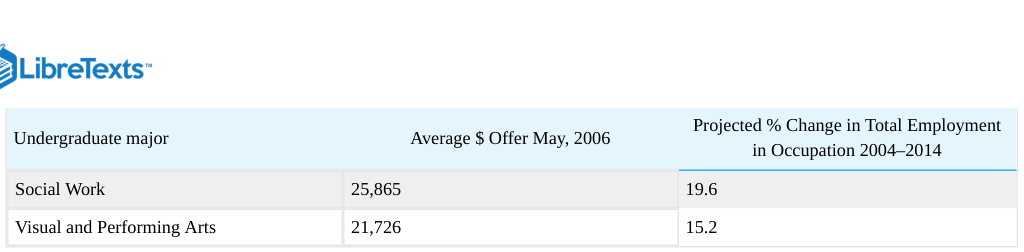

- Economics and finance graduates command strong starting salaries, averaging over $45,000 as of 2006, with steady projected job growth.

- The major qualifies individuals for diverse specialized roles including actuaries, financial analysts, urban planners, and underwriters.

In rankings for all three years, economics majors recorded the highest scores.

Economics and Career Prospects

- A statistical comparison of undergraduate majors shows significant variance in starting salaries and projected job growth across disciplines.

- While earnings are a factor, the text emphasizes that major selection is also driven by personal interests, abilities, and the pursuit of satisfaction.

- The concept of opportunity cost is central to the decision-making process when choosing a field of study like economics.

- Economics is defined by three core assumptions: the consideration of opportunity costs, the maximization of self-interest, and marginal decision-making.

- The field is fundamentally divided into two primary branches: microeconomics and macroeconomics.

What is your opportunity cost of pursuing study of economics? Does studying more economics serve your interests and will doing so maximize your satisfaction level?

The Financial Payoff of Economics

- Economics majors consistently earn higher salaries than graduates in most other fields, including business administration and natural sciences.

- The financial advantage of an economics degree persists even for those who pursue graduate studies like an MBA or a law degree.

- Data suggests economics majors outperform all other common pre-law majors in terms of post-graduation wages.

- While some attribute high earnings to student intelligence, the fact that economics majors outearn physics majors suggests the specific 'economic way of thinking' is what the market rewards.

- Economics graduates are highly versatile, finding employment across a wide range of occupations, particularly in management positions.

This finding lends some credence to the notion that the marketplace rewards training in the economic way of thinking.

Microeconomics and Opportunity Cost

- The cost of raising a child involves both direct expenditures and the economic concept of opportunity cost.

- Standard estimates include housing, food, and education but often omit the value of time spent on childcare.

- Long-term financial planning must account for extended support of adult children over the age of 21.

- Microeconomic analysis specifically examines these types of individual household choices and trade-offs.

- The field of economics relies on the 'ceteris paribus' assumption to isolate variables when testing hypotheses.

- Economists distinguish between positive statements of fact and normative statements of value.

An economist would add the value of the best alternative use of the additional time that will be required for the child.

The Scientific Method in Economics

- Economics is distinguished by its focus on opportunity cost, self-interest maximization, and marginal analysis.

- The scientific method serves as a systematic framework for creating knowledge through the testing of falsifiable hypotheses.

- A hypothesis must be an assertion of a relationship between variables that is capable of being proven false through testing.

- Hypotheses that survive rigorous, widespread testing and gain general acceptance evolve into theories and eventually laws.

- Scientific laws represent high levels of confidence but can never be considered definitively proven true, as new evidence may always emerge.

There is always a possibility that someone may find a case that invalidates the hypothesis. That possibility means that nothing in economics, or in any other social science, or in any science, can ever be p r o v e n true.

Economic Models and Hypotheses

- Scientific thought relies on models which are deliberate simplifications of a reality too complex for the human mind to process.

- Economic models use intentionally false assumptions, such as an economy producing only two goods, to improve conceptual understanding.

- Graphs serve as a primary tool for economists to represent these theoretical models and generate testable hypotheses.

- Testing economic hypotheses requires empirical data, but raw observations can often appear to contradict theoretical predictions.

- The 'ceteris paribus' assumption is critical because it isolates the relationship between two variables by assuming all other factors remain unchanged.

- Apparent contradictions in data, such as rising gas prices alongside rising consumption, often stem from multiple variables shifting simultaneously.

A model of the real world cannot b e the real world.

Economic Causality and Challenges

- Economic analysis is complicated by the fact that multiple variables, such as income and population, often change simultaneously.

- Unlike laboratory sciences, economics operates in the real world where controlled experiments are rarely possible.

- The fallacy of false cause occurs when researchers incorrectly assume one variable causes another simply because they move together.

- Economists use complex statistical methods to isolate the impact of single events, though absolute certainty remains elusive.

- Despite the inability to prove causation definitively, theoretical frameworks and extensive testing provide high confidence in economic propositions.

We cannot ask the world to stand still while we conduct experiments in economic phenomena.

Positive and Normative Economics

- Positive statements are assertions of fact or hypotheses that can be tested and potentially proven false through investigation.

- Normative statements are based on value judgments and opinions, making them impossible to prove or disprove through scientific testing.

- Disagreements in economics often persist because they are rooted in differing personal values rather than conflicting data.

- The scientific method in economics is limited by the inability to prove a hypothesis true; researchers can only fail to prove it false.

- Correlation does not equal causation, as seen in the 'fallacy of false cause' where an underlying factor may drive two seemingly related conditions.

Because no test exists for these values, these two economists will continue to disagree, unless one persuades the other to adopt a different set of values.

The Economists' Tool Kit

- Scarcity forces choices because selecting one alternative necessitates giving up another, creating an opportunity cost.

- Economics is defined by its focus on opportunity costs, maximizing behavior, and marginal analysis.

- Microeconomics examines individual and market-level choices, while macroeconomics analyzes aggregate outcomes like employment and inflation.

- The scientific method in economics relies on testing hypotheses that can be refuted but never definitively proven.

- Models simplify real-world complexity through assumptions to generate testable hypotheses about economic behavior.

- Positive statements are testable facts or hypotheses, whereas normative statements are untestable value judgments.

The data are consistent with the hypothesis, but it is never possible to prove that a hypothesis is correct.

Economic Principles and Scarcity

- The text presents exercises to distinguish between normative statements, which express values, and positive statements, which describe factual relationships.

- It explores the fundamental concept of scarcity by questioning if doubling the hours in a day would eliminate the time constraint on human activity.

- Opportunity cost is examined through the lens of higher education, specifically why younger individuals are more likely to pursue degrees than older ones.

- The material addresses the 'fallacy of false cause' and the 'ceteris paribus' problem when testing economic and scientific hypotheses.

- It discusses the validity of using idealized models, such as a perfect vacuum in physics, despite their reliance on technically incorrect assumptions.

- The section introduces the 'Production Possibilities Model' as a framework for understanding how societies make choices under conditions of scarcity.

What if the quantity of time were increased, say to 48 hours per day, and everyone still lived as many days as before. Would time still be scarce?

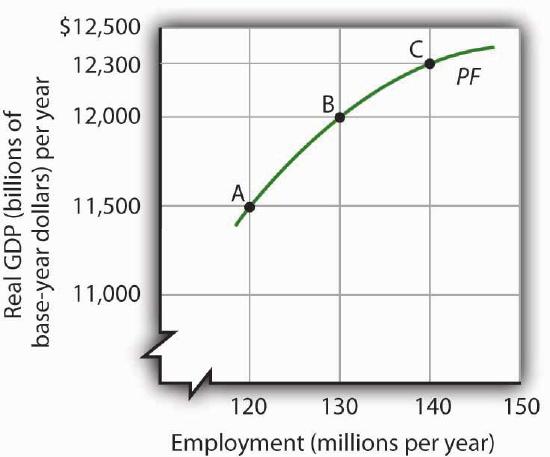

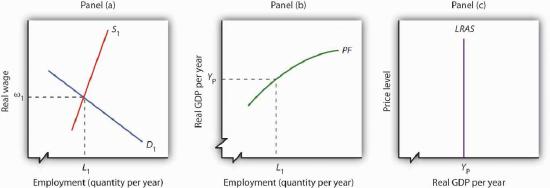

The Factors of Production

- The three primary factors of production—labor, capital, and natural resources—are the essential building blocks used to create goods and services.

- The ultimate goal of utilizing these resources is to create utility, which is the value or satisfaction people derive from consumption.

- Labor encompasses both physical human effort and human capital, which consists of the skills gained through education and experience.

- Capital is defined specifically as a factor of production that has itself been produced for the purpose of creating other goods and services.

- The total labor capacity of an economy can be expanded by either increasing the number of workers or enhancing their human capital through training.

- Technology and entrepreneurs serve as the catalysts that organize and put these fundamental factors of production to work.

Ultimately, then, an economy’s factors of production create utility; they serve the interests of people.

Defining Capital and Natural Resources

- Capital is defined as any produced resource used to create other goods and services, ranging from ancient stone tools to modern software and symphonies.

- A critical distinction is made between physical or intellectual capital and financial capital; money itself is not capital because it cannot directly produce goods.

- Natural resources must exist in nature without human alteration and require human knowledge to be transformed into productive assets.

- The status of a substance as a resource is fluid, as seen with oil, which was once a nuisance until technological refinement gave it utility.

- Natural resources include aesthetic and environmental value, such as wilderness areas that provide utility through beauty rather than raw materials.

- The availability of natural resources can be expanded through new discoveries, new applications for existing materials, or improved extraction methods.

Pennsylvania farmers in the eighteenth century who found oil oozing up through their soil were dismayed, not delighted.

Drivers of Economic Production

- Technology and entrepreneurship are the primary forces that organize factors of production to create goods and services.

- Entrepreneurs in market economies drive innovation by seeking profit through the reorganization of resources.

- In non-market economies, bureaucrats fulfill the entrepreneurial role but respond to incentives other than profit.

- The continuous introduction of new technologies by entrepreneurs fundamentally alters how labor is performed across all sectors.

- Factors of production are categorized into labor, capital, and natural resources, with human capital being a key variable in labor quality.

We can dispute whether all the changes have made our lives better. What we cannot dispute is that they have made our lives different.

Technology and Economic Productivity

- Advanced mapping and drilling technologies have reduced the cost of discovering oil from $20 to under $5 per barrel.

- Logistics technology, such as handheld inventory computers, allows companies like PepsiCo to optimize delivery routes and reduce fleet requirements.

- In the dairy industry, electronic milkers and computer monitoring have increased milk output per cow by 50% over two decades.

- Technological progress generally benefits consumers through lower prices and workers through higher wages linked to productivity.

- While technology drives overall economic growth and profit, it also leads to job displacement and the obsolescence of certain firms.

- The Mars oil platform exemplifies the scale of modern engineering, standing 300 feet above water with tendons reaching 3,000 feet deep.

The name Mars reflects its otherworld appearance—it extends 300 feet above the water’s surface and has steel tendons that reach 3,000 feet to the floor of the gulf.

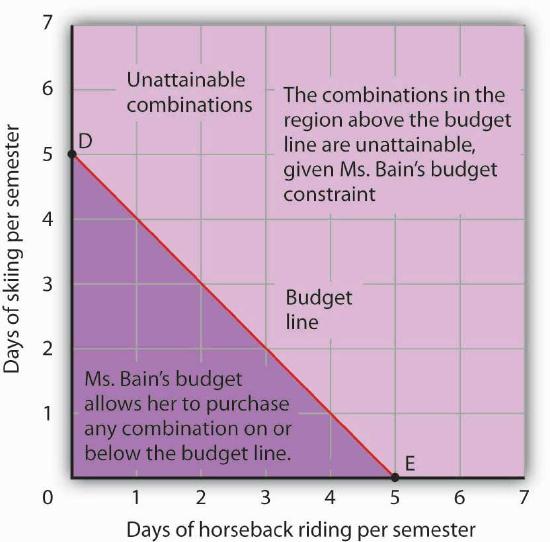

Defining Capital and Production Possibilities

- Distinguishes between natural resources and capital by highlighting that human intervention or extraction transforms raw materials into capital.

- Identifies diverse examples of capital ranging from campus libraries and power plants to the White House and national park facilities.

- Introduces the production possibilities curve as a graphical tool to represent the trade-offs between two specific goods or services.

- Explains that the model assumes fixed technology and a limited quantity of factors of production to illustrate scarcity.

- Outlines how the model differentiates between full employment of resources and inefficient, idle factors of production.

- Connects the concepts of specialization and comparative advantage to the physical constraints of the production possibilities curve.

An untapped deposit of natural gas is a natural resource. Once extracted and put in a storage tank, natural gas is capital.

