printmgr file

Overview unavailable.

Global Offering Notice

- Introduces Knowledge Atlas Technology Joint Stock Company Limited’s global offering of H Shares on the Hong Kong Stock Exchange under stock code 2513.

- Sets out key offering terms, including 37,419,500 offer shares, a Hong Kong offer tranche and international tranche, and an offer price of HK$116.20 per share plus applicable fees and levies.

- Identifies the sponsor, coordinators, bookrunners and lead managers involved in the offering, while noting HKEX and regulators do not take responsibility for the prospectus contents.

- Highlights investor cautions, including the need to review risk factors, PRC/Hong Kong legal and regulatory differences, underwriting termination conditions, and U.S. offering restrictions.

- Notes the company is a Chapter 18C Specialist Technology Company with potentially high investment risks, and that the Hong Kong public offering uses a fully electronic application process.

Stock code: 2513

Knowledge Atlas Technology Joint Stock Company Limited

北京智譜華章科技股份有限公司

(A joint stock company established in the People’s Republic of China with limited liability)

GLOBAL

OFFERING

Sole Sponsor, Sponsor-Overall Coordinator, Overall Coordinator, Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager

Overall Coordinators, Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers

Joint Bookrunners and Joint Lead Managers

IMPORTANT

IMPORTANT: If you are in any doubt about any of the contents of this prospectus, you should seek independent professional advice.

Knowledge Atlas Technology Joint Stock Company Limited

北京智譜華章科技股份有限公司

(A joint stock company established in the People’s Republic of China with limited liability)

GLOBAL OFFERING

Number of Offer Shares under the Global Offering

37,419,500 H Shares (subject to the Over-allotment

Option)

Number of Hong Kong Offer Shares

1,871,000 H Shares (subject to reallocation)

Number of International Offer Shares

35,548,500 H Shares (subject to reallocation and the

Over-allotment Option)

Offer Price

HK$116.20 per H Share, plus brokerage of 1.0%, SFC

transaction levy of 0.0027%, Stock Exchange trading

fee of 0.00565% and AFRC transaction levy of

0.00015% (payable in full on application in Hong Kong

dollars and subject to refund)

Nominal value

RMB0.10 per H Share

Stock code

2513

Sole Sponsor, Sponsor-Overall Coordinator, Overall Coordinator,

Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager

Overall Coordinators, Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers

Joint Bookrunners and Joint Lead Managers

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents

of this prospectus, make no representation as to its accuracy or completeness, and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon

the whole or any part of the contents of this prospectus.

A copy of this prospectus, having attached thereto the documents specified in “Appendix VII—Documents Delivered to the Registrar of Companies and Documents on Display—A.

Documents Delivered to the Registrar of Companies” to this prospectus, has been registered by the Registrar of Companies in Hong Kong as required by section 342C of the Companies

(Winding Up and Miscellaneous Provisions) Ordinance (Chapter 32 of the Laws of Hong Kong). The Securities and Futures Commission and the Registrar of Companies in Hong Kong take

no responsibility for the contents of this prospectus or any other document referred to above.

The Offer Price will be HK$116.20 per Offer Share, unless otherwise announced. Applicants for Hong Kong Offer Share may be required to pay, on application (subject to application

channels), the Offer Price of HK$116.20 for each Hong Kong Offer Share together with a brokerage fee of 1.0%, a SFC transaction levy of 0.0027%, AFRC transaction levy of

0.00015% and a Hong Kong Stock Exchange trading fee of 0.00565%.

The Sponsor-Overall Coordinator (for and on behalf of the Underwriters) may, with the consent of our Company, reduce the number of Offer Shares and/or the Offer Price below that

stated in this prospectus at any time on or prior to the morning of the last date for lodging applications under the Hong Kong Public Offering. In such a case, notices of the reduction in

the number of Hong Kong Offer Shares and/or the Offer Price will be published on the websites of the Stock Exchange at www.hkexnews.hk and our Company at www.zhipuai.cn as

soon as practicable but in any event not later than the morning of the day which is the latest day for lodging applications under the Hong Kong Public Offering. For further information,

see the sections headed “Structure of the Global Offering” and “How to Apply for Hong Kong Offer Shares” in this prospectus.

Prior to making an investment decision, prospective investors should carefully consider all of the information set out in this prospectus, and in particular, the risk factors set out in the

section headed “Risk Factors.”

We are incorporated, and substantially all of our businesses are located, in the PRC. Potential investors should be aware of the differences in the legal, economic and financial systems

between the PRC and Hong Kong and that there are different risk factors relating to investment in PRC-incorporated businesses. Potential investors should also be aware that the

regulatory framework in the PRC is different from the regulatory framework in Hong Kong and should take into consideration the different market nature of the H Shares. Such

differences and risk factors are set out in “Risk Factors,” “Appendix IV—Summary of Principal Legal and Regulatory Provisions” and “Appendix V— Summary of Articles of

Association” to this Prospectus.

The obligations of the Hong Kong Underwriters under the Hong Kong Underwriting Agreement to subscribe for, and to procure applicants for the subscription for, the Hong Kong

Offer Shares are subject to termination by the Sponsor-Overall Coordinator (for and on behalf of the Hong Kong Underwriters) if certain grounds arise prior to 8:00 a.m. on the day

that trading in the H Shares commences on the Stock Exchange. Such grounds are set out in “Underwriting—Underwriting Arrangements and Expenses—The Hong Kong Public

Offering—Grounds for Termination” in this prospectus.

The Offer Shares have not been, and will not be, registered under the U.S. Securities Act or any state securities laws in the United States and may not be offered, sold, pledged or

otherwise transferred within the United States or to, or for the account or benefit of, any U.S. Investors. The Offer Shares will be offered and sold outside the United States to persons

that are not, and are not acting for the account or benefit of, U.