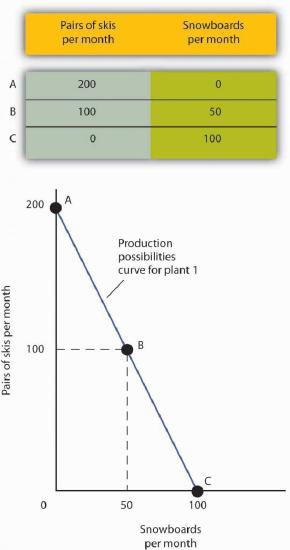

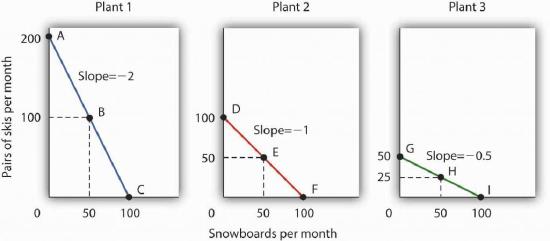

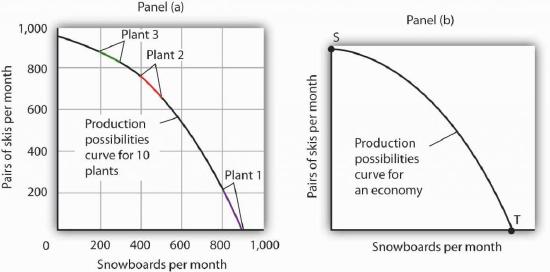

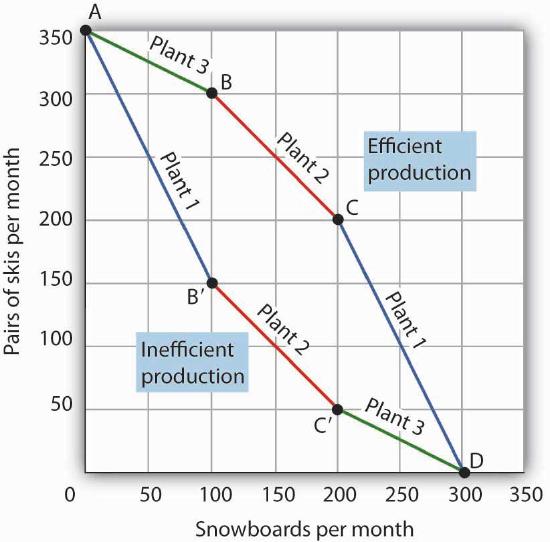

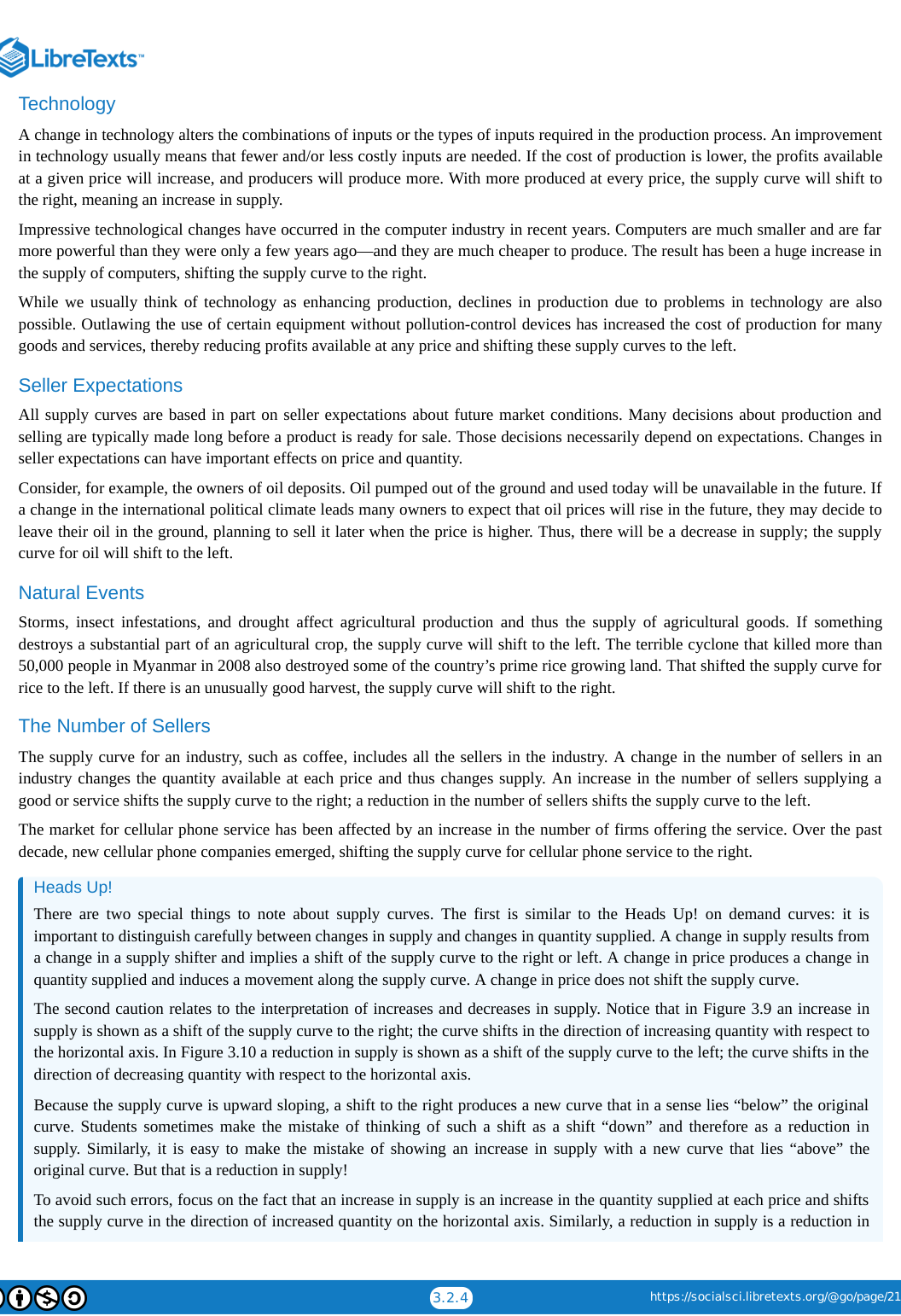

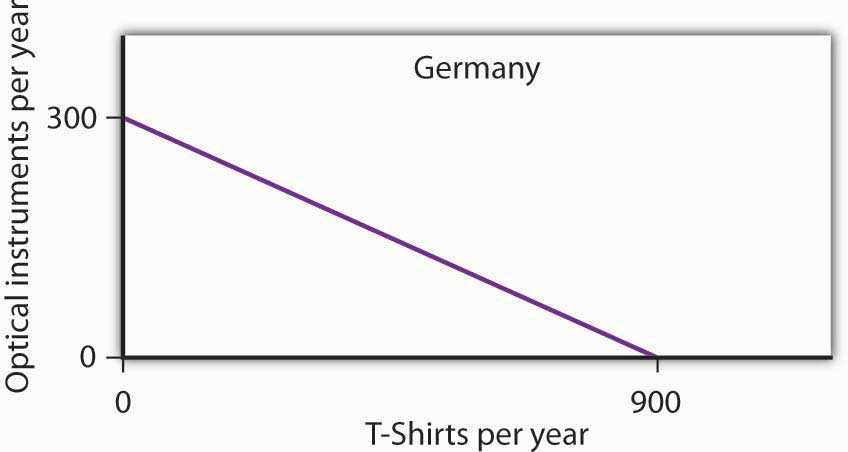

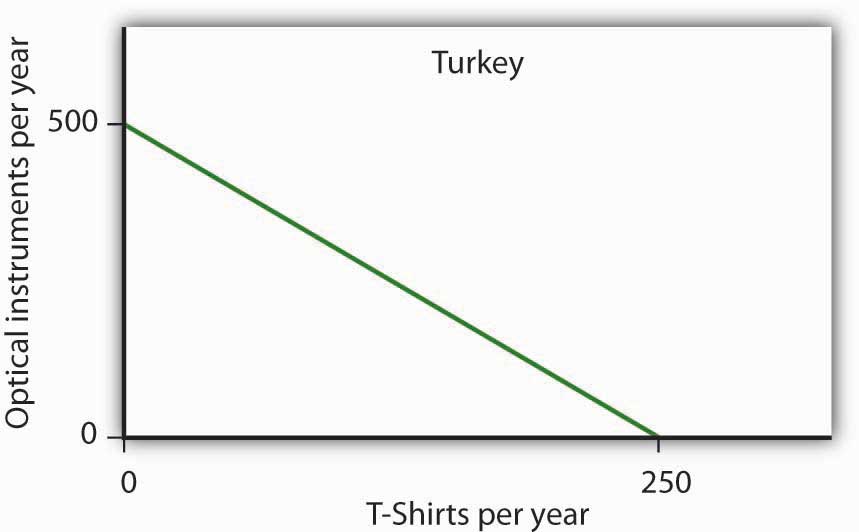

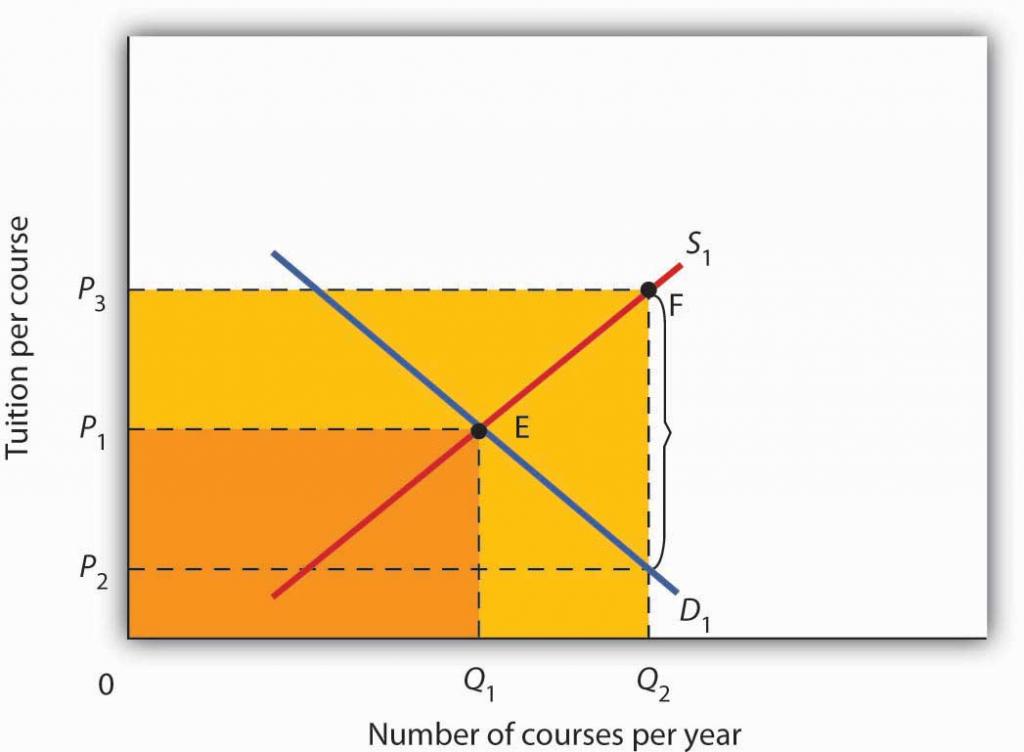

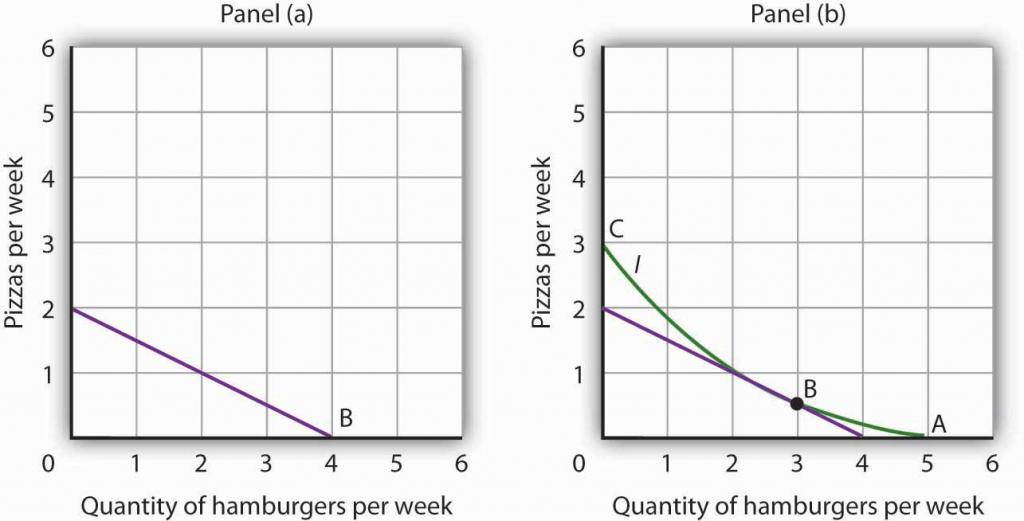

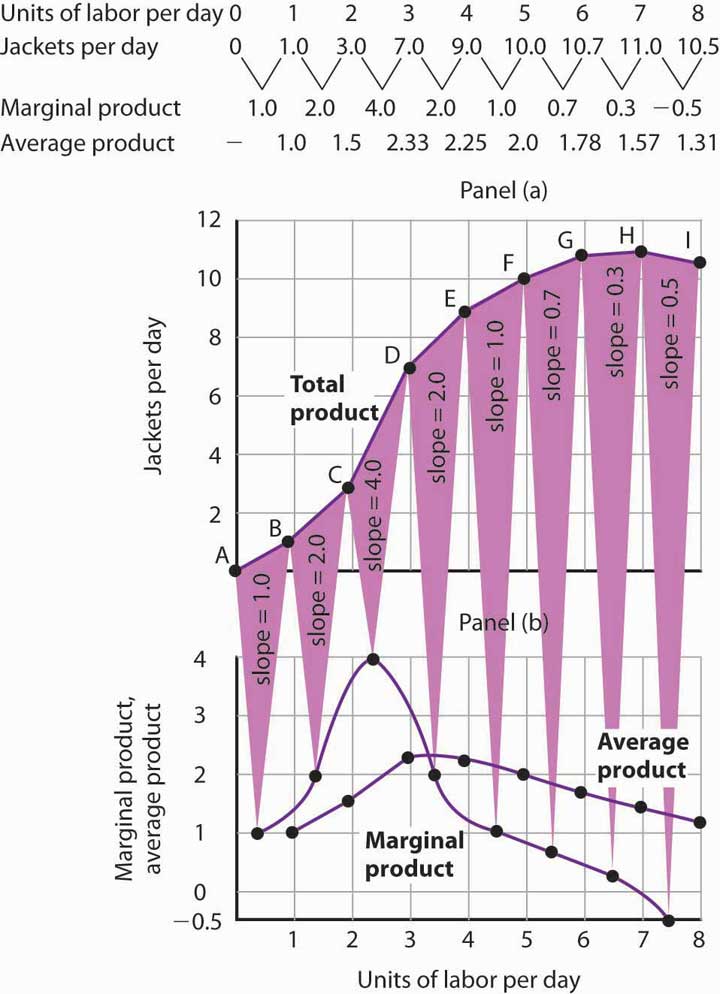

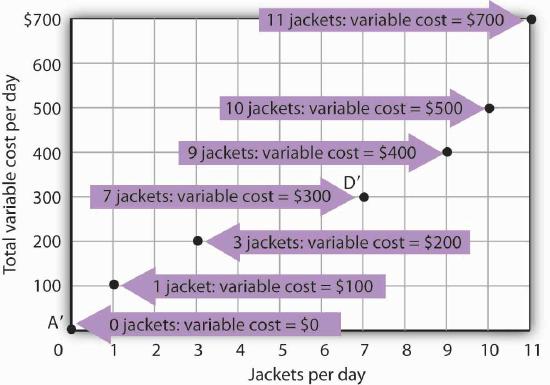

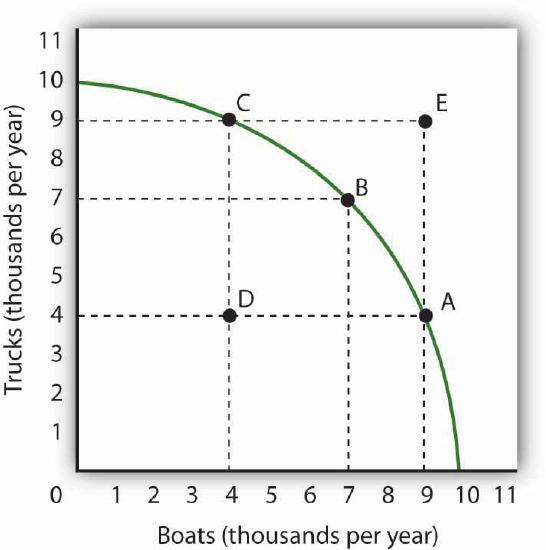

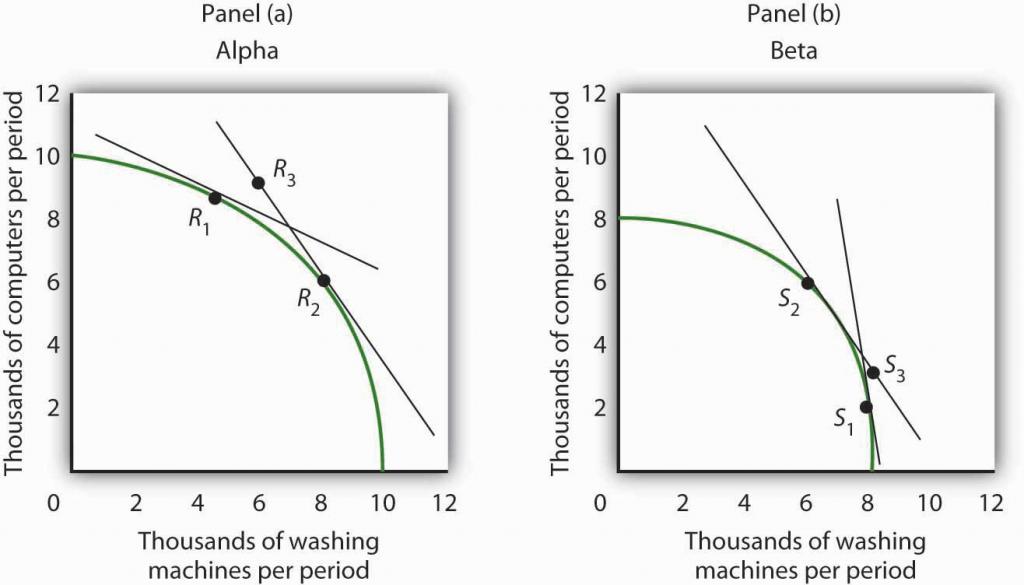

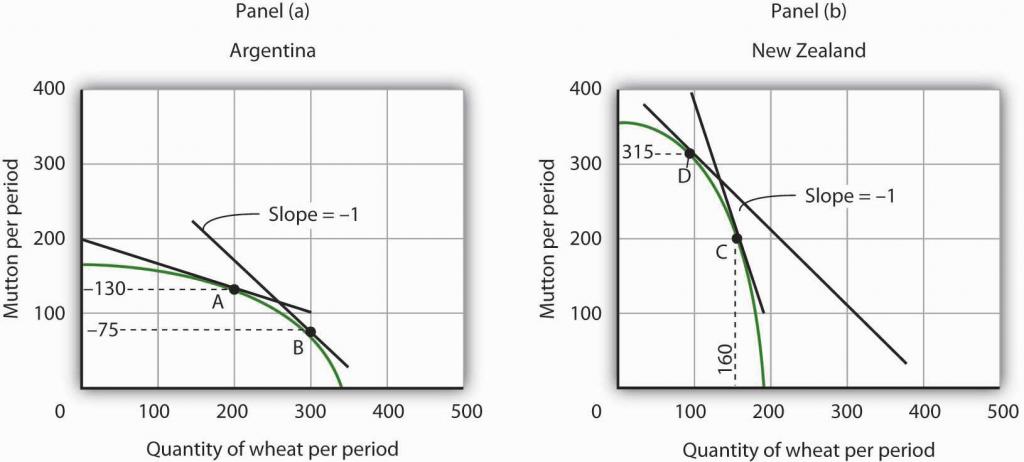

Alpine Sports Production Possibilities

- Alpine Sports serves as a model for understanding production trade-offs between two goods: skis and snowboards.

- The firm operates three distinct plants, each with different capacities and specialized designs for production.

- A production possibilities curve (PPC) illustrates the maximum output combinations given fixed resources and technology.

- The downward-sloping linear curve demonstrates a negative relationship, where increasing one product necessitates decreasing the other.

- The slope of the PPC represents the opportunity cost, specifically the rate at which one good must be sacrificed to produce another.

- Constant opportunity cost is shown through a straight-line PPC, where the trade-off ratio remains identical at all points on the curve.

The negative slope of the production possibilities curve reflects the scarcity of the plant’s capital and labor.

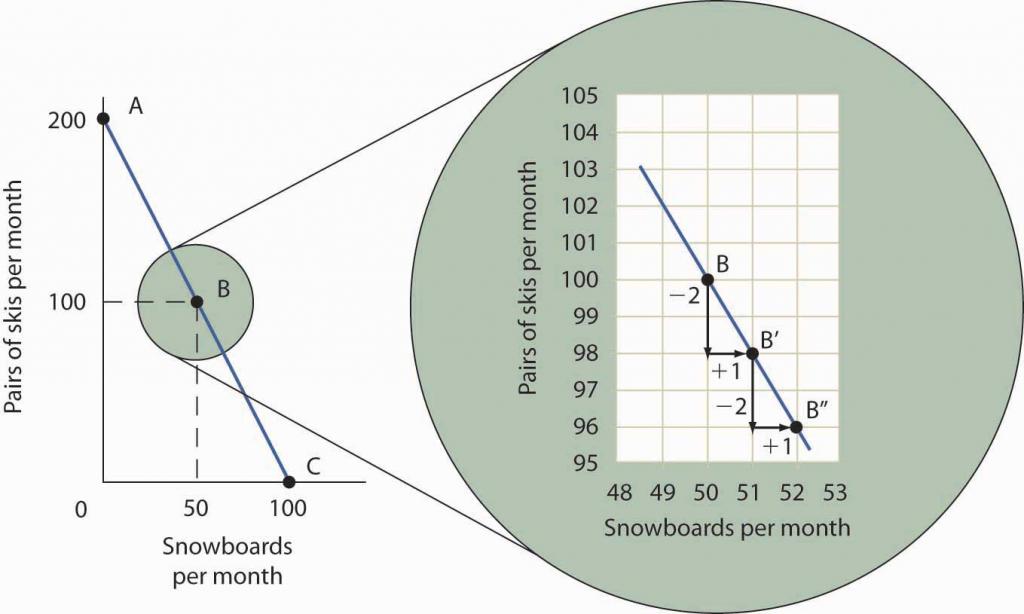

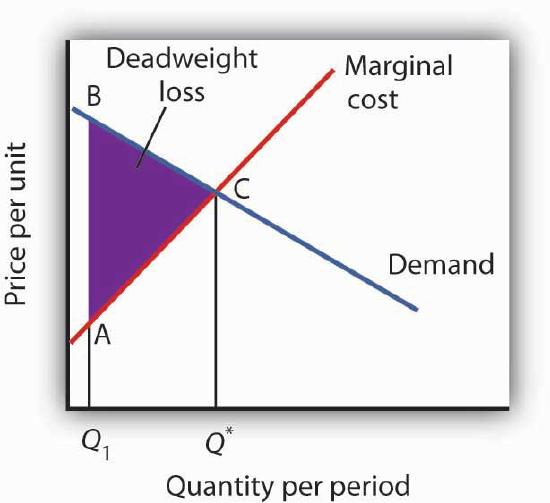

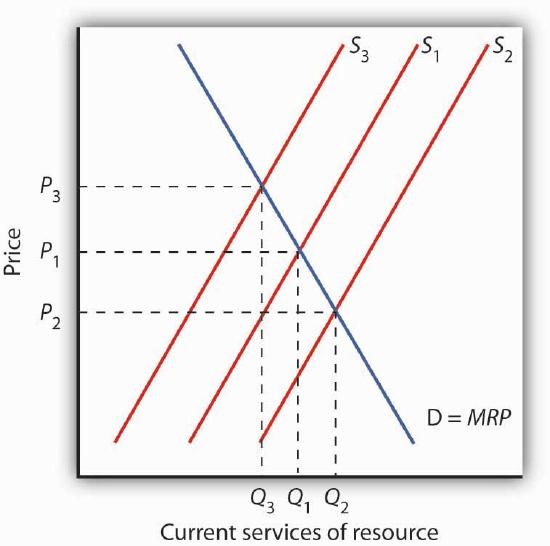

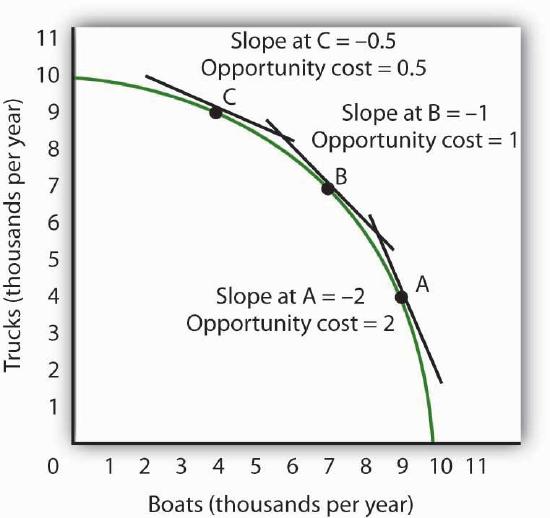

Opportunity Cost and Slope

- The absolute value of the slope of a production possibilities curve (PPC) represents the opportunity cost of producing one additional unit of the good on the horizontal axis.

- In a linear PPC, the slope remains constant, meaning the trade-off ratio between two goods like skis and snowboards does not change regardless of production volume.

- Different production facilities often have different slopes, reflecting varying levels of efficiency and resource allocation for specific products.

- The steepness of the PPC curve is a direct visual indicator of cost; a steeper curve signifies a higher opportunity cost for the good on the horizontal axis.

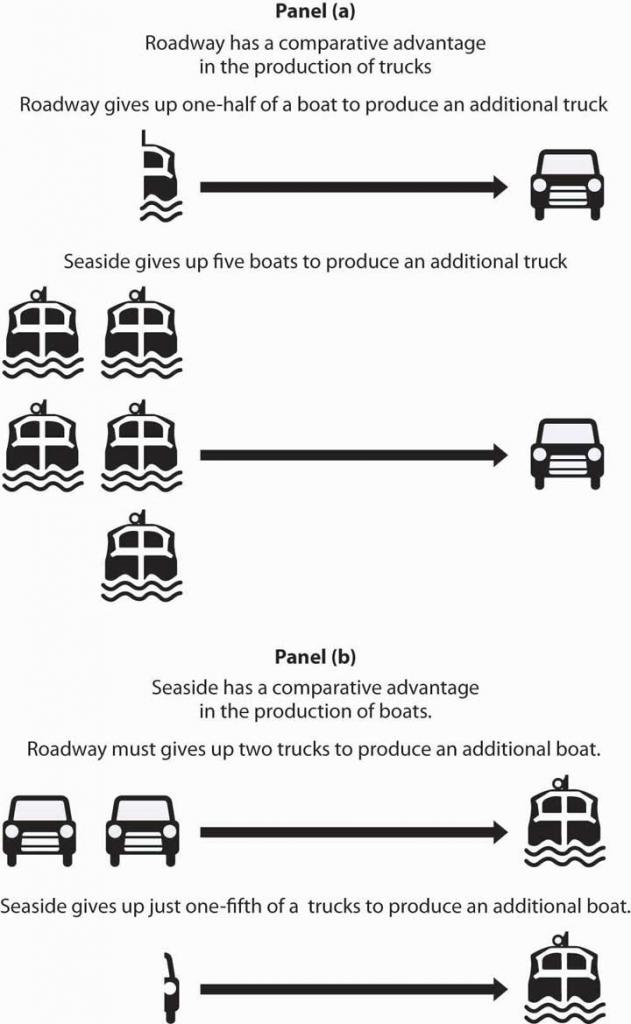

- Comparative advantage is identified by finding the plant or resource with the lowest opportunity cost, such as Plant 3 requiring only half a pair of skis per snowboard.

- To increase production of one good, resources must be freed up by reducing the production of another, a fundamental constraint of the PPC model.

The greater the absolute value of the slope of the production possibilities curve, the greater the opportunity cost will be.

Comparative Advantage and Production Curves

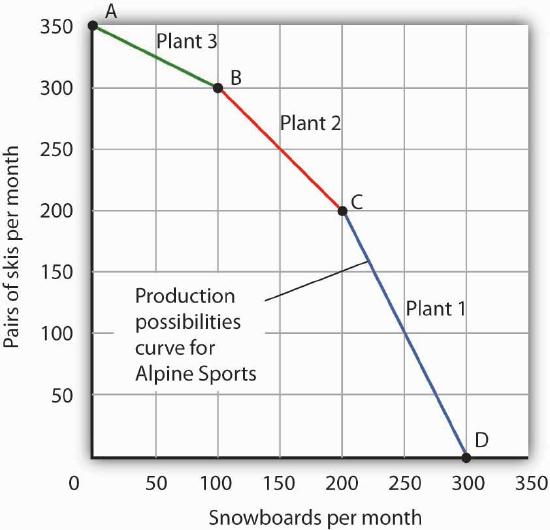

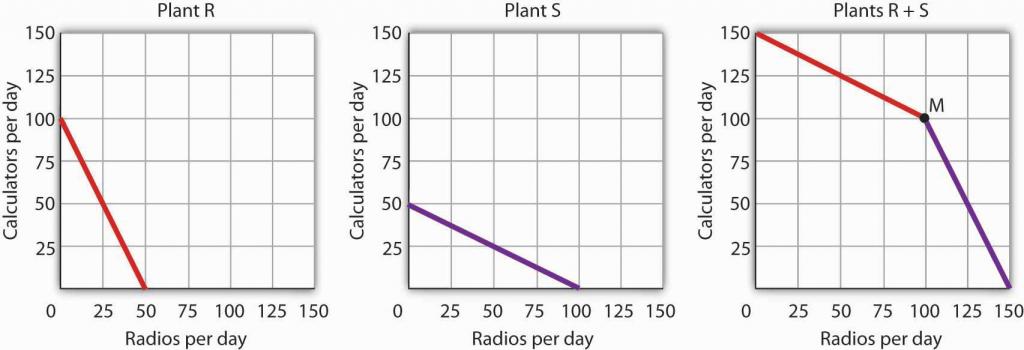

- A combined production possibilities curve is constructed by aggregating the maximum output capacities of multiple individual plants.

- When shifting production from one good to another, efficient firms prioritize plants with the lowest opportunity cost for the new product.

- Comparative advantage is defined as the ability to produce a good at a lower opportunity cost than other entities.

- A plant can possess a comparative advantage not through superior proficiency, but through a lack of efficiency in producing alternative goods.

- The sequence of shifting production across plants creates a bowed-out combined curve, reflecting increasing opportunity costs as more resources are diverted.

Comparative advantage thus can stem from a lack of efficiency in the production of an alternative good rather than a special proficiency in the production of the first good.

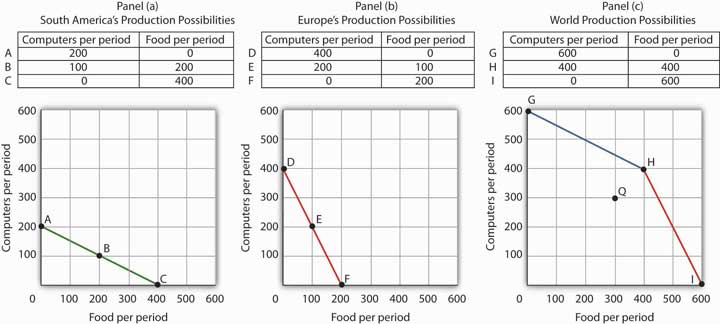

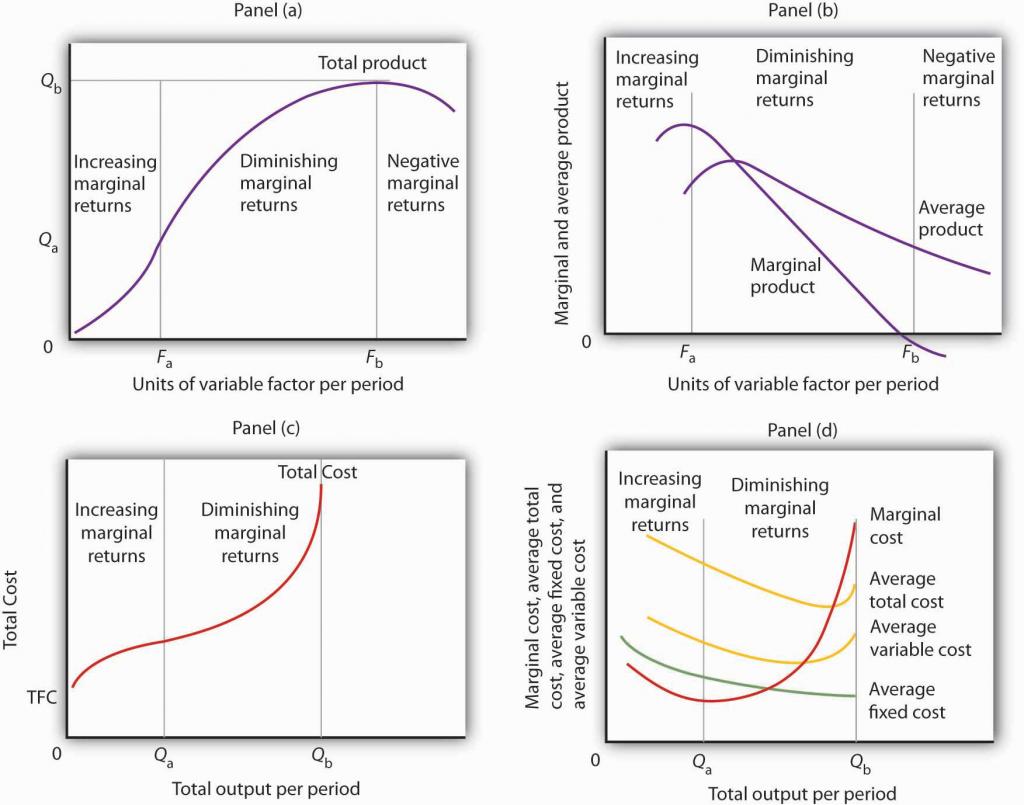

The Law of Increasing Opportunity Cost

- The production possibilities curve is constructed from linear segments representing individual assembly plants.

- The resulting curve exhibits a bowed-out shape rather than a straight line.

- The absolute value of the curve's slope increases as production shifts toward a single good.

- This shape is a direct consequence of allocating resources based on the principle of comparative advantage.

- The transition from skis to snowboards illustrates how opportunity costs change with production volume.

Notice that this production possibilities curve, which is made up of linear segments from each assembly plant, has a bowed-out shape; the absolute value of its slope increases as Alpine Sports produces more and more snowboards.

Law of Increasing Opportunity Cost

- The law of increasing opportunity cost states that as production of a specific good rises, the cost of producing additional units in terms of sacrificed alternatives also increases.

- This economic principle is visually represented by a bowed-out or concave production possibilities curve rather than a straight line.

- The curve's shape is driven by comparative advantage, as resources (like different manufacturing plants) are not equally efficient at producing all goods.

- As more production units or plants are added to a model, the production possibilities curve transitions from jagged segments into a smooth, continuous curve.

- In large-scale economies with millions of participants, economists typically use smooth, numberless curves to illustrate general production trade-offs and scarcity.

Scarcity implies that a production possibilities curve is downward sloping; the law of increasing opportunity cost implies that it will be bowed out, or concave, in shape.

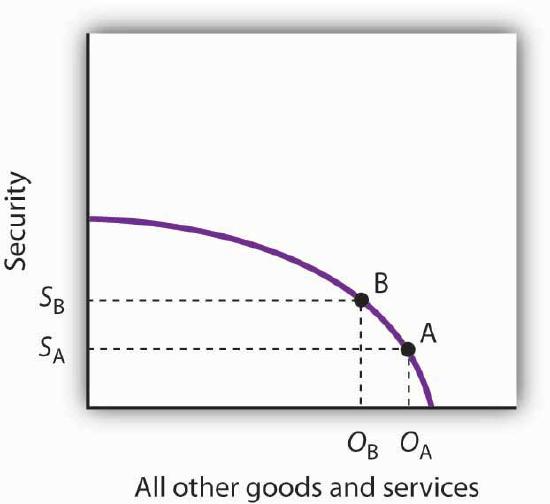

The Production Possibilities Model

- Economic models often assume production curves are smooth and 'bowed out' to represent trade-offs.

- The model simplifies reality by focusing on an economy that produces only two specific goods.

- A core assumption is that technology and available factors of production remain constant during the analysis.

- Operating on the curve implies that increasing one good's production requires reducing the other.

- The model can be applied to macro-level choices, such as balancing national security against all other goods.

In this section, we shall assume that the economy operates on its production possibilities curve so that an increase in the production of one good in the model implies a reduction in the production of the other.

The Cost of Security

- National security is treated as a category of production that competes with all other goods and services for limited resources.

- The shift toward increased security spending after 9/11 illustrates a movement along the production possibilities curve.

- Increasing security requires tangible resources, such as personnel for airport inspections and state-level counter-terrorism efforts.

- The law of increasing opportunity cost suggests that as more security is produced, the sacrifice of other goods becomes progressively larger.

- The production possibilities model identifies the trade-offs available to a nation but does not dictate which specific point on the curve is optimal.

Of course, an economy cannot really produce security; it can only attempt to provide it.

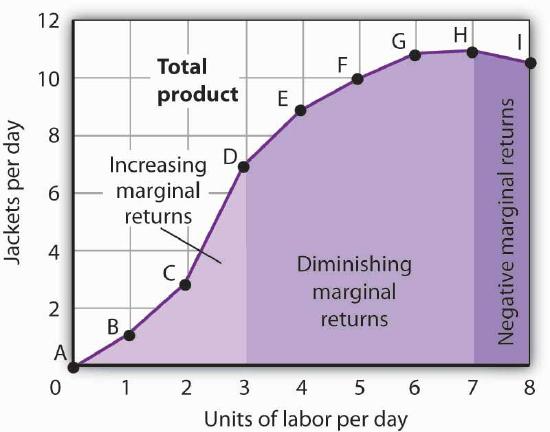

Inside the Production Curve

- Operating inside the production possibilities curve indicates an economy is failing to maximize its potential output of goods and services.

- The failure to achieve full employment of labor, buildings, or land results in a level of production that falls short of the curve.

- Beyond unemployment, an economy can underperform if it fails to allocate its resources based on the principle of comparative advantage.

- Moving from inside the curve to the boundary allows an economy to increase the production of all goods simultaneously, raising the standard of living.

- The production possibilities model highlights that job loss is not just a loss of income for workers, but a loss of tangible goods for the entire society.

Some workers are without jobs, some buildings are without occupants, some fields are without crops.

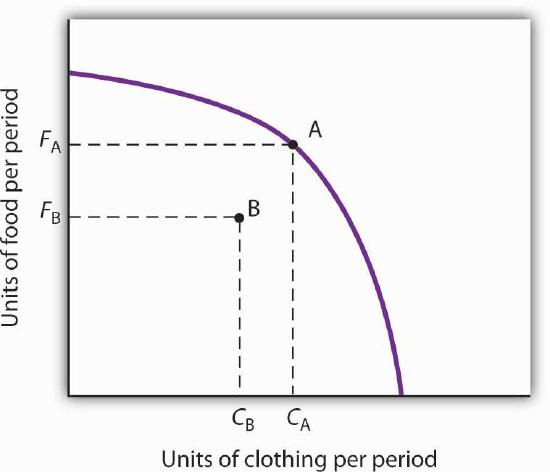

Efficiency and Comparative Advantage

- Allocating resources without considering comparative advantage results in a bowed-in production curve rather than a bowed-out one.

- Inefficient production occurs when an economy operates inside its production possibilities curve, producing fewer goods than its resources allow.

- By switching production based on comparative advantage, a firm can increase the output of all goods simultaneously without adding more labor or capital.

- Efficient production requires both the full use of available factors and the optimal allocation of those factors.

- The production possibilities curve serves as a guide for how goods should be produced to maximize societal output.

Inefficient production implies that the economy could be producing more goods without using any additional labor, capital, or natural resources.

Specialization and Comparative Advantage

- Specialization occurs when an economy produces goods and services in which it holds a comparative advantage.

- Individual workers specialize in specific fields and use their income to trade for goods produced by others with different advantages.

- The absence of specialization would lead to a drastic decline in living standards, making survival difficult for most people.

- Nations allocate resources based on land and population endowments, such as the U.S. focusing on agriculture while Hong Kong focuses on nonagricultural uses.

- The production possibilities curve is bowed outward because resources are allocated according to the law of increasing opportunity cost.

- Operating inside the production possibilities curve indicates an inefficient use of an economy's factors of production.

Imagine that you are suddenly completely cut off from the rest of the economy. You must produce everything you consume; you obtain nothing from anyone else.

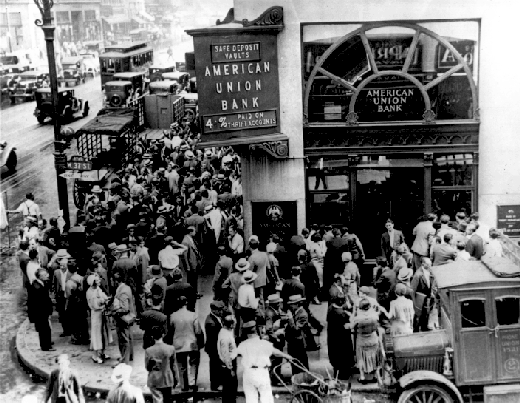

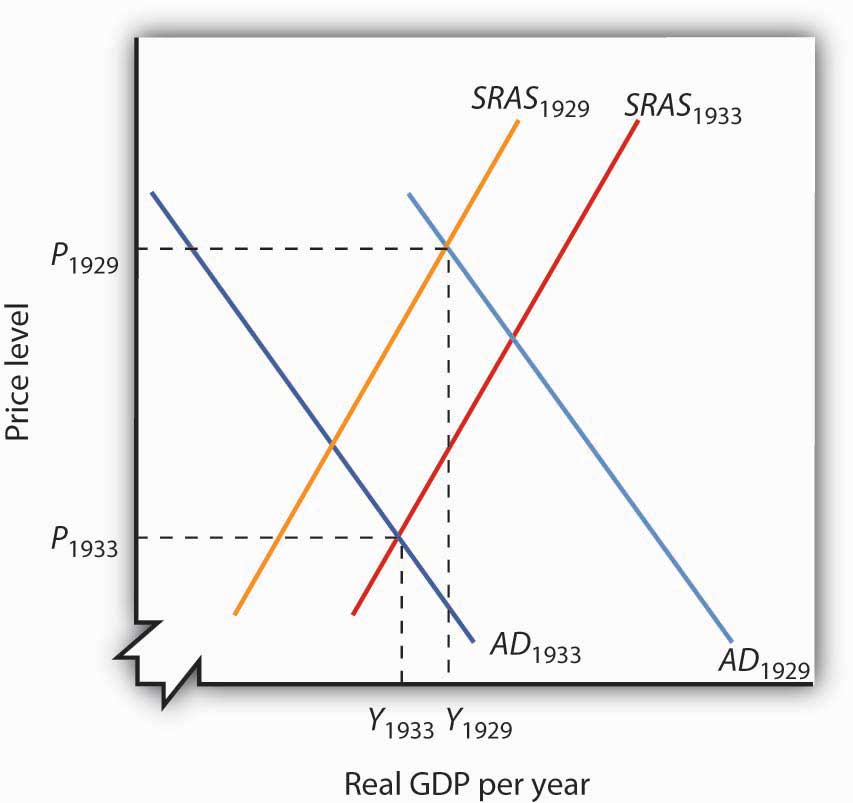

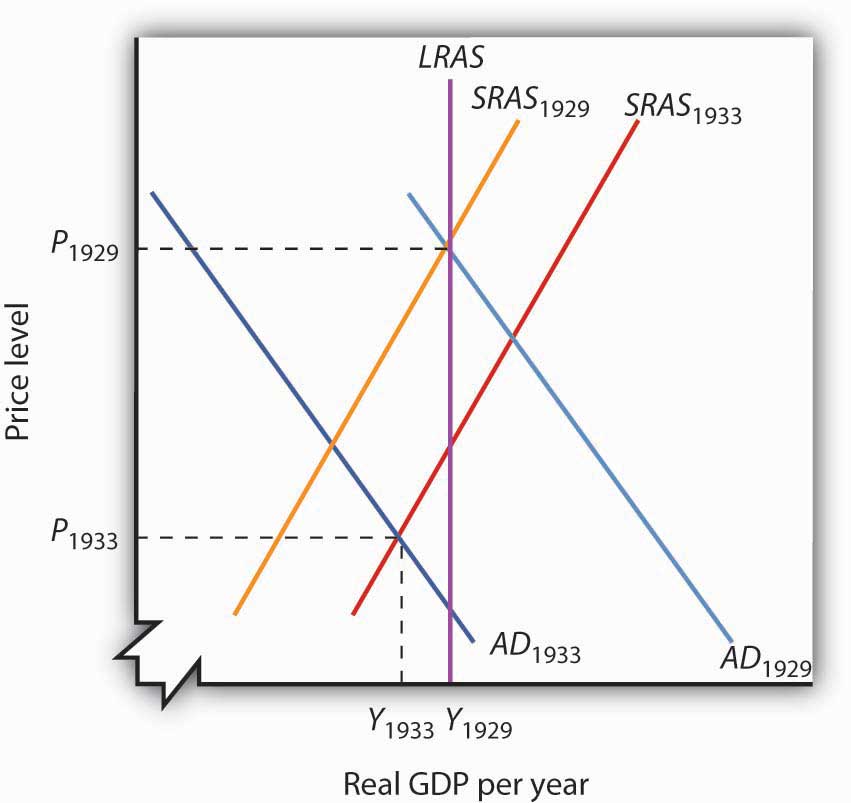

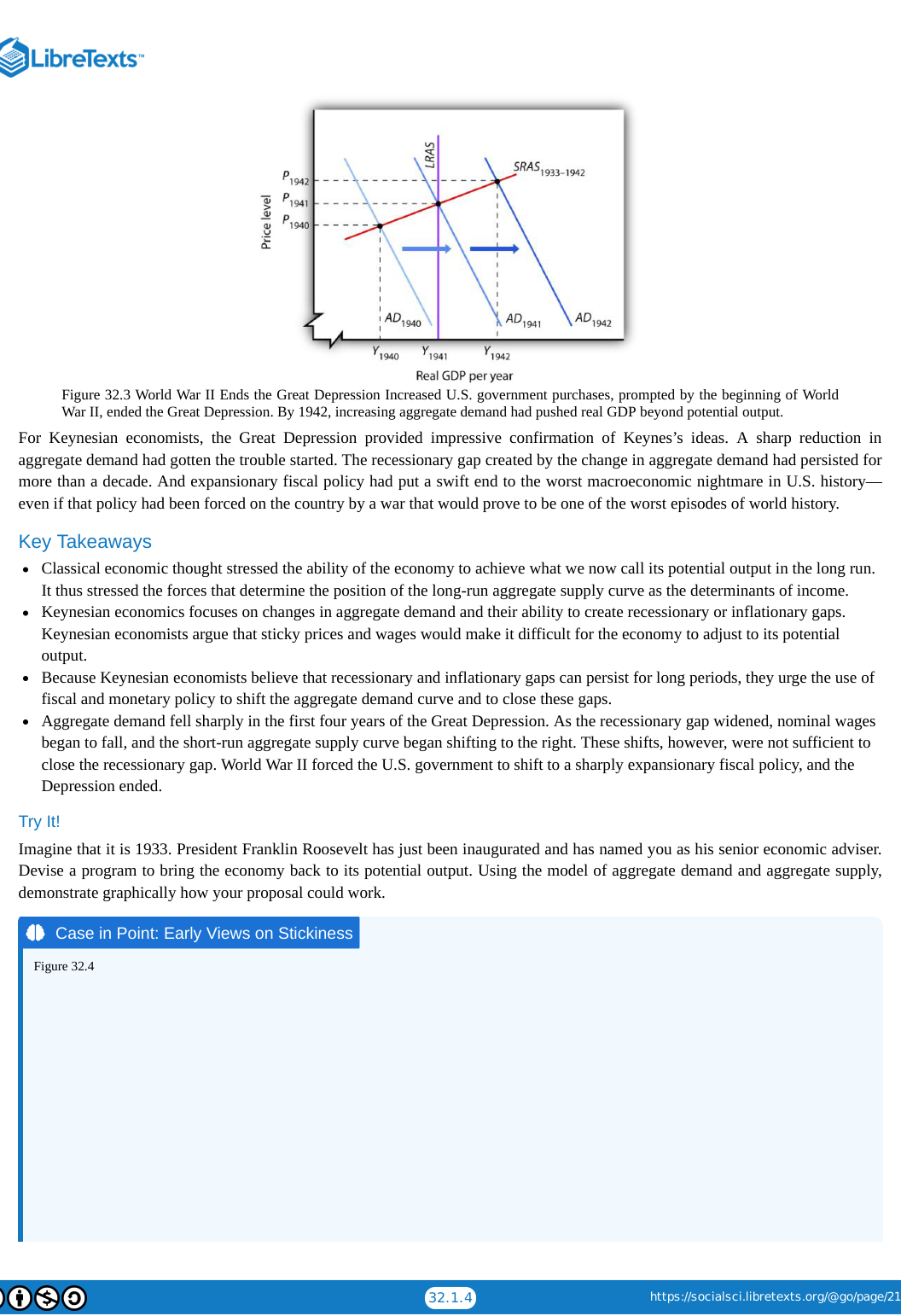

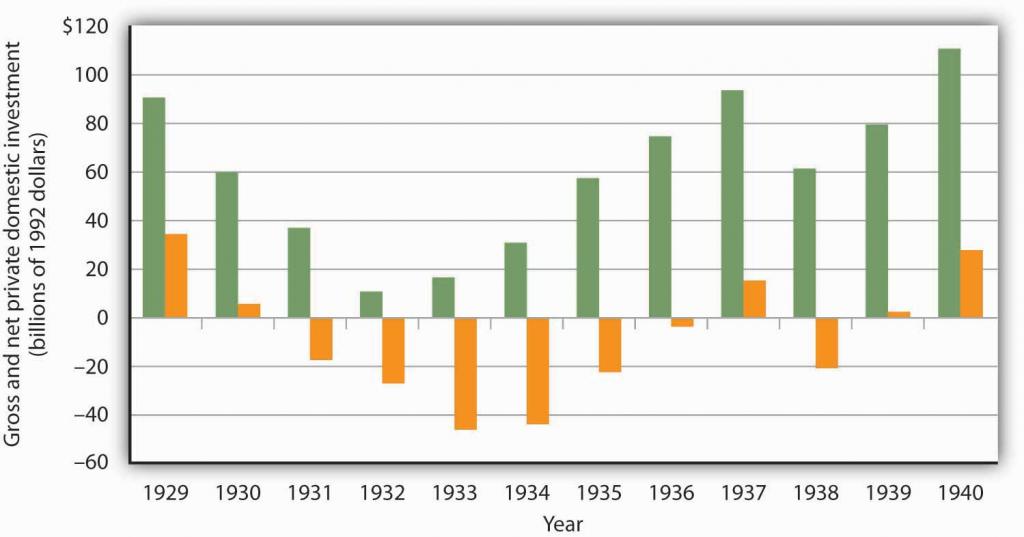

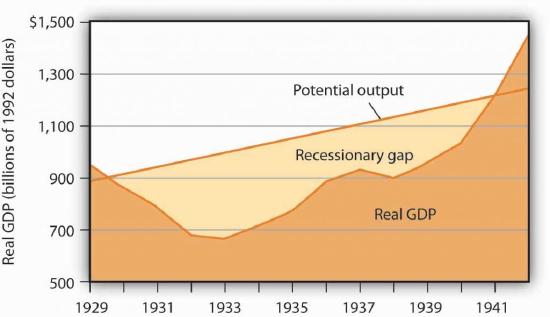

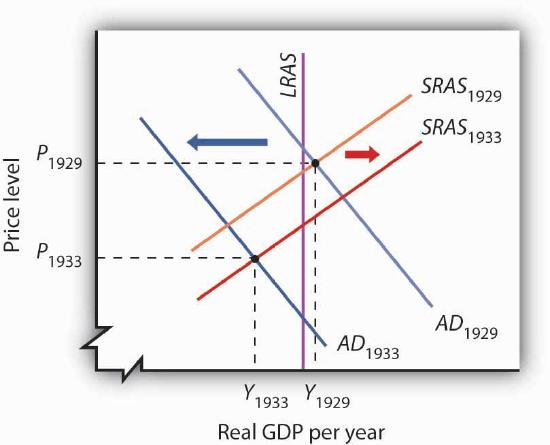

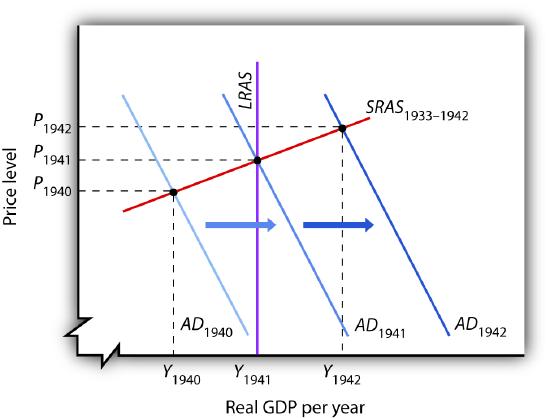

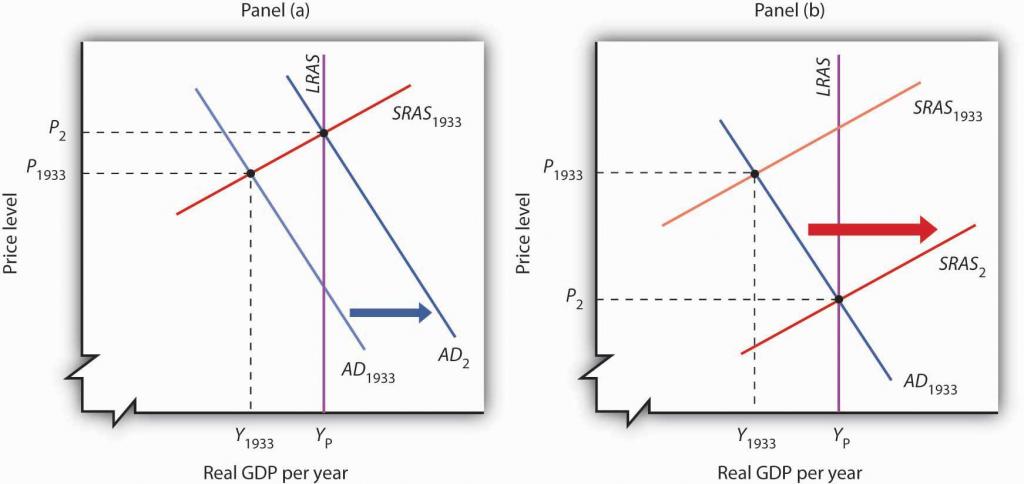

Costs of the Great Depression

- The U.S. economy transitioned from unprecedented prosperity in early 1929 to a severe contraction that left resources vastly underutilized.

- By 1933, unemployment exceeded 25% and national production had plummeted by nearly 30%, moving the economy far inside its production possibilities curve.

- Full employment of resources was not achieved again until 1942, driven by the massive mobilization required for World War II.

- The cumulative loss of goods and services between 1929 and 1942 is estimated at over $3 trillion in modern currency.

- The material cost of the output lost during the Great Depression actually exceeded the total financial cost of fighting World War II.

- The production possibilities model serves as a framework for understanding international trade, economic growth, and the efficiency of different economic systems.

In material terms, the forgone output represented a greater cost than the United States would ultimately spend in World War II.

Comparative Advantage in Trade

- Nations function like individual production plants, each possessing a unique comparative advantage in specific activities.

- Global efficiency is maximized when nations specialize in goods where they hold a comparative advantage rather than attempting self-sufficiency.

- Specialization creates a state of mutual interdependence where nations must trade their surplus for goods produced more efficiently elsewhere.

- A refusal to trade results in world production falling inside the production possibilities curve, indicating a waste of potential resources.

- Using a model of South America and Europe, the text demonstrates that free trade allows for a higher total output of both food and computers.

A failure to allocate resources in this way means that world production falls inside the production possibilities curve; more of each good could be produced by relying on comparative advantage.

The Power of Comparative Advantage

- The world production possibilities curve takes on a bowed-out shape even when individual nations have linear curves.

- Specialization based on comparative advantage allows for a higher total output of goods without requiring additional resources.

- Trade restrictions force the world to operate inside its production possibilities curve, resulting in lower overall production.

- A nation's trade policy affects the distribution of employment across sectors but does not dictate the overall level of employment.

- While trade creates enormous global benefits, it necessitates the reallocation of resources which can incur transition costs.

- Economists generally agree that free trade is desirable as it promotes greater production of goods and services for the global population.

Of course, this idealized example would have all of South America’s computer experts becoming farmers while all of Europe’s farmers become computer geeks!

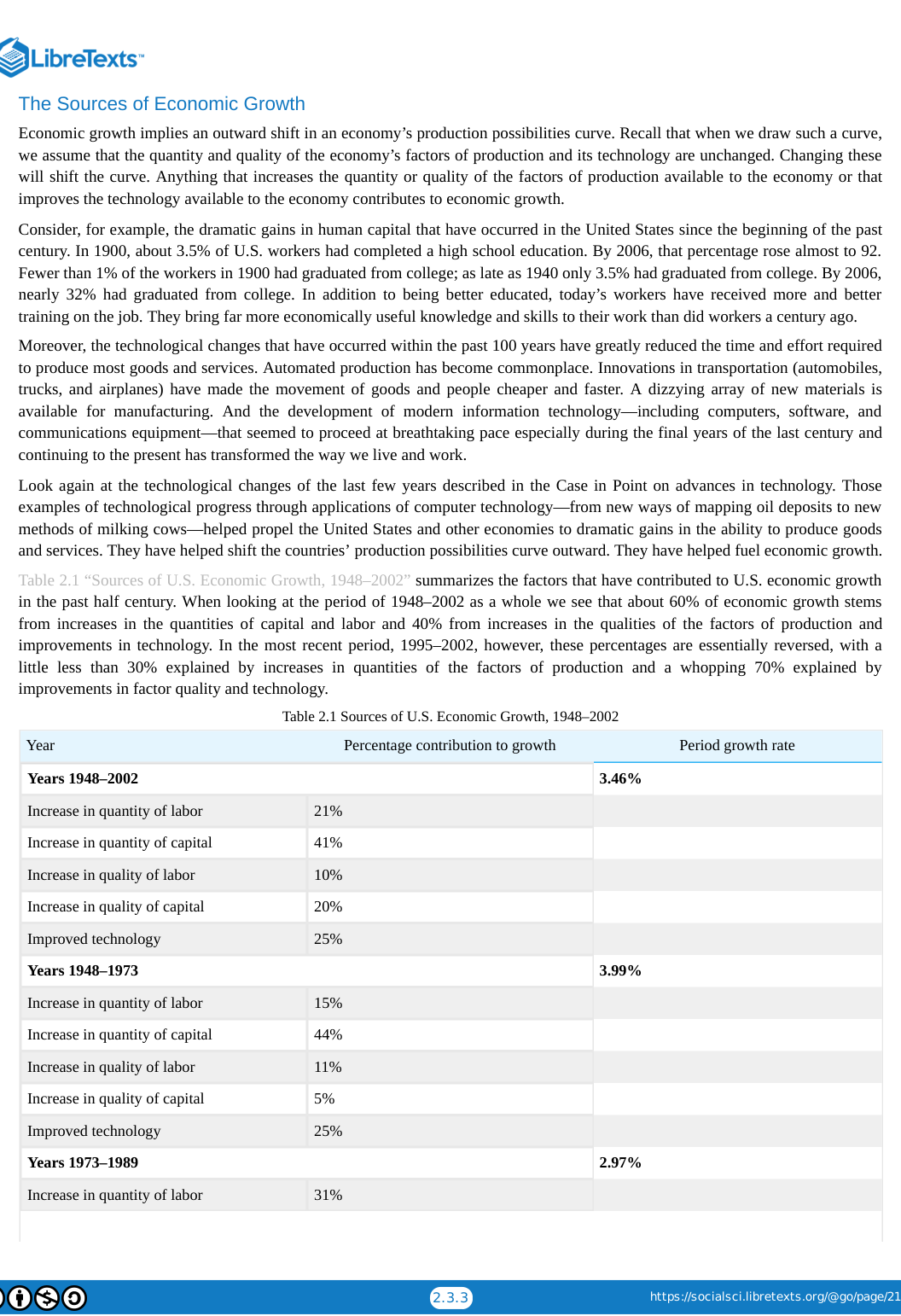

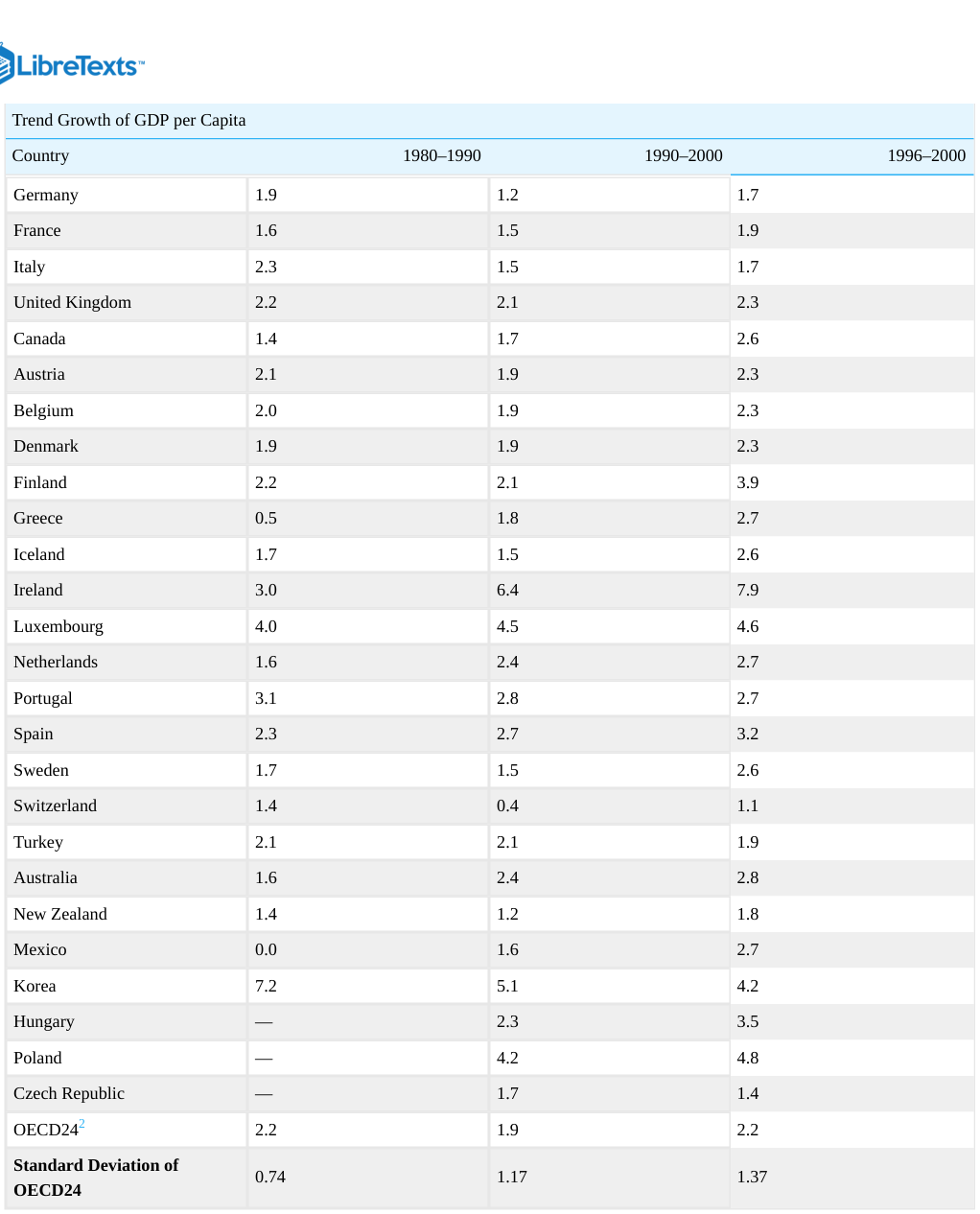

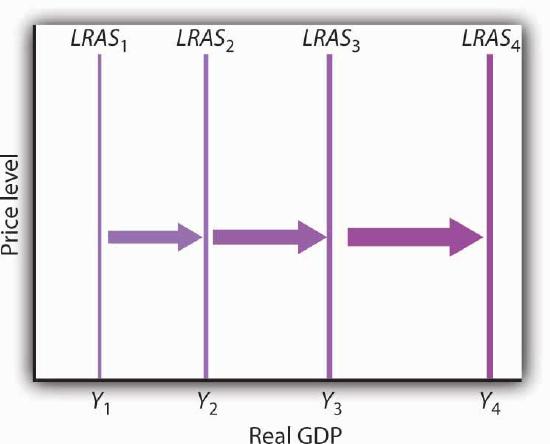

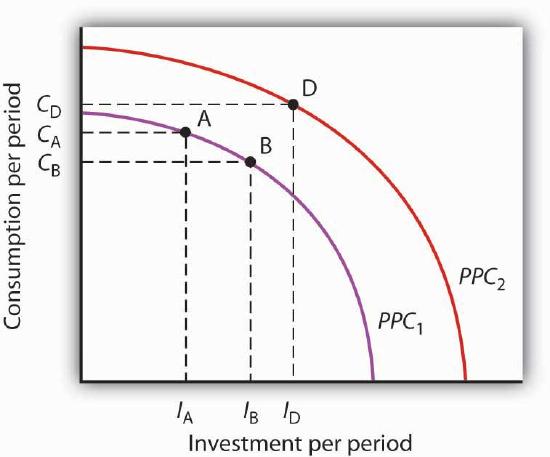

Mechanics of Economic Growth

- Economic growth is defined as an outward shift in a production possibilities curve, making previously unattainable production levels possible.

- Growth is driven by increases in the physical quantity or quality of factors of production, such as labor and capital.

- Technological gains, ranging from automated production to advanced information technology, significantly reduce the time and effort required for output.

- Human capital has seen dramatic improvements, evidenced by U.S. high school completion rates rising from 3.5% in 1900 to 92% in 2006.

- Modern innovations like computer-based oil mapping and automated milking demonstrate how technology fuels growth across diverse sectors.

The development of modern information technology—including computers, software, and communications equipment—that seemed to proceed at breathtaking pace especially during the final years of the last century and continuing to the present has transformed the way we live and work.

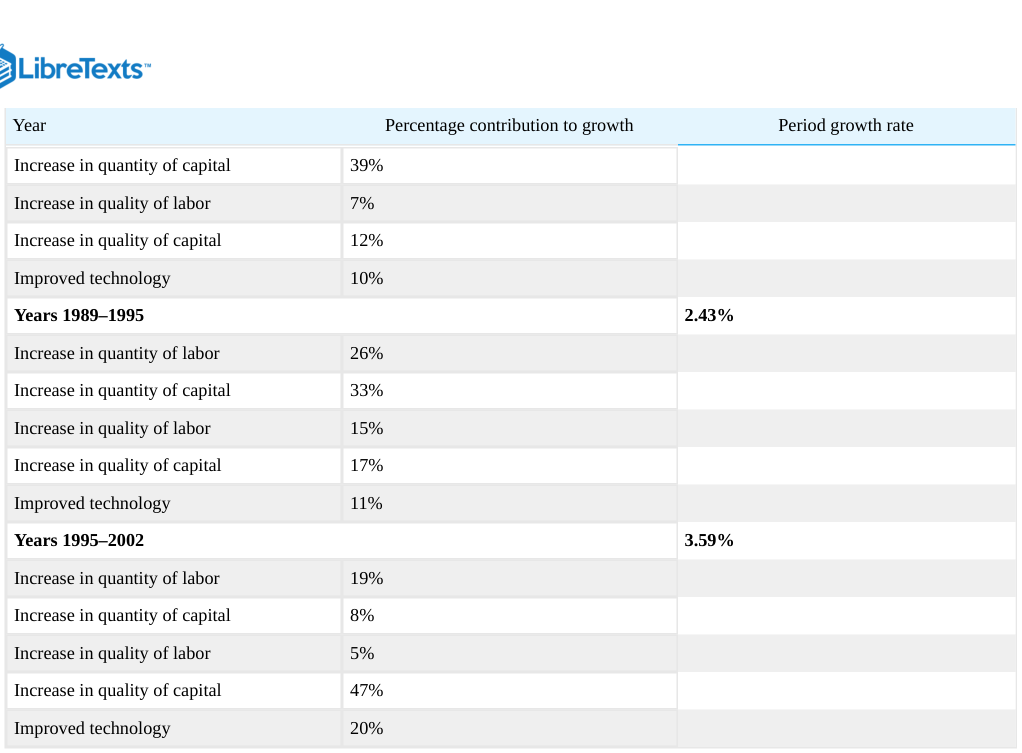

Sources of Economic Growth

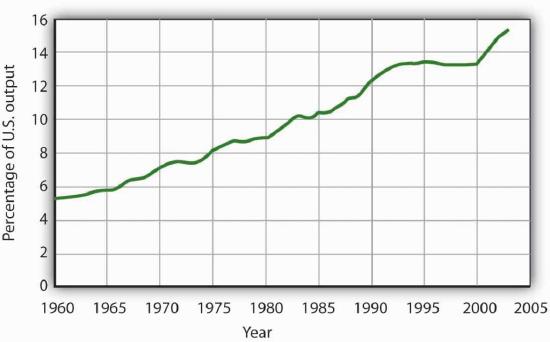

- U.S. economic growth shifted from being driven by factor quantities to being driven by factor quality and technology.

- Between 1948 and 2002, total economic output increased sixfold, with technology and capital quality playing increasingly dominant roles.

- In the 1995-2002 period, improvements in technology and capital quality accounted for a 'whopping' 70% of growth.

- The surge in growth during the late 1990s is largely attributed to the rapid integration of information technology in the workplace.

- The contribution of capital quantity significantly dropped in the most recent period, falling to just 8% compared to historical highs of 44%.

In the most recent period, 1995–2002, however, these percentages are essentially reversed, with a little less than 30% explained by increases in quantities of the factors of production and a whopping 70% explained by improvements in factor quality and technology.

Sacrifice for Future Growth

- Economic growth requires the postponement of current consumption to invest in future productive capability.

- Capital formation, such as the creation of tools or infrastructure, is a primary result of delaying immediate gratification.

- Human capital is developed through personal sacrifices, such as students choosing study over immediate income-earning work.

- A society's production possibilities curve shifts outward when resources are diverted from consumer goods to capital goods.

- The incentive to achieve production efficiency is often driven by the pursuit of profit within specific economic systems.

When Stone Age people fashioned the first tools, they were spending time building capital rather than engaging in consumption.

The Spectrum of Economic Systems

- Global economies exist on a spectrum ranging from market capitalism to command socialism.

- Market capitalism is characterized by private ownership and individual decision-making regarding resource use.

- Command socialism involves government ownership of capital and natural resources with centralized allocation power.

- Mixed economies incorporate varying elements of both capitalist and socialist systems.

- No real-world economy functions as a pure case of either extreme; they are evaluated by the degree of government intervention.

- Countries like the United States and Chile represent the capitalist end, while North Korea and Cuba represent the socialist end.

No economy represents a pure case of either market capitalism or command socialism.

The Spectrum of Economic Systems

- Economies exist on a spectrum ranging from command socialist to market capitalist, with many nations like France and Germany operating in the regulated center.

- The global shift toward market capitalism in the late 20th century was driven by its emphasis on individual freedom and decision-making power.

- Market-based systems tend to allocate resources more efficiently by leveraging comparative advantage, leading to higher production levels.

- Entrepreneurial activity is most robust in market capitalist systems where individuals can profit directly from the efficient use of resources.

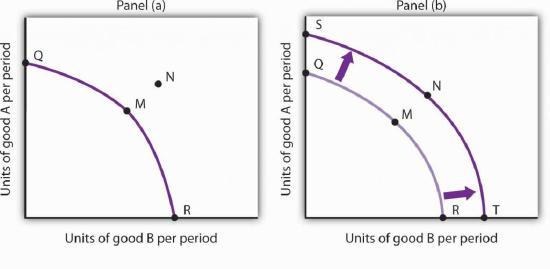

- Data from the Heritage Foundation suggests a strong positive correlation between a nation's degree of economic freedom and its per capita income.

- Heavy government regulation or state ownership can stifle productivity by prohibiting the flexible transfer of resources between different uses.

If she were operating under a command socialist system, she would not be the owner of the plants and thus would be unlikely to profit from their efficient use.

Economic Freedom and Government Roles

- Market capitalist economies are defined and measured by the degree of economic freedom they permit.

- Data from the Heritage Foundation suggests a strong correlation between high economic freedom and higher per capita income.

- While correlation exists, economists must avoid the fallacy of false cause when linking freedom to income growth.

- Governments in market economies influence production through taxes, subsidies, and the prohibition of certain goods.

- Public agencies act as the primary providers for essential services like national defense and law enforcement where private markets may not exist.

North Korea received the dubious distinction of being the least free.

Economic Growth and European Integration

- Comparative advantage and specialization are identified as primary drivers for increasing the production of goods and services through international trade.

- Economic growth requires increasing the quantity or quality of factors of production, often necessitating a postponement of current consumption to build capital.

- Market capitalist systems are noted for generally outperforming mixed or command socialist economies in terms of overall productivity.

- The European Union serves as a major real-world application of comparative advantage by eliminating trade barriers and establishing a common currency.

- The origins of European integration were radical and revolutionary, beginning with a 1950 proposal for steel cooperation between former enemies France and Germany.

The proposal for cooperation between two countries that had been the most bitter of enemies was a revolutionary one.

European Union Comparative Advantage

- The European Union functions similarly to the United States by dismantling internal trade restrictions and ceding national sovereignty to a central entity.

- Removing trade barriers allowed member nations to move from inside their collective production possibilities curve to a more efficient frontier.

- Research indicates that expanded trade within the EU is primarily driven by specialization based on comparative advantage within specific industries.

- Northern European nations like Germany and France specialize in high-value goods such as technology and luxury automobiles.

- Southern European nations like Spain and Portugal specialize in lower-value goods, including textiles, food, and budget-friendly vehicles.

- Specialization across the Union corresponds to national income levels and human capital, ultimately increasing the welfare of all member citizens.

Just as the U.S. Constitution prohibits states from restricting trade with other states, the European Union has dismantled all forms of restrictions that countries within the Union used to impose on one another.

The Production Possibilities Model

- Economics centers on the allocation of labor, capital, and natural resources through specific production choices.

- The production possibilities curve is downward sloping and bowed out, illustrating scarcity and the law of increasing opportunity cost.

- Comparative advantage drives efficient production choices and forms the theoretical basis for the benefits of international trade.

- Economic growth is achieved by increasing the quantity or quality of factors of production or through technological advancement.

- Economic systems are defined by the ownership of resources, with a global trend moving toward market capitalist models for higher productivity.

- While market systems are favored, government remains essential for establishing legal frameworks and providing social safety nets.

Producing each additional unit of the good on the horizontal axis requires a greater sacrifice of the good on the vertical axis than did the previous units produced.

Production Possibilities and Trade

- The text explores how technological improvements in one sector shift the production possibilities curve and alter opportunity costs.

- It examines the impact of resource restrictions, such as labor bans or trade barriers, on a nation's total economic output.

- The concept of comparative advantage is tested through scenarios involving specialized resources in different countries.

- The relationship between investment and consumption is questioned to determine if prioritizing growth is always a desirable social choice.

- Numerical problems are used to calculate opportunity costs and slopes to identify comparative advantages between individuals and nations.

Suppose blue-eyed people were banned from working. How would this affect a nation’s production possibilities curve?

Principles of Demand and Supply

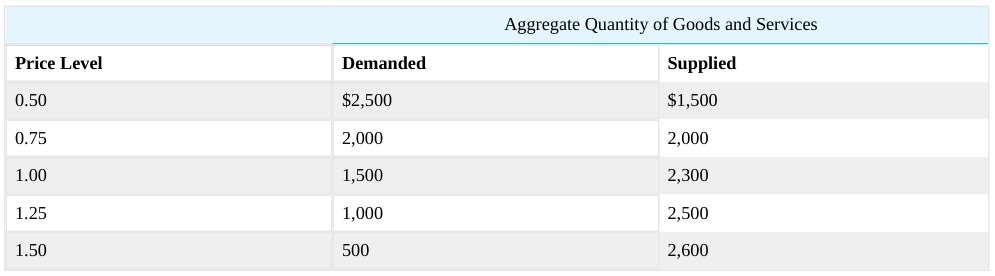

- The text transitions from comparative advantage exercises involving Turkey and Germany to the fundamental principles of demand and supply.

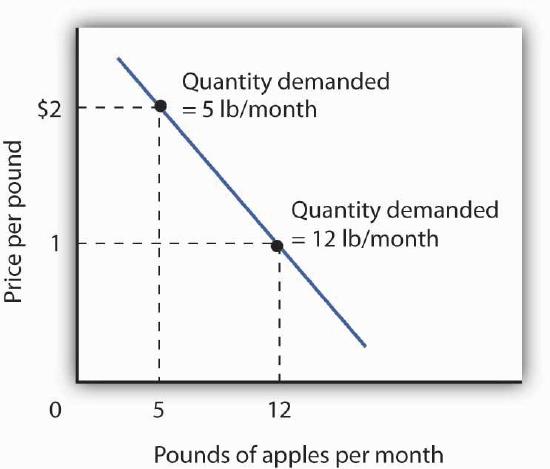

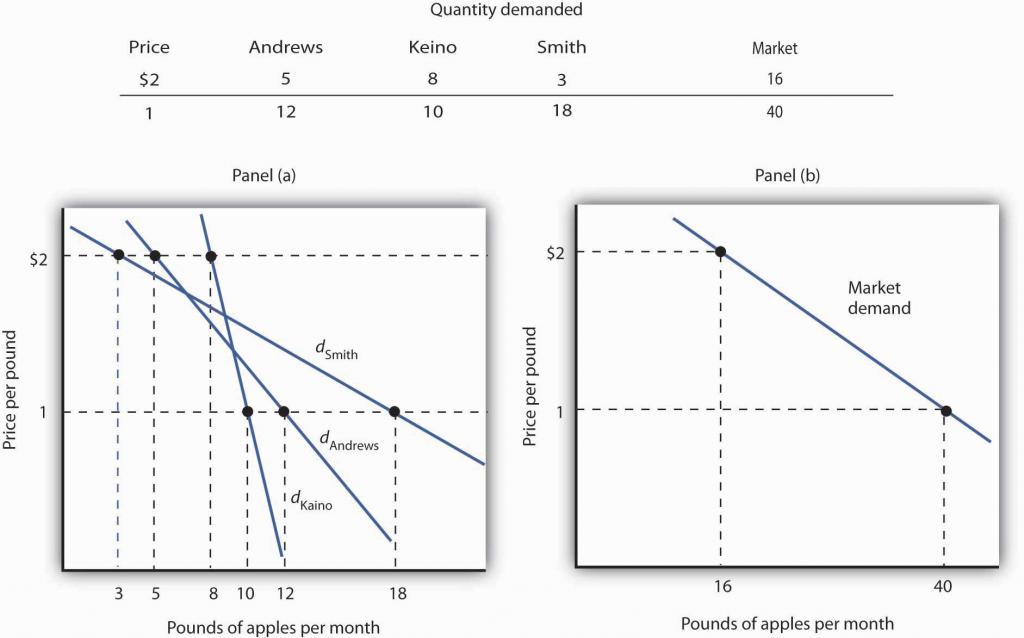

- Quantity demanded is defined as the specific amount of a good or service consumers are willing and able to purchase at various price points.

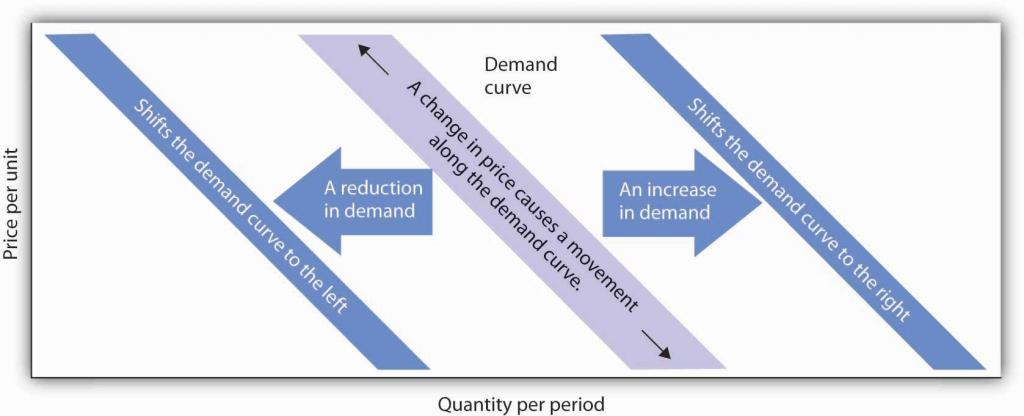

- Economists distinguish between a movement along a demand curve, caused by price changes, and a shift in the curve, caused by external variables.

- Key determinants of demand beyond price include consumer preferences, income levels, demographic characteristics, and the prices of related goods.

- The law of demand is illustrated by the inverse relationship between price and quantity, where higher prices typically reduce consumer desire for a product.

How many pizzas will people eat this year? How many doctor visits will people make? How many houses will people buy?

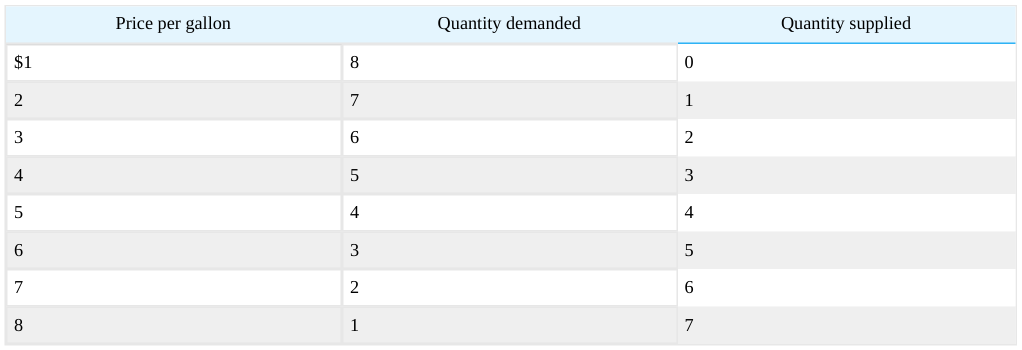

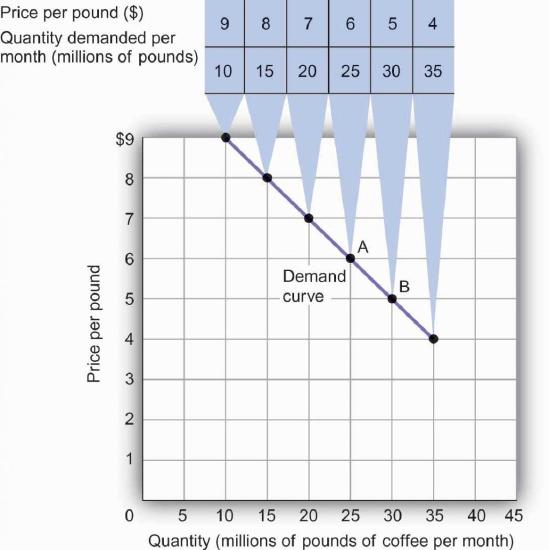

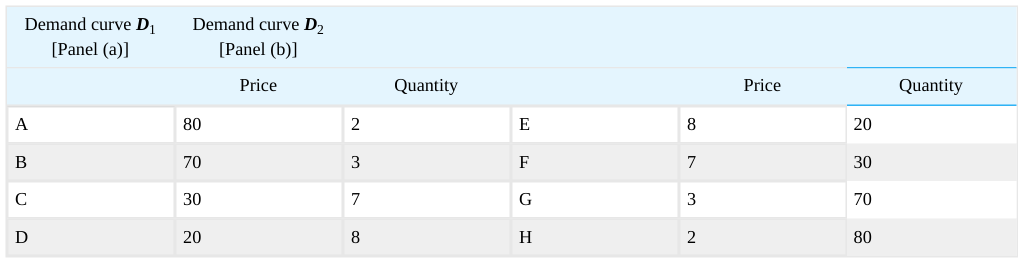

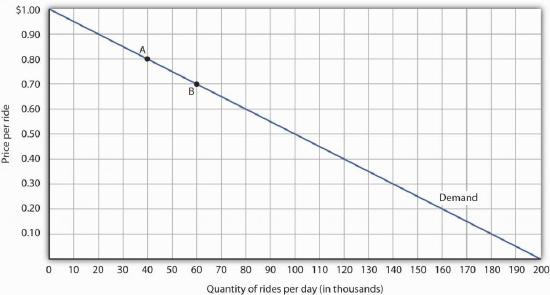

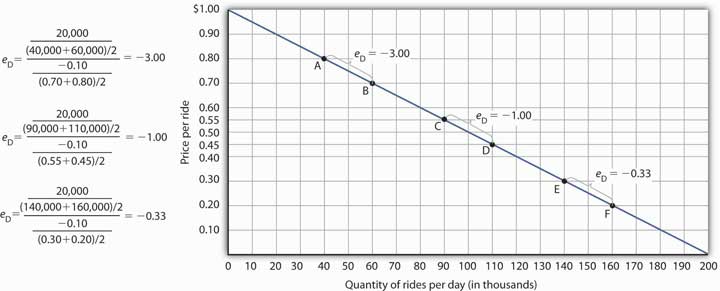

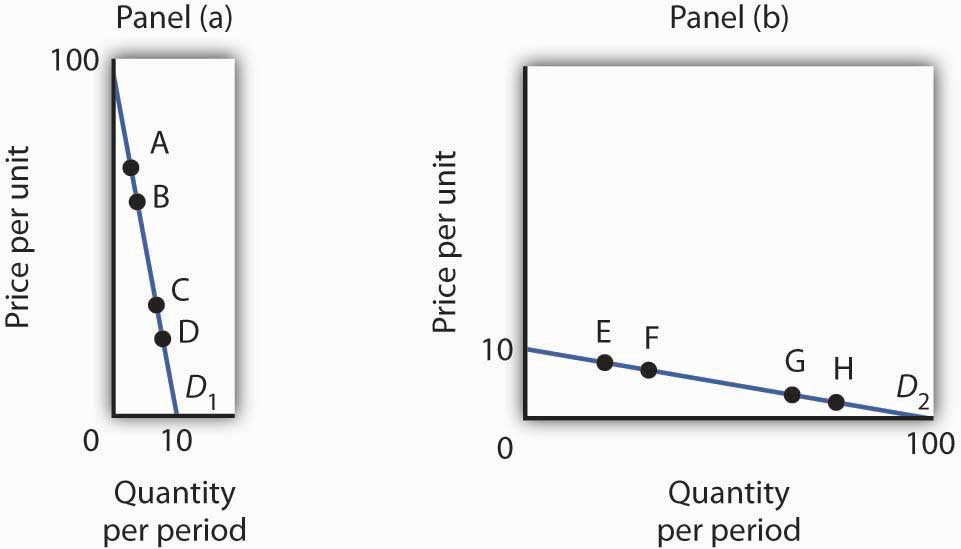

Defining Demand and Quantity

- Economists distinguish between 'demand' as a general concept and 'quantity demanded,' which refers to a specific amount at a specific price.

- The 'ceteris paribus' assumption is essential to isolating the relationship between price and quantity by holding all other variables constant.

- A demand schedule provides a tabular view of how different price points correlate with the quantities buyers are willing to purchase.

- A demand curve serves as a graphical representation of the schedule, typically plotting price on the vertical axis and quantity on the horizontal axis.

- Movement along the demand curve is strictly defined as a 'change in quantity demanded' resulting from a change in price alone.

The quantity demanded of a good or service is the quantity buyers are willing and able to buy at a particular price during a particular period, all other things unchanged.

The Law of Demand

- The law of demand establishes a fundamental behavioral relationship where price and quantity demanded move in opposite directions.

- A movement along the demand curve occurs when the price of a good changes while all other factors remain constant.

- Empirical evidence from numerous economic studies consistently supports the validity of the law of demand.

- Retailers practically apply this law by lowering prices during sales to clear overstock and increase consumer purchases.

- The negative slope of the demand curve is a visual representation of the inverse relationship between price and quantity.

When a store finds itself with an overstock of some item, such as running shoes or tomatoes, and needs to sell these items quickly, what does it do?

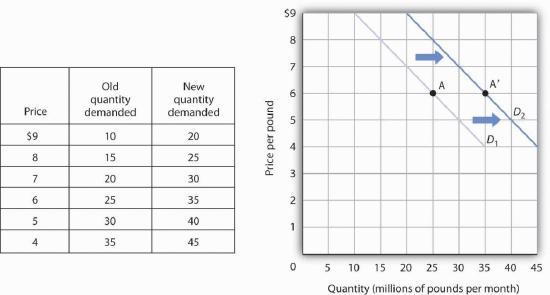

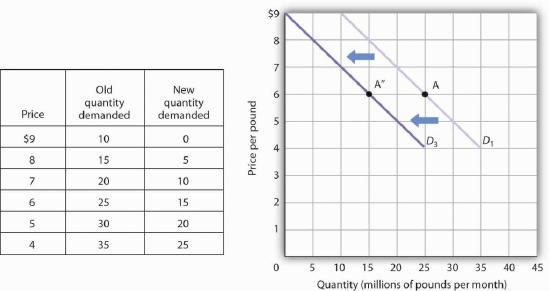

Shifts in the Demand Curve

- While price influences consumption, other variables like income, population, and preferences also dictate the quantity of goods demanded.

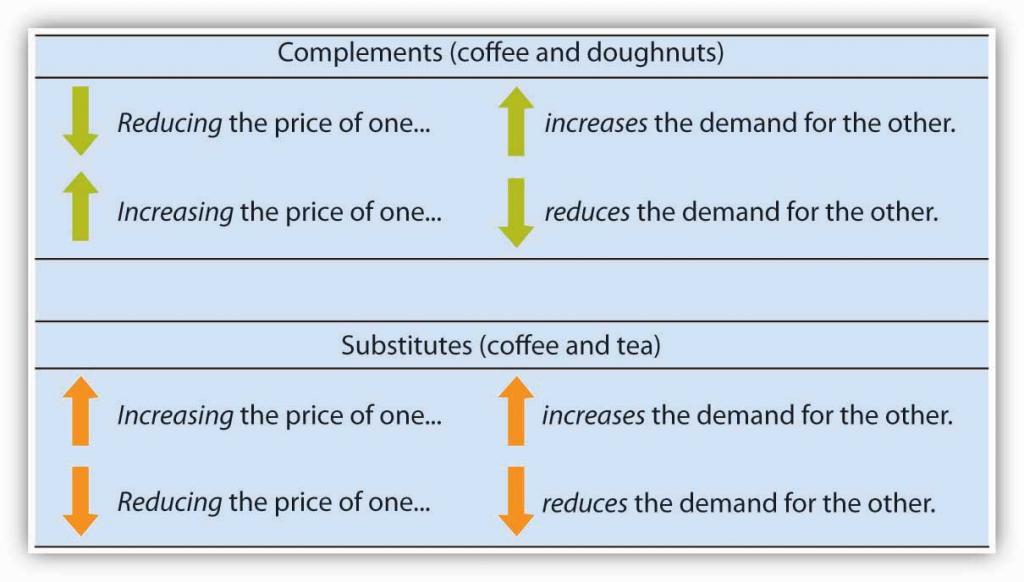

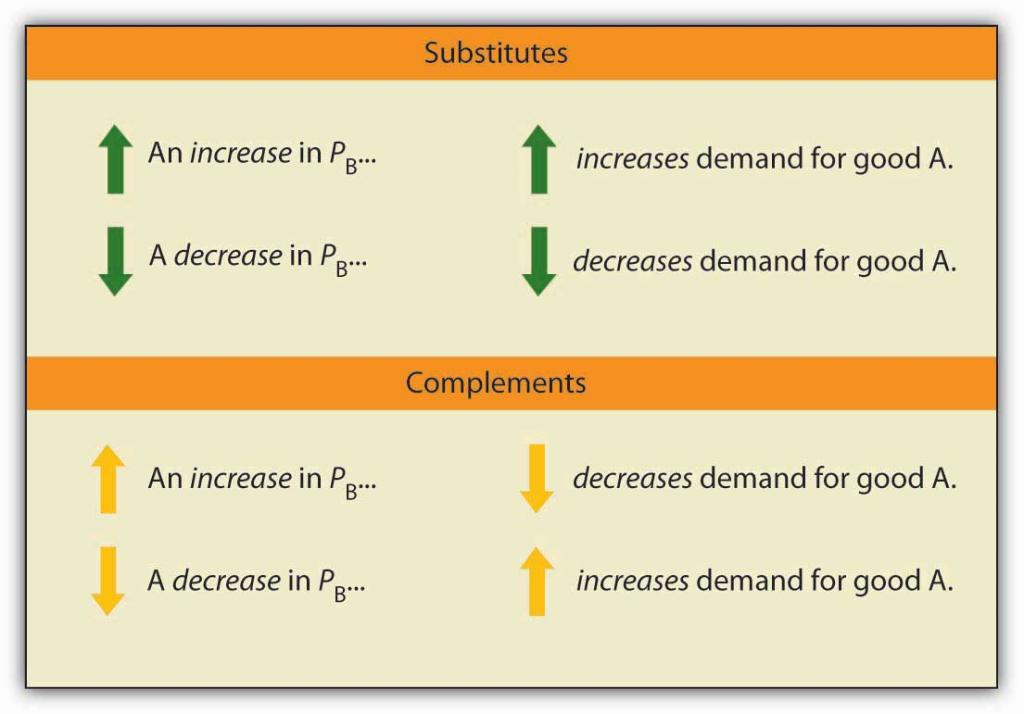

- The prices of related goods, such as complements like doughnuts or substitutes like tea, significantly impact the demand for a specific product.

- A change in any variable held constant during the creation of a demand schedule results in a shift of the entire demand curve rather than a movement along it.

- An increase in demand is represented graphically as a rightward shift, meaning more of a product is purchased at every given price point.

- A decrease in demand, or a leftward shift, can be triggered by external factors such as negative health findings or a reduction in the consumer population.

- Economists distinguish between a 'change in quantity demanded' (movement along the curve) and a 'change in demand' (a shift of the curve itself).

A shift in a demand curve is called a change in demand.

Determinants of Market Demand

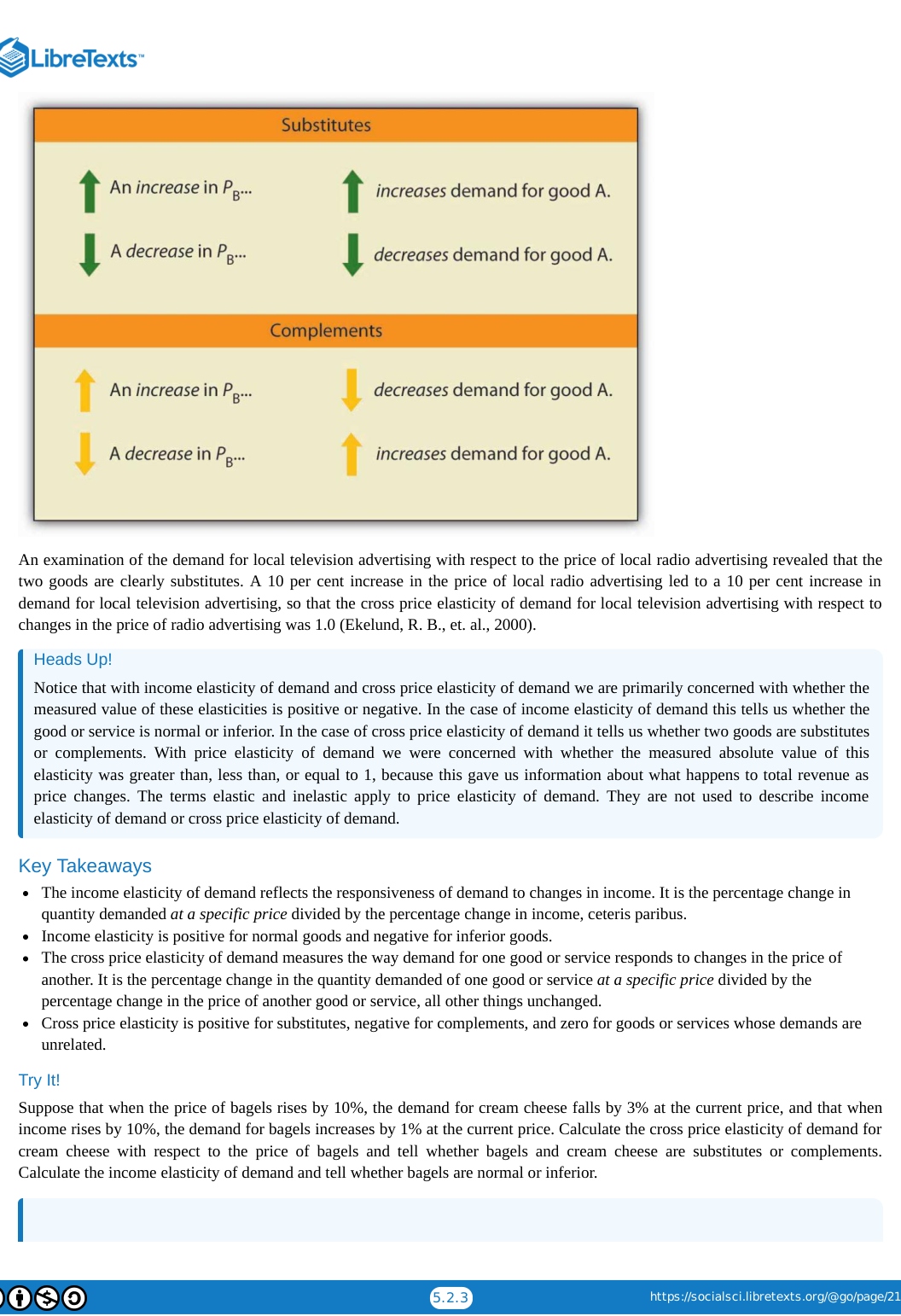

- Demand shifters include consumer preferences, prices of related goods, income levels, demographics, and buyer expectations.

- Changes in consumer preferences, such as health concerns regarding cigarettes, can shift the demand curve significantly to the left or right.

- Related goods are classified as complements, which are used together, or substitutes, which are used in place of one another.

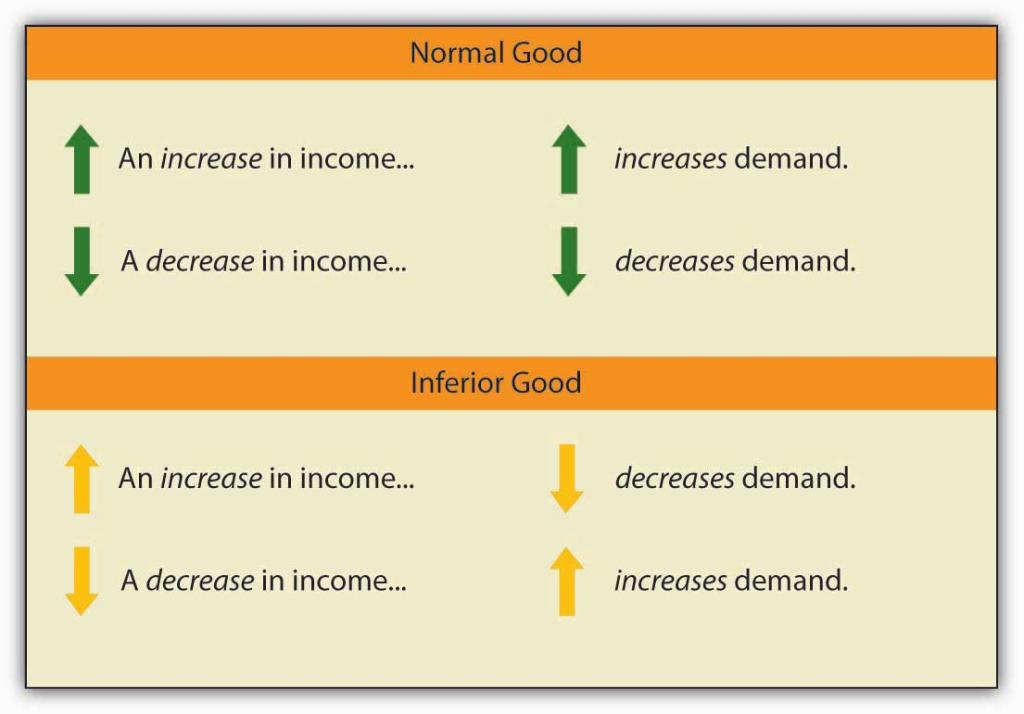

- Income levels distinguish normal goods, where demand rises with wealth, from inferior goods, where demand falls as income increases.

- Demographic shifts, such as an aging population or changes in birth rates, create long-term fluctuations in demand for specific services like healthcare or education.

A good for which demand increases when income increases is called a normal good. A good for which demand decreases when income increases is called an inferior good.

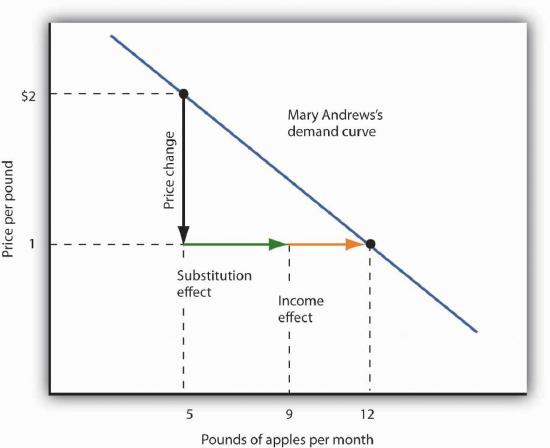

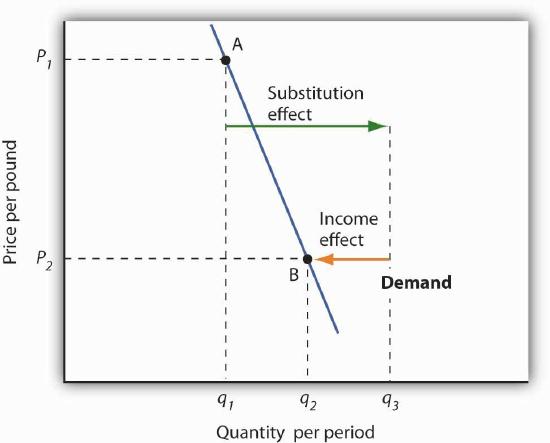

Dynamics of Buyer Demand

- Buyer expectations regarding future prices and technology significantly influence current consumption patterns for storable goods.

- Economists distinguish between a change in 'quantity demanded' (movement along a curve) and a 'change in demand' (a shift of the curve itself).

- The law of demand dictates that higher prices generally reduce the quantity demanded, provided all other factors remain unchanged.

- Demand shifters such as preferences, income, demographics, and the prices of related goods cause the entire demand curve to move.

- Goods are categorized as substitutes or complements based on how price changes in one affect the demand for the other.

- Income levels define whether a product is a 'normal good' (demand rises with income) or an 'inferior good' (demand falls with income).

If people expect gasoline prices to rise tomorrow, they will fill up their tanks today to try to beat the price increase.

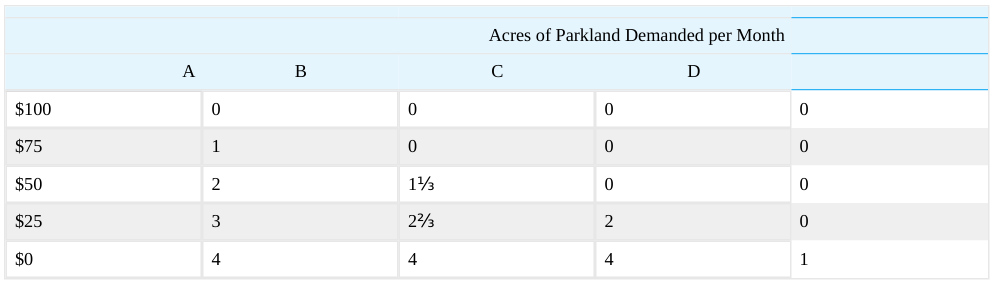

Solving Campus Parking Problems

- University parking demand has surged, with 70% of students owning cars and many driving even for short five-minute commutes.

- Most universities heavily subsidize parking, losing between $400,000 and $1.2 million annually per 1,000 spaces, with costs hidden in general tuition.

- Administrators often avoid raising parking fees to market rates due to fear of political backlash from students, parents, and faculty.

- Shifting demand through substitutes, such as free carpooling and public transit, has proven more effective than expanding infrastructure.

- The University of Washington and University of Colorado saved millions by investing in commuter alternatives rather than expensive parking structures.

Indeed, according to Clark Kerr, a former president of the University of California system, a university is best understood as a group of people “held together by a common grievance over parking.”

Dynamics of Demand and Supply

- The demand for substitute goods, such as DVD rentals, increases when the price of the primary alternative, like movie tickets, rises.

- Changes in family income shift demand curves differently depending on whether a product is classified as a normal or inferior good.

- A change in a product's own price results in a movement along the demand curve rather than a shift of the curve itself.

- Quantity supplied is primarily driven by price, where higher prices typically incentivize sellers to offer more goods, assuming all other factors remain constant.

- Supply is influenced by production costs, including factor prices, technology, seller expectations, and the total number of market participants.

- External variables like natural events and weather changes can significantly impact the cost of production and the resulting supply curve.

The latter may be the case for some families, since staying at home and watching DVDs is a cheaper form of entertainment than taking the family to the movies.

The Law of Supply

- The quantity supplied is defined as the amount sellers are willing to provide at a specific price, assuming all other factors remain constant.

- The law of supply generally dictates that higher prices lead to an increase in the quantity supplied because of higher profit incentives.

- Supply schedules and supply curves provide tabular and graphical representations of the positive relationship between price and quantity.

- Exceptions to the law of supply exist, such as fixed-supply goods like specific real estate or rare cases where higher prices reduce supply.

- A change in price results in a movement along the supply curve, which is technically termed a change in quantity supplied rather than a shift in the curve.

Goods that cannot be produced, such as additional land on the corner of Park Avenue and 56th Street in Manhattan, are fixed in supply—a higher price cannot induce an increase in the quantity supplied.

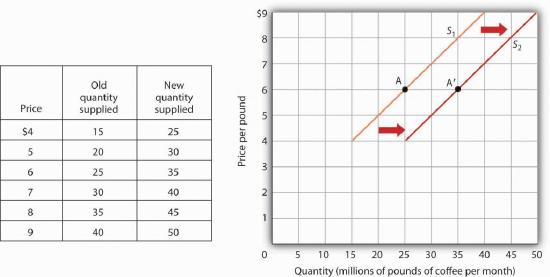

Mechanics of Supply Shifters

- Supply curves are drawn under the assumption that all variables other than price remain constant.

- A change in external variables results in a shift of the entire supply curve rather than a movement along it.

- Factors that increase supply, such as lower production costs, shift the curve to the right, increasing quantity at every price point.

- Factors that decrease supply, such as natural disasters or rising labor costs, shift the curve to the left.

- Key supply shifters include production factor prices, technology, seller expectations, and the number of market participants.

- The cost of factors of production, like labor and fertilizer, directly dictates the quantity suppliers are willing to offer at a given price.

When these other variables change, the all-other-things-unchanged conditions behind the original supply curve no longer hold.

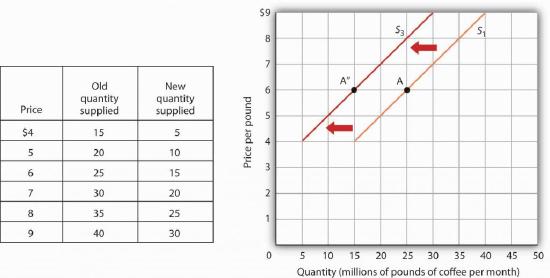

Factors Influencing Market Supply

- Opportunity cost dictates that producing one good requires forgoing another, meaning a price rise in a related good can decrease the supply of the current one.

- Technological advancements lower production costs and increase profit margins, shifting the supply curve to the right.

- Government regulations, such as mandatory pollution-control devices, can act as a technological reversal by increasing costs and reducing supply.

- Seller expectations regarding future price increases can lead producers to withhold current inventory, effectively shifting supply to the left.

- Natural events and disasters, such as the 2008 Myanmar cyclone, create unpredictable shifts in agricultural supply by destroying production capacity.

If a change in the international political climate leads many owners to expect that oil prices will rise in the future, they may decide to leave their oil in the ground, planning to sell it later when the price is higher.

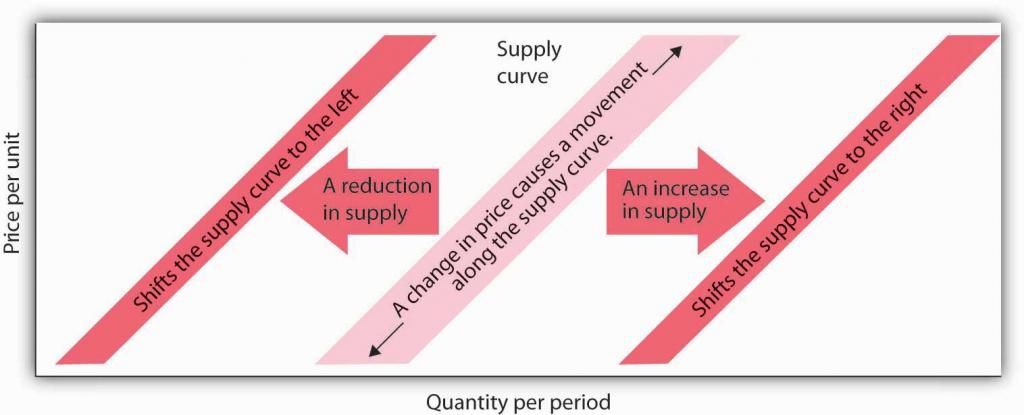

Dynamics of Supply Curves

- The number of sellers in an industry directly impacts the supply curve, with more sellers shifting it to the right and fewer shifting it to the left.

- It is critical to distinguish between a change in supply, which shifts the entire curve, and a change in quantity supplied, which is a movement along the curve caused by price changes.

- Supply shifters include production factor prices, technology, seller expectations, natural events, and the number of market participants.

- A common student error is misinterpreting a rightward shift as a 'downward' move due to the upward slope of the supply curve.

- An increase in supply always moves toward a higher quantity on the horizontal axis, regardless of the vertical appearance of the curve.

Students sometimes make the mistake of thinking of such a shift as a shift “down” and therefore as a reduction in supply.

Monastic Opportunity Costs

- The monks of St. Benedict’s monastery transitioned through three distinct business models: egg production, cookie manufacturing, and private retreats.

- Rising grain prices in the 1970s and 1980s doubled production costs for eggs, forcing the monks to adopt more aggressive agricultural practices.

- The shift from eggs to cookies was driven by a comparative analysis of profitability and the desire for a better quality of life, specifically the ability to take Sundays off.

- Market demand influenced their decisions, as declining egg consumption due to health concerns coincided with the success of their mail-order cookie experiment.

- Ultimately, the monks moved into the retreat business because it offered the highest return on investment and required the least amount of daily labor.

- This case study illustrates the economic principle of opportunity cost, where the monks consistently chose the path that maximized both financial and spiritual resources.

“The chickens didn’t stop laying eggs on Sunday,” Father Joseph chuckles. “When we shifted to cookies we could take Sundays off. We weren’t hemmed in the way we were with the chickens.”

Supply Dynamics and Market Equilibrium

- An increase in the wages of production factors, such as rental clerks, raises production costs and shifts the supply curve to the left.

- Wage increases for specific workers should be viewed as supply shifters rather than significant drivers of consumer demand.

- Changes in the price of a good do not shift the supply curve but instead cause movement along the existing curve.

- The entry of more firms into a market increases the number of suppliers, shifting the supply curve to the right.

- The model of demand and supply combines both curves to determine the equilibrium price and quantity in a given market.

- Market imbalances, such as surpluses and shortages, create natural pressures that drive prices toward equilibrium.

An increase in the price of DVD rentals does not shift the supply curve at all; rather, it corresponds to a movement upward to the right along the supply curve.

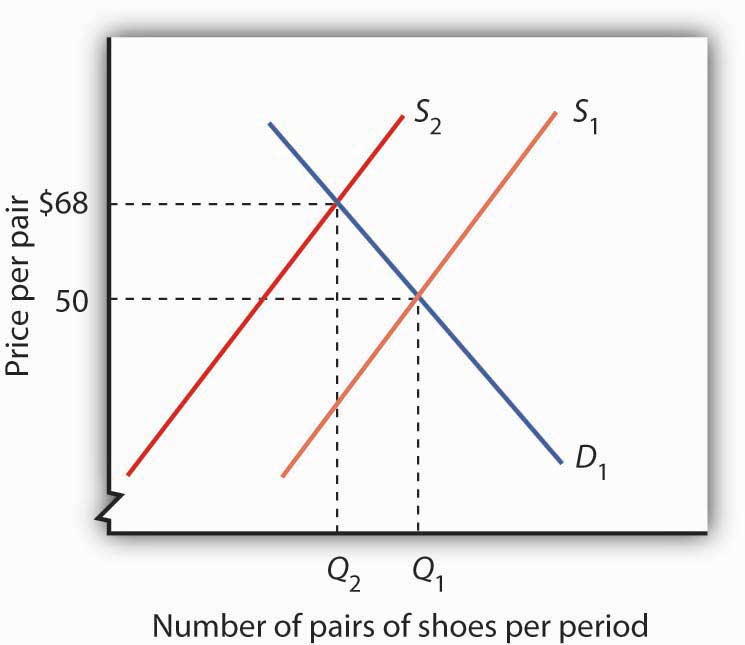

Market Equilibrium Dynamics

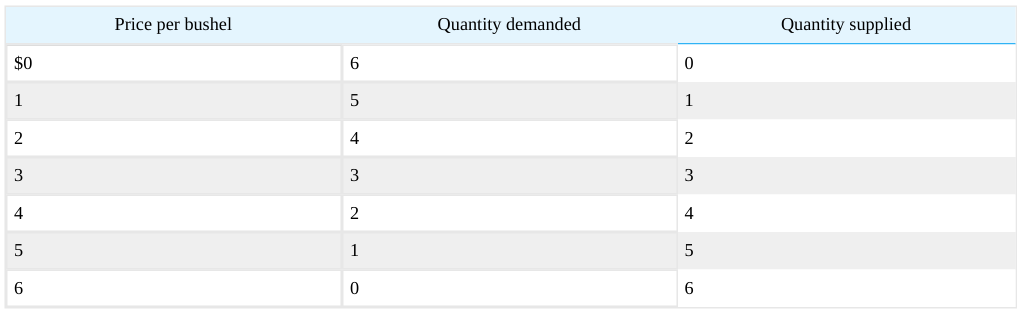

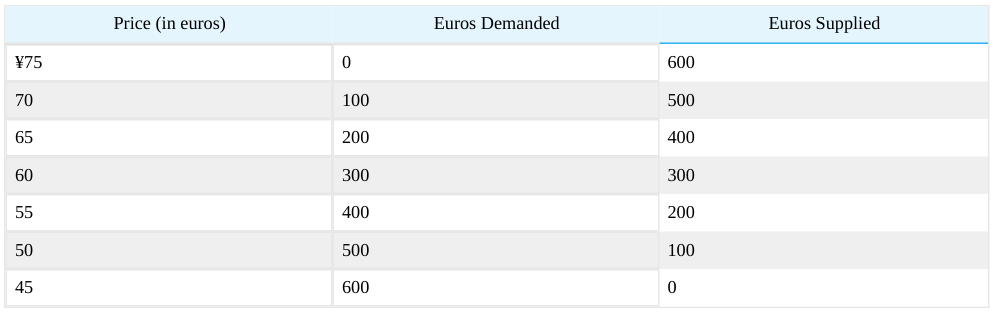

- The demand curve represents the quantity buyers are willing and able to purchase at various price points.

- The supply curve illustrates the quantities sellers are prepared to offer for sale at those same prices.

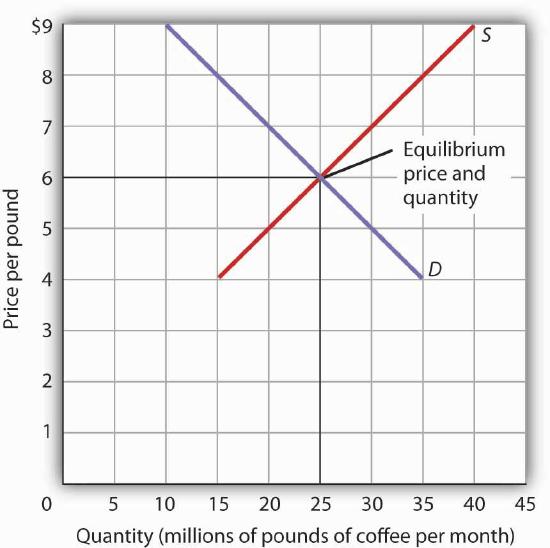

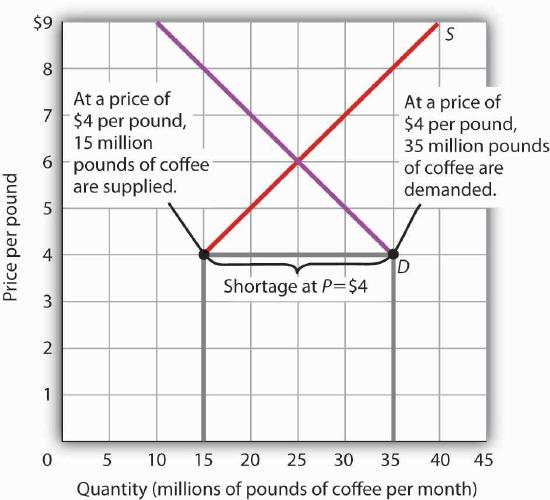

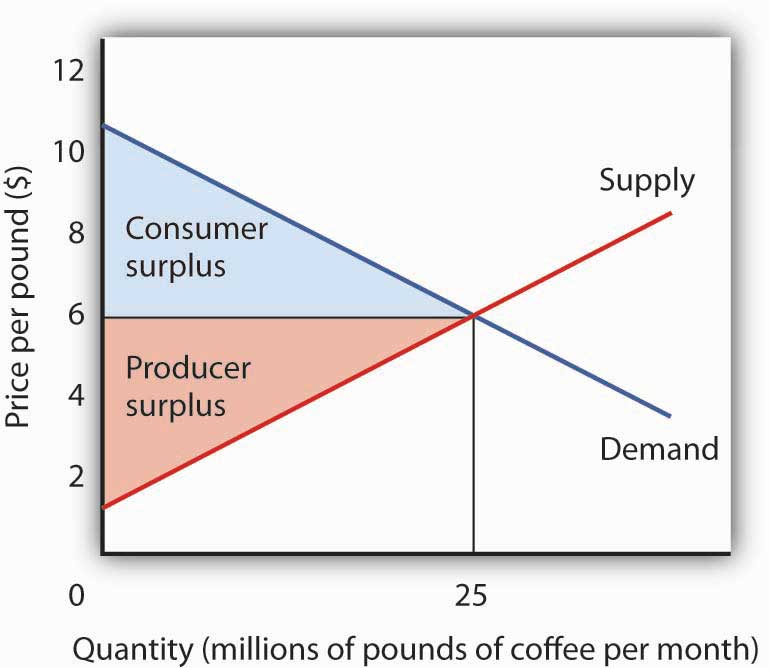

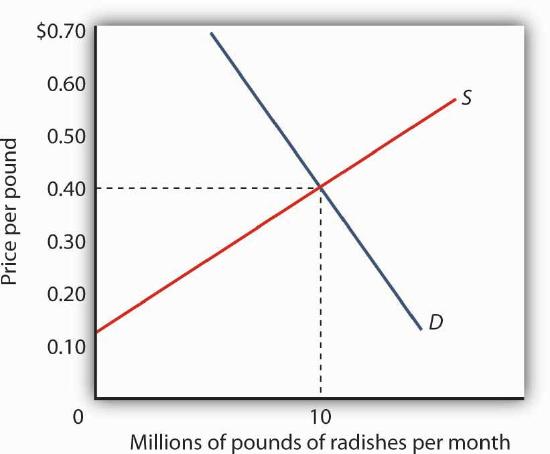

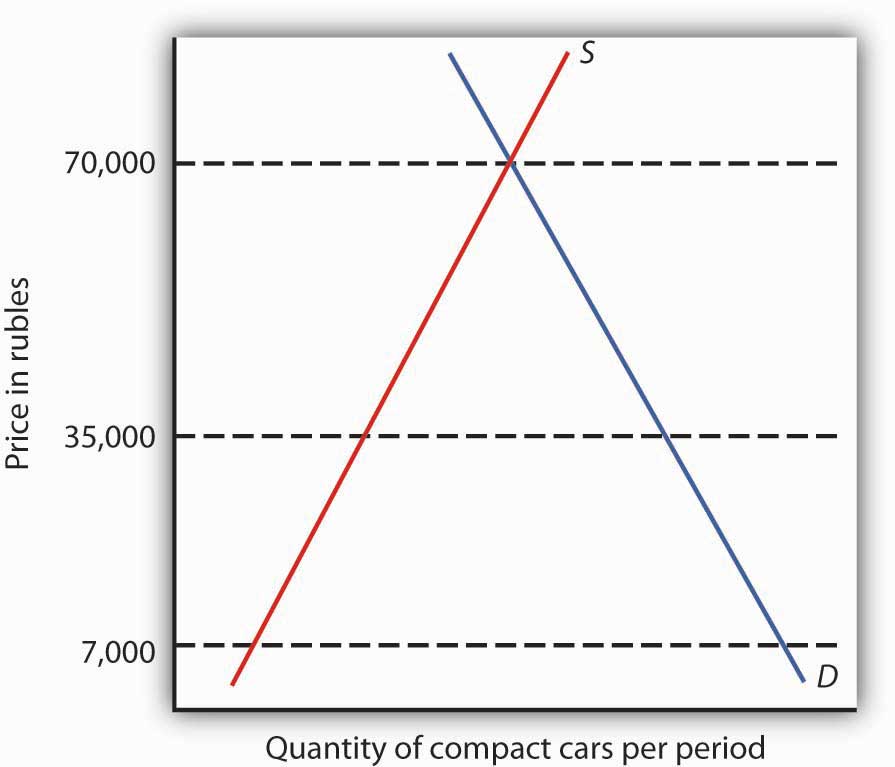

- Market equilibrium occurs at the specific intersection where the quantity demanded exactly equals the quantity supplied.

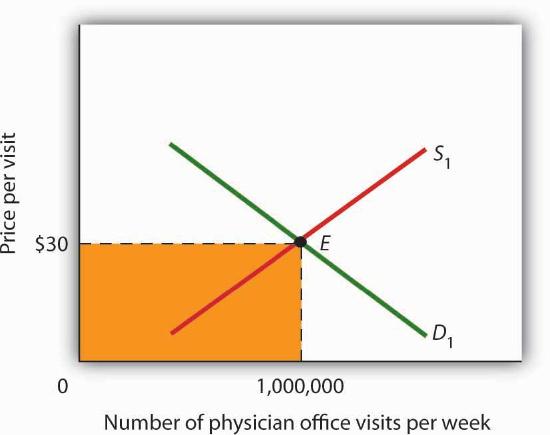

- In the provided coffee market example, equilibrium is reached at a price of $6 per pound and a quantity of 25 million pounds.

- Unless external factors cause the curves to shift, there is no inherent pressure for the equilibrium price to change.

- Any price point above or below the intersection results in a market imbalance, leading to either surpluses or shortages.

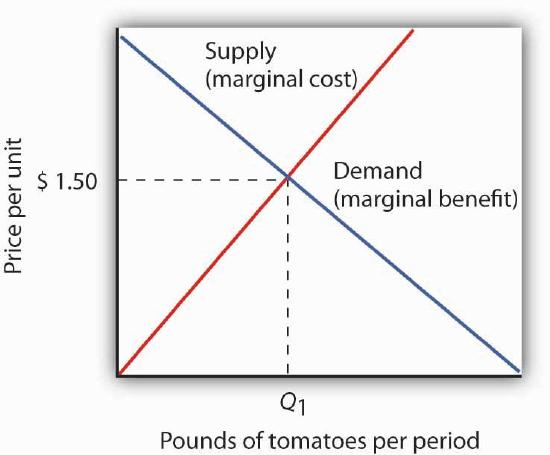

The equilibrium price in any market is the price at which quantity demanded equals quantity supplied.

Market Surpluses and Shortages

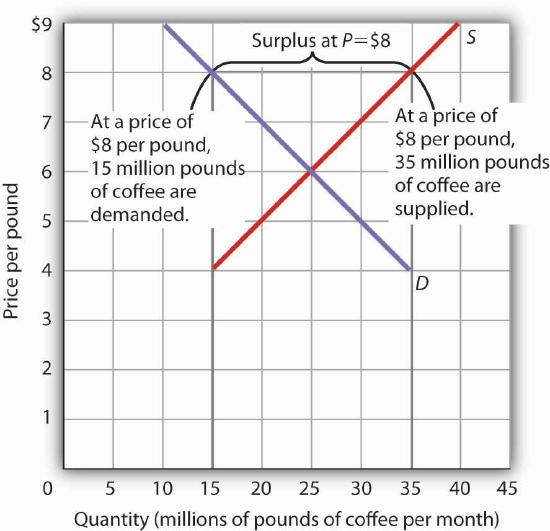

- A surplus occurs when the current market price is set above the equilibrium level, resulting in a quantity supplied that exceeds the quantity demanded.

- In response to a surplus, sellers naturally lower prices to clear unsold inventory, which simultaneously decreases supply quantity and increases demand quantity.

- A shortage arises when the market price falls below equilibrium, leading to a situation where consumers demand more than sellers are willing to provide.

- Market forces typically correct shortages as sellers raise prices, causing a movement along the curves until the equilibrium intersection is reached.

- Price adjustments serve as a self-correcting mechanism in most markets, though some specific goods may adjust to equilibrium very slowly or not at all.

With unsold coffee on the market, sellers will begin to reduce their prices to clear out unsold coffee.

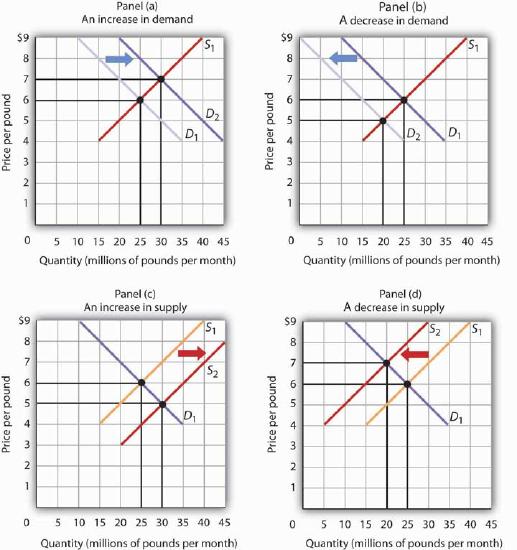

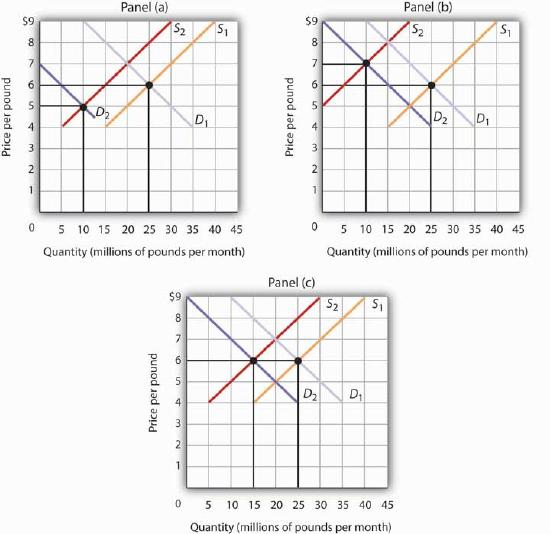

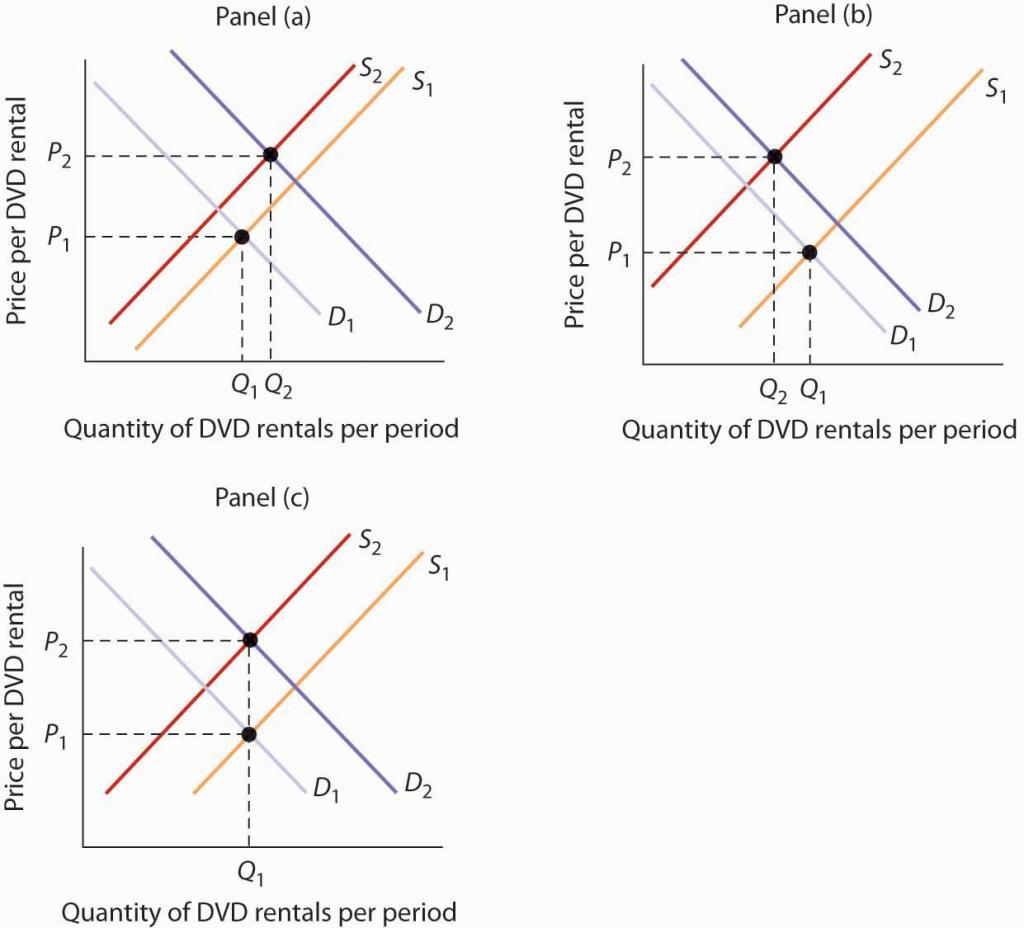

Market Equilibrium and Curve Shifts

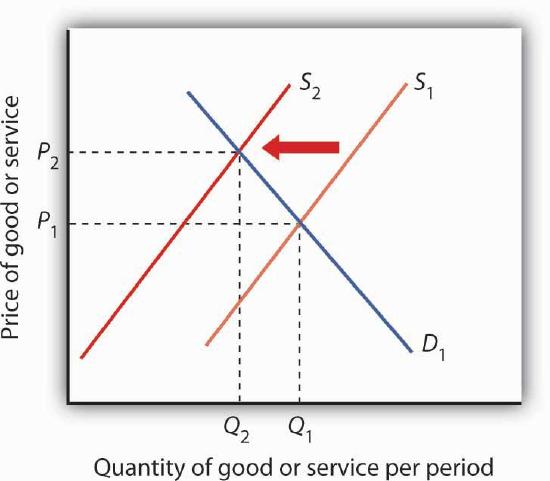

- Changes in demand or supply shifters alter the equilibrium price and quantity of a good or service.

- An increase in demand shifts the demand curve right, raising both the equilibrium price and the quantity supplied.

- A decrease in demand shifts the curve left, resulting in a lower equilibrium price and a reduction in quantity supplied.

- Supply increases shift the supply curve right, which lowers the equilibrium price while increasing the quantity demanded.

- Shifts in one curve cause movement along the other curve rather than shifting both simultaneously in the initial response.

- External factors like weather, income, and the price of complements or substitutes act as the primary drivers for these shifts.

Notice that the supply curve does not shift; rather, there is a movement along the supply curve.

Supply Shifters and Market Equilibrium

- A decrease in supply shifts the supply curve to the left, resulting in a higher equilibrium price and a lower quantity demanded.

- Factors that reduce supply include rising input costs, better returns on alternative products, technological setbacks, or natural disasters.

- When analyzing market changes, it is crucial to distinguish between a shift in the entire curve and a movement along the curve.

- A common analytical error is confusing a change in quantity demanded with a change in demand itself.

- The 'Heads Up!' section provides a step-by-step methodology for graphing supply and demand shifts using plausible numerical values.

- Logical consistency checks, such as ensuring a scarcity of goods leads to a price increase, help verify the accuracy of economic models.

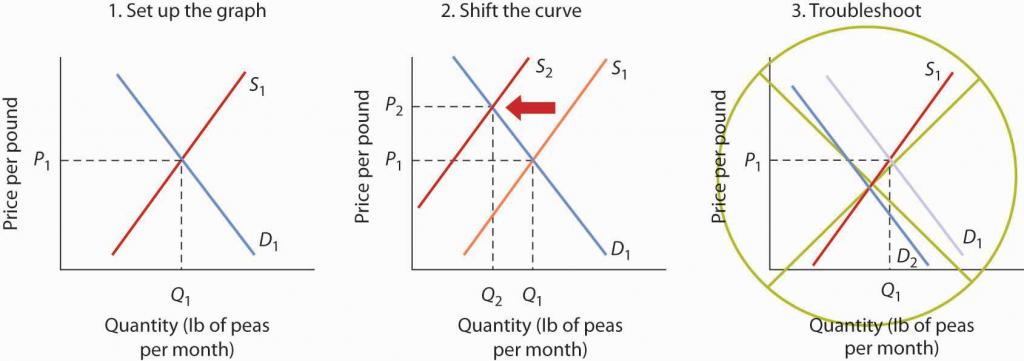

Suppose you are told that an invasion of pod-crunching insects has gobbled up half the crop of fresh peas, and you are asked to use demand and supply analysis to predict what will happen to the price and quantity of peas demanded and supplied.

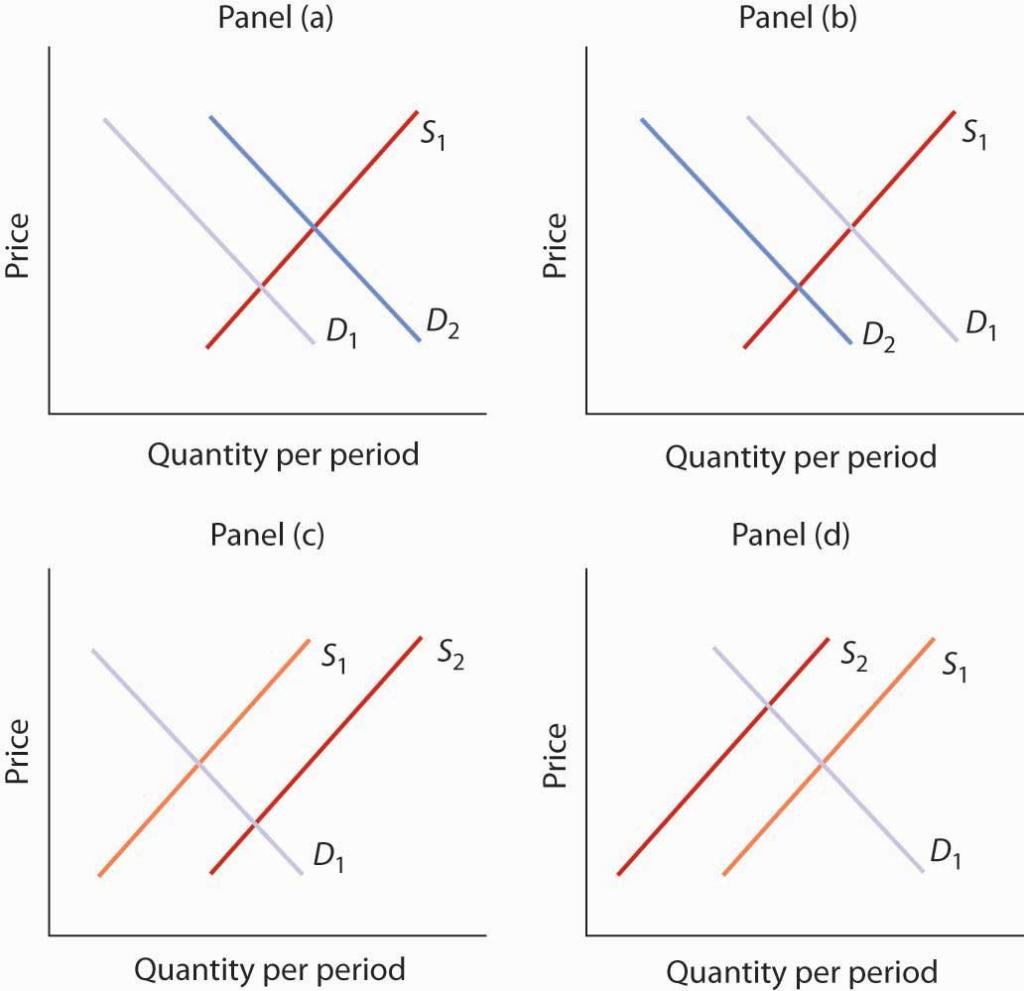

Simultaneous Shifts in Market Equilibrium

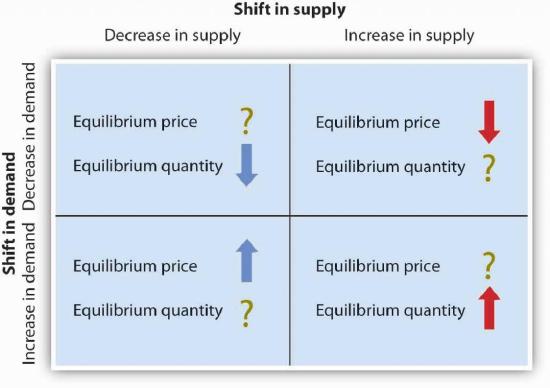

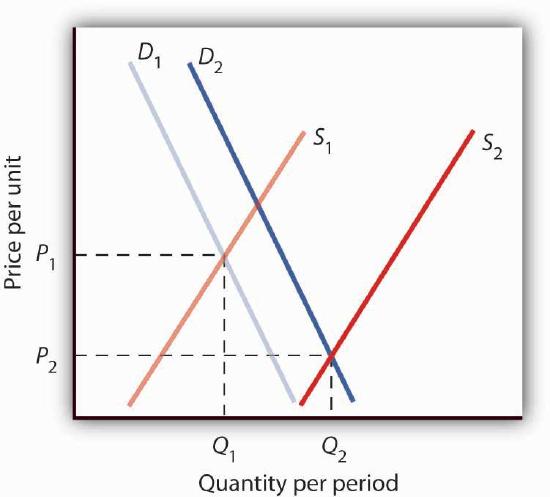

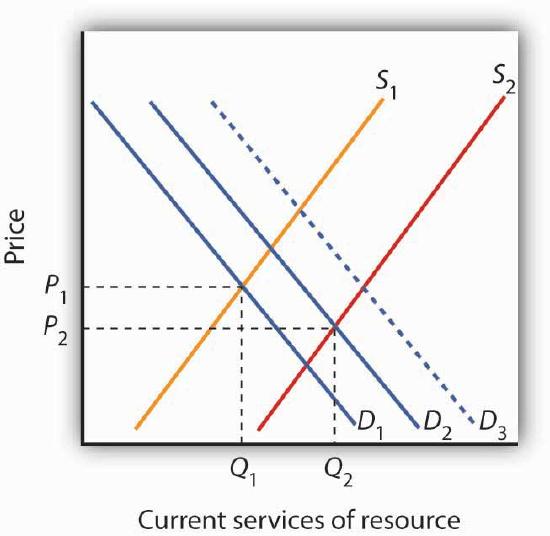

- Single shifts in demand or supply produce predictable changes in both equilibrium price and quantity.

- When both demand and supply shift simultaneously, the outcome for at least one variable becomes ambiguous.

- A simultaneous decrease in both demand and supply will always result in a lower equilibrium quantity.

- The direction of price change during simultaneous shifts depends entirely on the relative magnitude of each curve's movement.

- If demand shifts further left than supply, price falls; if supply shifts further left than demand, price rises.

- Analyzing complex market changes requires breaking down events separately to determine their individual impacts on price and quantity.

Whether the equilibrium price is higher, lower, or unchanged depends on the extent to which each curve shifts.

Market Equilibrium and Curve Dynamics

- Prices act as the primary mechanism to balance the quantity demanded with the quantity supplied.

- Without price adjustments, the essential balance between market supply and demand cannot be maintained.

- Linear representations of supply and demand curves are used as a simplification to enhance readability.

- Regardless of their shape, demand curves consistently slope downward while supply curves generally slope upward.

- Analyzing shifts in these curves allows for the prediction of changes in market price and quantity.

If prices did not adjust, this balance could not be maintained.

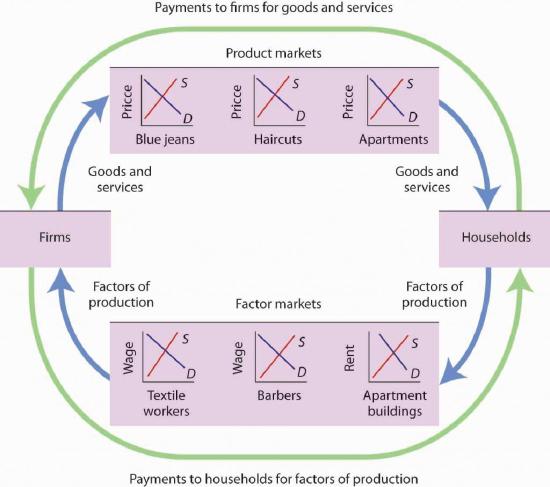

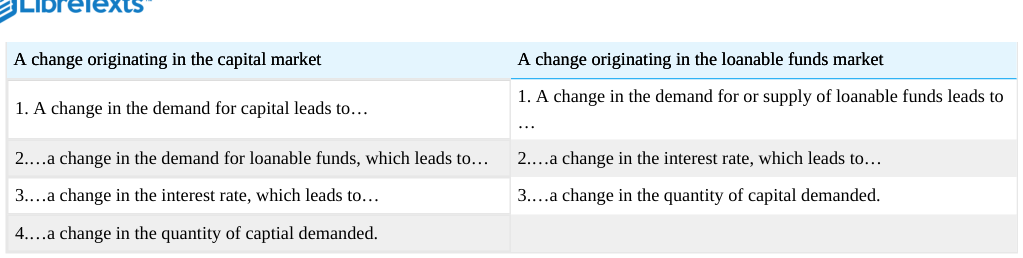

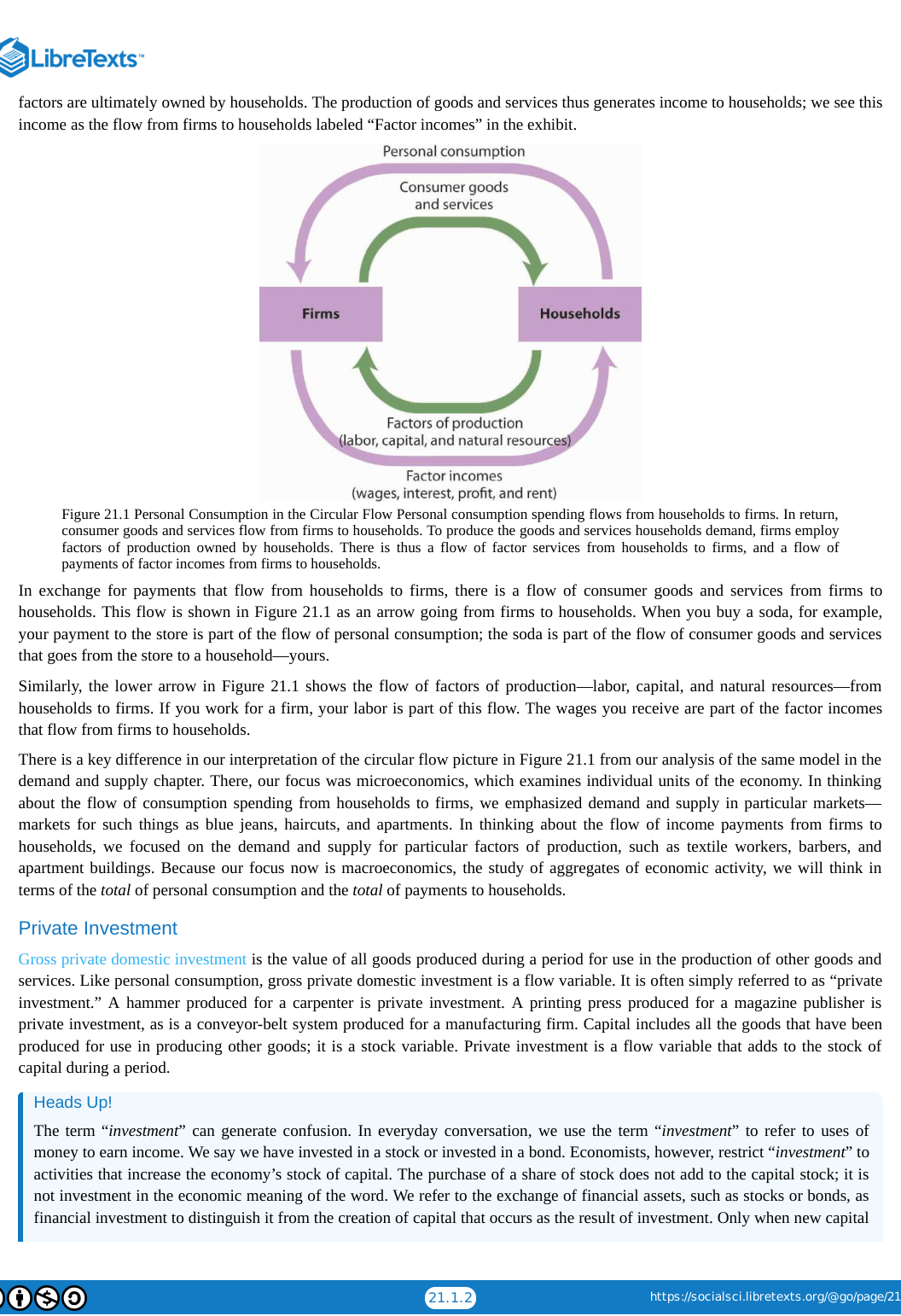

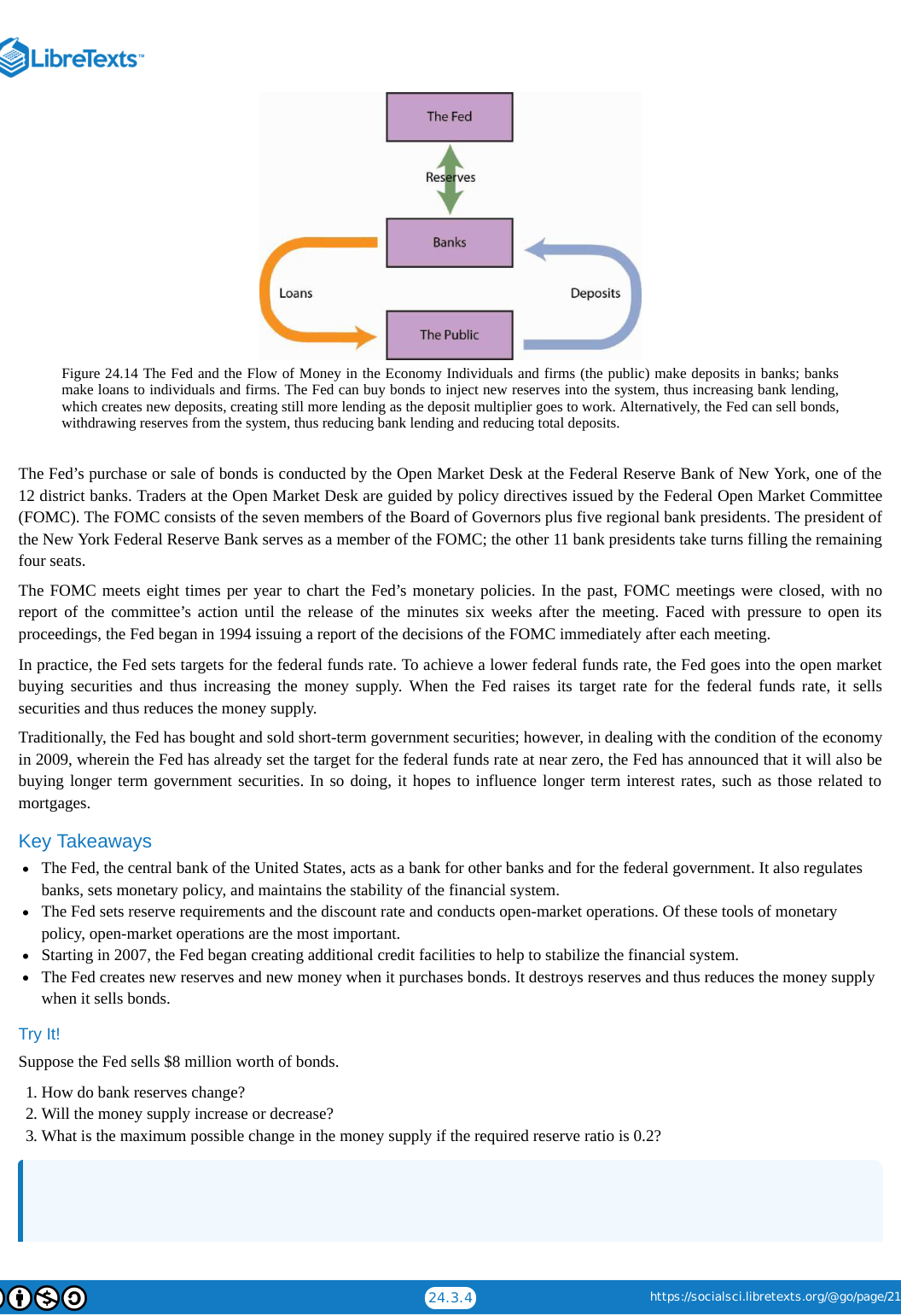

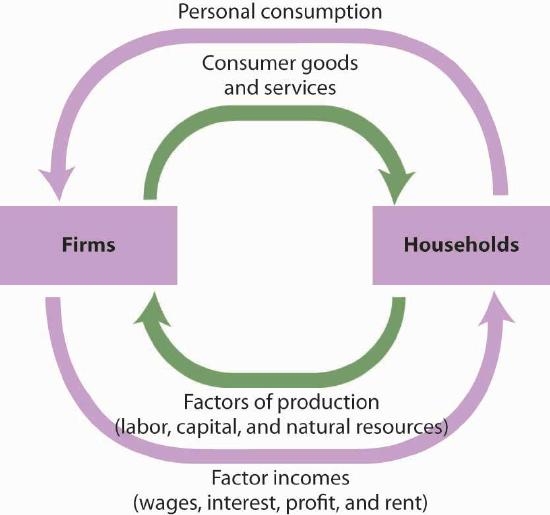

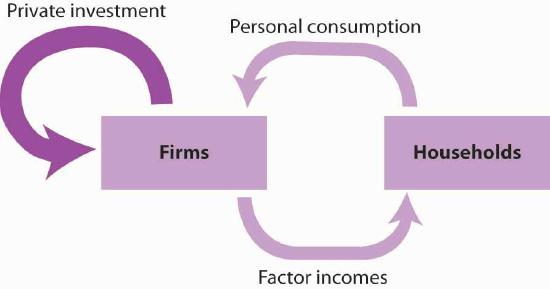

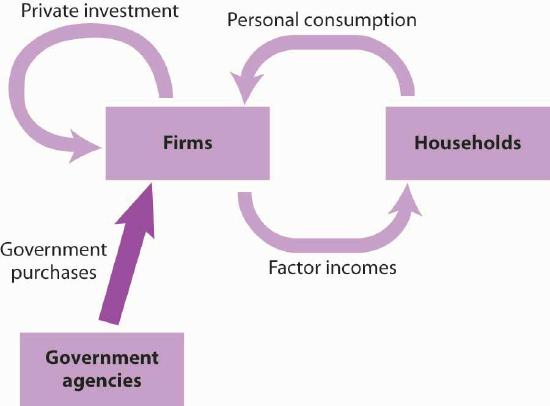

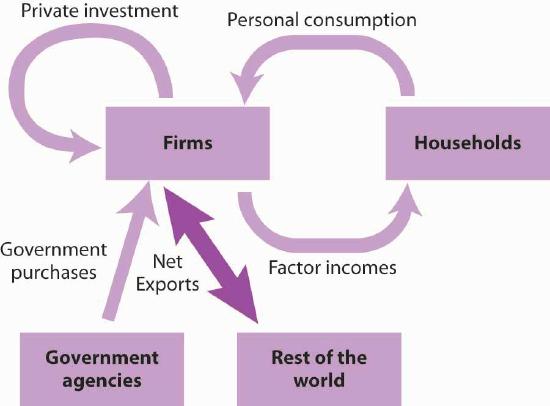

The Circular Flow Model

- The circular flow model illustrates the continuous interaction and adjustment between households and firms within an economy.

- Economic activity is defined as a process of exchange where firms provide goods and services while households provide factors of production like labor and capital.

- Product markets represent the top half of the cycle where households demand goods, while factor markets represent the bottom half where firms demand resources.

- The model demonstrates how markets are interrelated, showing that a change in demand for a consumer product directly impacts the demand for the labor required to produce it.

- While simplified by omitting government and foreign sectors, the model accurately reflects the millions of individual exchanges that constitute a private domestic economy.

The circular flow model shows that goods and services that households demand are supplied by firms in product markets.

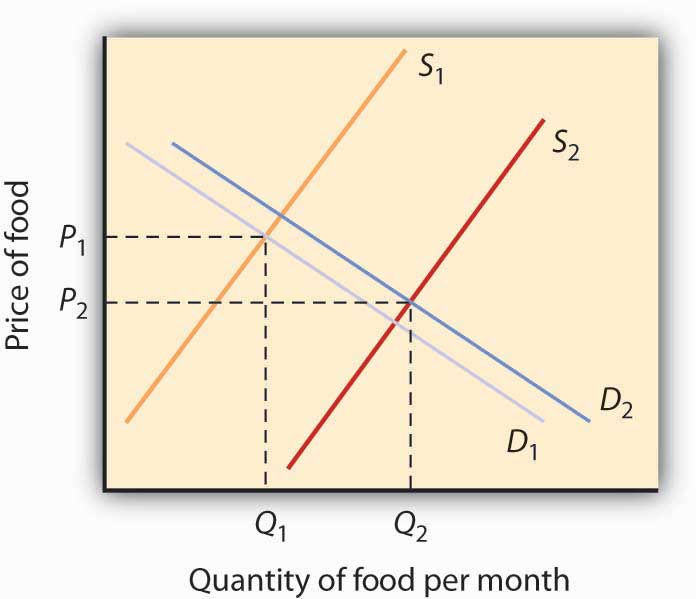

Market Equilibrium and Obesity Trends

- Equilibrium price is established at the intersection of supply and demand curves where quantity supplied equals quantity demanded.

- Market imbalances such as surpluses and shortages exert downward or upward pressure on prices to restore equilibrium.

- Shifts in demand or supply curves independently predict changes in price and quantity, but simultaneous shifts require knowing the magnitude of each change.

- The circular flow model illustrates the interconnectedness of product and factor markets within an economy.

- Economic principles of supply and demand are being applied to analyze the rising rates of obesity in the United States.

- Research suggests obesity now has a stronger correlation with chronic medical conditions and healthcare costs than smoking or alcoholism.

Obesity appears to have a stronger association with the occurrence of chronic medical conditions, reduced physical health-related quality of life and increased health care and medication expenditures than smoking or problem drinking.

Economics of Rising Obesity

- Increased demand for food is driven by sedentary lifestyles and higher income levels, contributing to roughly 60% of weight gain.

- Modern life requires fewer calories to prepare food or earn the income to purchase it, compounding the physiological impact of caloric intake.

- Despite rising demand, the relative price of food has actually declined by 0.2% annually since World War II.

- Agricultural innovation has caused a massive rightward shift in the supply curve, which outweighs the shift in demand and lowers equilibrium prices.

- The remaining 40% of weight gain is attributed to these technological advancements in food production that make calories cheaper and more accessible.

What more apt picture of our sedentary life style is there than spending the afternoon watching a ballgame on TV, while eating chips and salsa, followed by a dinner of a lavishly topped, take-out pizza?

Market Equilibrium and Dynamics

- The law of demand dictates that price increases reduce quantity demanded, while the law of supply suggests price increases generally boost quantity supplied.

- Market equilibrium is reached at the intersection of demand and supply curves, where the quantity demanded exactly matches the quantity supplied.

- Prices above equilibrium create surpluses, while prices below equilibrium result in shortages, both of which are typically temporary in a functioning market.

- Changes in the underlying determinants of demand and supply shift the curves, resulting in new equilibrium prices and output levels.

- Economic logic can be applied to real-world safety issues, such as how airfare pricing indirectly influences highway fatality rates through substitution effects.

Usually, market surpluses and shortages are short-lived.

Economic Principles in Practice

- The text presents real-world scenarios to test the application of supply and demand models, such as how low-carb diet trends impact egg prices.

- It contrasts public perception of price gouging during peak travel seasons with the economic reality of seasonal demand shifts.

- Market dynamics are explored through historical shifts, including the rise of Vietnam as a coffee exporter and the transition of skim milk from hog feed to a primary consumer product.

- The relationship between substitute and complementary goods is examined through the correlation between rising cigarette prices and increased food consumption.

- Labor market imbalances are analyzed using the example of Indian outsourcing, where demand for college graduates outpaces the available supply.

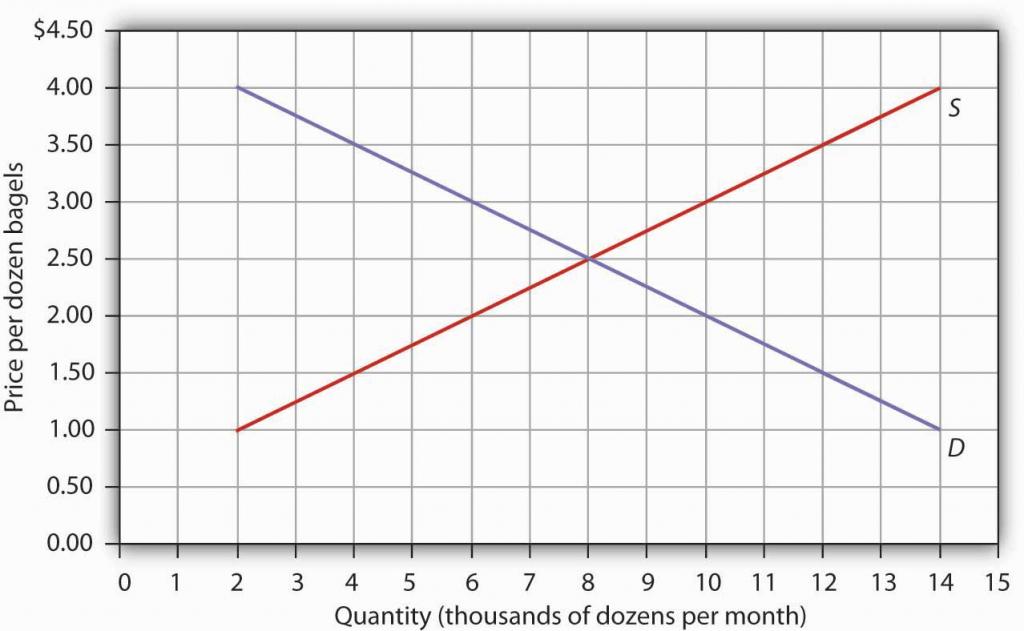

- Numerical problems provide a framework for calculating equilibrium price and quantity using specific data points for commodities like bagels and coffee.

I think the gas companies just use any excuse to jack up prices, and they’re doing it again now.

Market Equilibrium and Applications

- The text provides practical exercises for calculating shifts in demand and supply curves based on specific price and quantity changes.

- Students are tasked with identifying market surpluses and shortages by comparing quantity demanded and quantity supplied at various price points.

- A gasoline market case study illustrates how equilibrium is reached when quantity demanded equals quantity supplied at a specific price.

- The material introduces the concept of simultaneous shifts in both demand and supply, challenging students to predict outcomes for price and quantity.

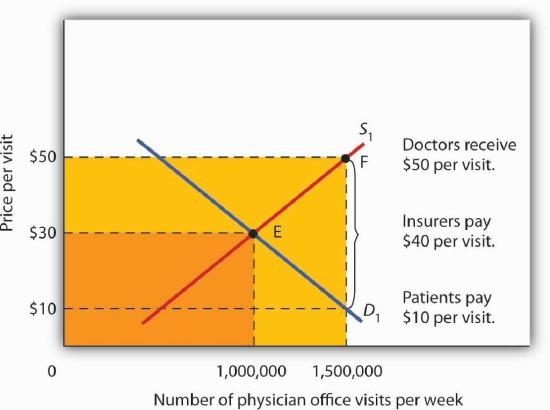

- The chapter transitions into real-world applications, including government interventions like price floors and ceilings and the health-care market.

- A focus is placed on how external factors, such as technological change, can be modeled using standard demand and supply frameworks.

If the demand curve shifts as in problem 13 and the supply curve shifts as in problem 14, without drawing a graph or consulting the data, can you predict whether equilibrium price increases or decreases?

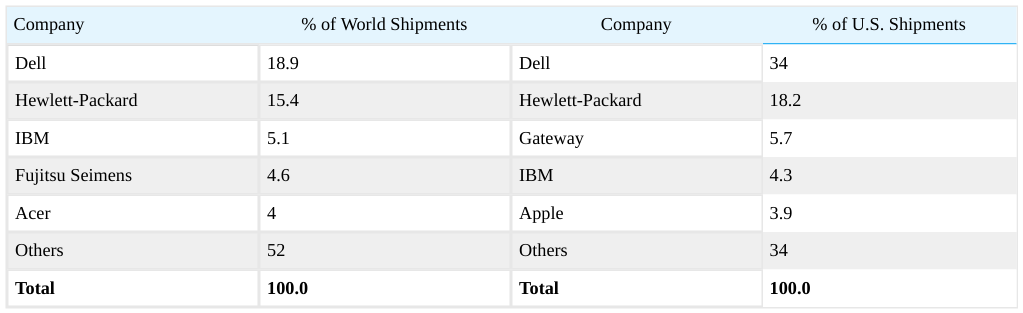

Evolution of the PC Market

- The model of demand and supply is used to analyze rapid price and quantity shifts in markets like crude oil, stocks, and personal computers.

- Technological advancement in the computer industry has been so rapid that economists must use 'quality-adjusted' metrics to compare hardware across different eras.

- The 'halving time' for the price of quality-adjusted desktop computers accelerated from 50 months in the late 70s to just 24 months by the late 90s.

- Explosive growth in hardware capability is evidenced by CPU speeds and hard drive capacities increasing by thousands of percentage points within single decades.

- The industry transitioned from a near-monopoly held by IBM in the mainframe era to a highly competitive global market with numerous manufacturers.

In 1984, just 8.2% of U.S. households owned a personal computer. By 2007, Google estimates that 78% did.

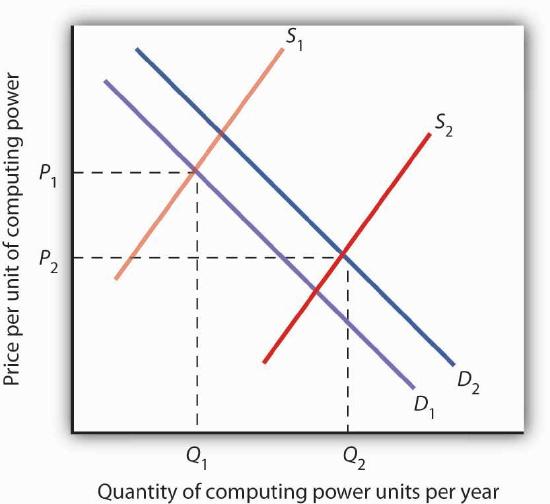

Market Shifts in Tech and Oil

- The personal computer market experienced a massive rightward supply shift due to technological advancements and increased competition, lowering prices despite rising demand.

- Computer demand grew simultaneously as rising incomes and new technologies like VoIP and RFID expanded the utility of computing power.

- Crude oil prices spiked to $147 per barrel in 2008, driven primarily by surging global demand from emerging economies like China outpacing production capacity.

- Rising energy costs act as a universal supply-side shock, shifting supply curves for nearly all goods and services to the left and increasing general price levels.

- The volatility of the oil market was demonstrated when the 2008 economic slowdown caused a rapid demand reversal, dropping prices from record highs to below $60 in months.

Higher oil prices also increase the cost of producing virtually every good or service, as at a minimum, the production of most goods requires transportation.

The Circular Flow of Capital

- The circular flow model posits that households supply factors of production, including capital, to firms.

- In exchange for providing capital, firms pay income back to the households.

- In practical reality, many large corporations like General Motors and Wal-Mart directly own their physical capital.

- There is a conceptual tension between the theoretical model of household ownership and the reality of corporate ownership.

- The relationship between firms and households remains the foundational link in macroeconomic resource distribution.

General Motors owns its assembly plants, and Wal-Mart owns its stores; these firms therefore own their capital.

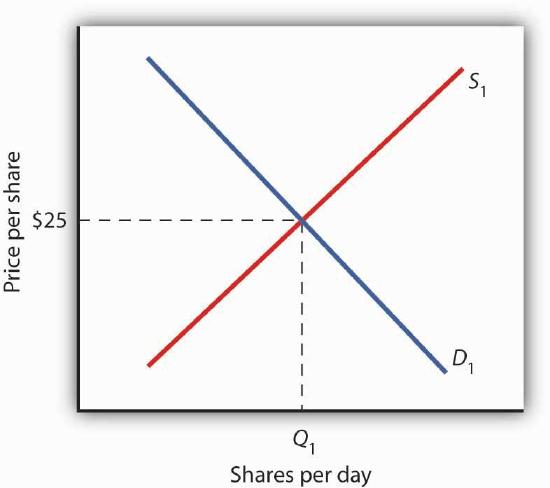

Mechanics of the Stock Market

- Households ultimately own all capital through their ownership of firms, whether as sole proprietorships, partnerships, or corporations.

- While most U.S. firms are small businesses, corporations produce approximately 90% of the nation's total output and own the majority of capital.

- Corporations only receive direct funding during an Initial Public Offering (IPO); subsequent trading occurs on the secondary market without further funding to the firm.

- Stock prices are determined by the interaction of supply and demand, where the supply curve represents the willingness of current owners to sell at various price points.

- The stock market functions as a global network of institutions where brokers and traders match buy and sell orders to reach equilibrium prices.

The process through which shares of stock are bought and sold can seem chaotic.

Mechanics of Stock Valuation

- Stock prices are determined by the intersection of supply and demand curves, representing the equilibrium between buyers and sellers.

- A share of stock represents a claim on a company's future profits, which are either reinvested as retained earnings or distributed as dividends.

- Because future profits are uncertain, stock prices are essentially market estimates based on product demand, production costs, and management quality.

- Shifts in supply and demand are primarily driven by changes in expectations; positive news shifts demand right and supply left, raising the price.

- Broader macroeconomic factors, such as demographic shifts toward retirement and overall economic health, influence general market price levels.

At the equilibrium price, the number of shares supplied by people who think holding the stock no longer makes sense just balances the number of shares demanded by people who think it does.

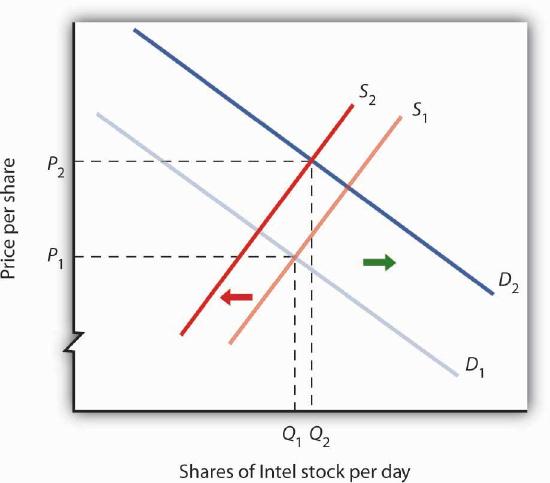

Market Volatility and Information

- Stock prices are constantly adjusted based on a continuous stream of new information, ranging from corporate profit reports to global geopolitical events.

- Technological advancements and shifts in global demand, such as the 2008 oil price fluctuations, demonstrate how supply and demand curves dictate equilibrium prices.

- Higher energy costs, like rising gasoline prices, create a systemic impact by shifting supply curves leftward, increasing prices while reducing output across industries.

- The equilibrium price of a stock represents a balance between market participants with opposing views on the asset's intrinsic value.

- Major disasters and 'complete surprises' like the 9/11 attacks cause dramatic short-term market declines by sapping consumer confidence and introducing extreme uncertainty.

The attacks on 9/11 provoked fear and uncertainty—two things that are certain to bring stock prices down, at least until other events and more information cause expectations to change again in this very responsive market.

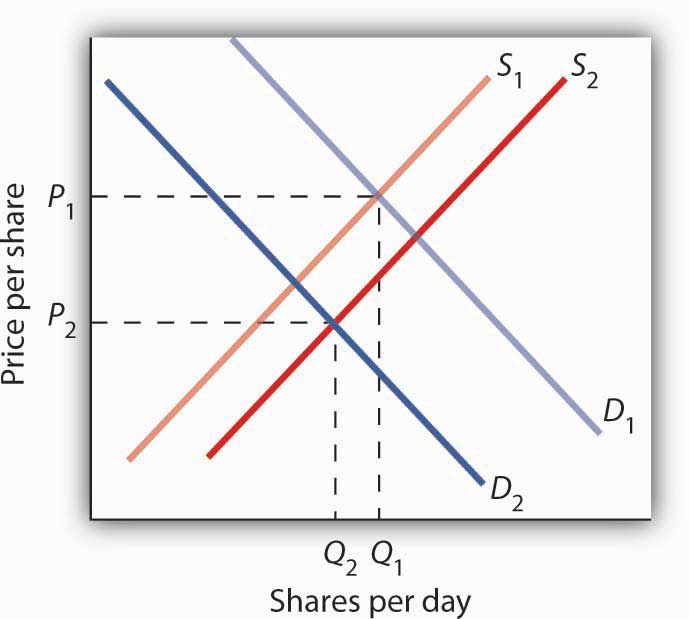

Market Equilibrium and Price Controls

- Negative information regarding a corporation's profitability causes a simultaneous increase in stock supply and a decrease in demand.

- While market shifts clearly drive down equilibrium prices, the final impact on equilibrium quantity depends on the relative magnitude of the shifts.

- Markets naturally tend toward equilibrium, where prices adjust to eliminate temporary surpluses and shortages.

- Governments often intervene in markets to artificially maintain prices above or below the natural equilibrium due to public pressure.

- Price floors in agriculture and price ceilings in rental markets serve as primary examples of government intervention and its consequences.

Surpluses and shortages of goods are short-lived as prices adjust to equate quantity demanded with quantity supplied.

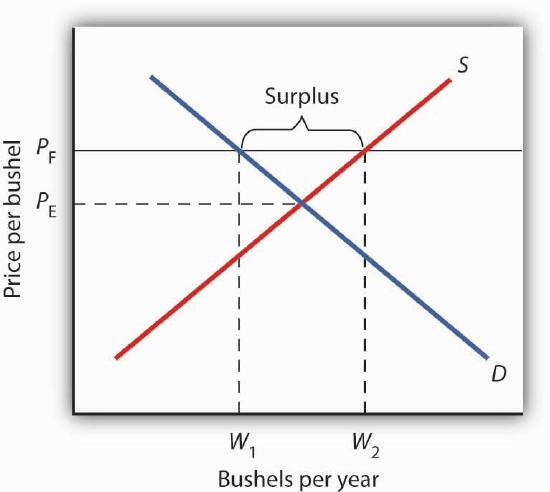

Agricultural Price Floors

- A price floor is a government-mandated minimum price set above the market equilibrium to prevent prices from falling.

- Setting a price floor above equilibrium results in a persistent surplus because the quantity supplied exceeds the quantity demanded.

- If a price floor is set below the equilibrium price, it remains irrelevant as it does not prevent the market from reaching its natural balance.

- Technological advancements in farming have significantly increased global production capacity, leading to downward pressure on crop prices.

- Farmers have successfully lobbied for these price floors to protect their income from the price-reducing effects of increased efficiency.

While such price reductions have been celebrated in computer markets, farmers have successfully lobbied for government programs aimed at keeping their prices from falling.

Agricultural Economics and Policy

- Technological advances have shifted the agricultural supply curve rightward far more significantly than the modest demand increases driven by population and income growth.

- The disparity between high supply and low demand growth has led to a long-term historical trend of falling equilibrium prices for agricultural goods.

- Farmers face extreme income instability due to short-term volatility caused by weather events and sudden shifts in international trade policy.

- The Great Depression served as a catalyst for federal intervention, as plummeting prices left over half of all farm loans in default by 1932.

- Government interventions have evolved from direct surplus purchasing and storage to 'target price' systems that pay farmers the difference between market rates and guaranteed minimums.

- To manage the surpluses created by price floors, the government often mandates acreage restrictions and conservation compliance from participating farmers.

Prices received by farmers plunged nearly two-thirds from 1930 to 1933.

Agricultural Subsidies and Reform

- Agricultural price support programs result in higher costs for consumers and significant government expenditure.

- U.S. federal spending on agriculture averaged over $22 billion annually between 2003 and 2007, costing roughly $70 per person.

- Farm aid often benefits large-scale producers rather than small farmers because subsidies are typically based on production volume.

- The 1996 FAIR Act attempted to phase out price supports to encourage market-based farming, but falling prices led to emergency aid.

- The 2008 farm bill increased subsidies to $40 billion while introducing the first income-based eligibility limits for wealthy farmers.

However, since farm aid has generally been allotted on the basis of how much farms produce rather than on a per-farm basis, most federal farm support has gone to the largest farms.

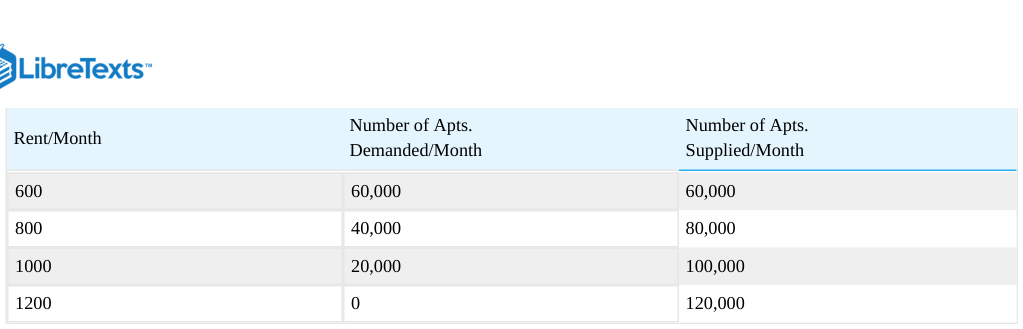

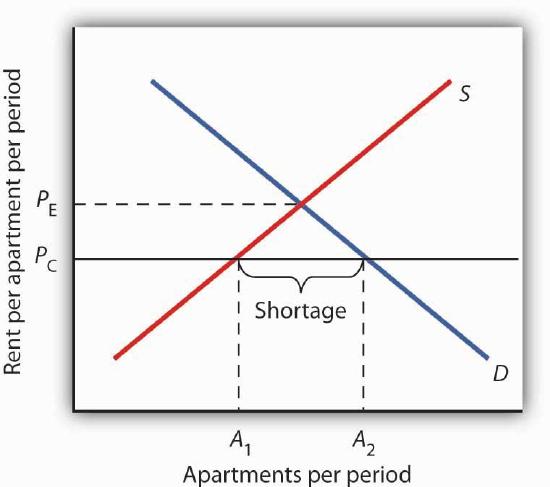

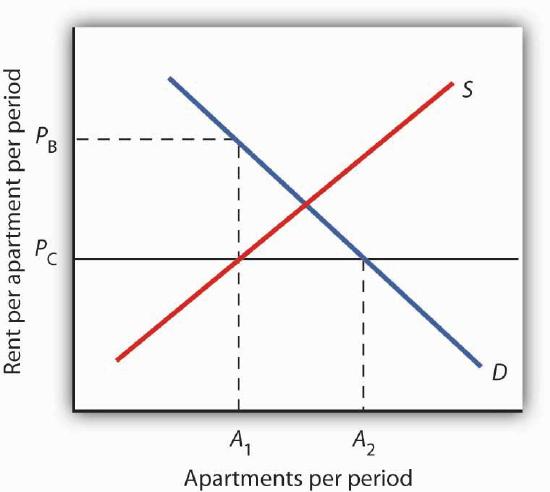

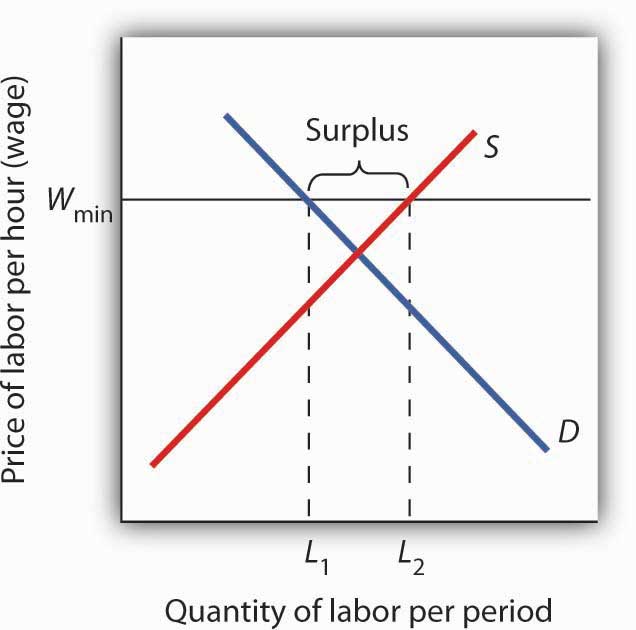

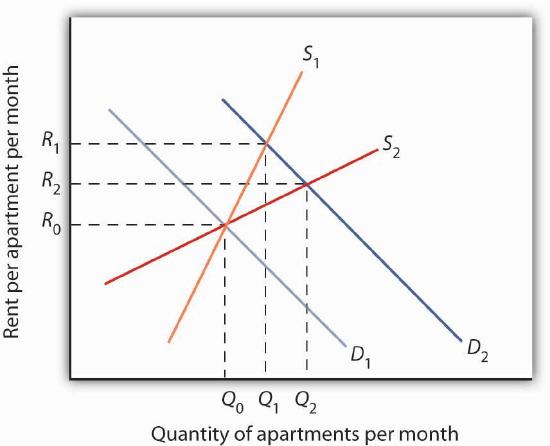

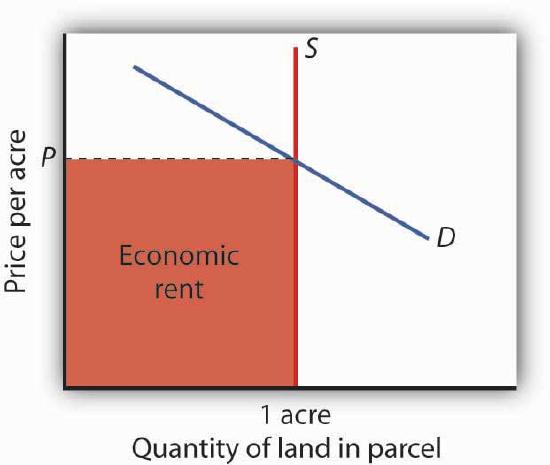

The Mechanics of Rent Control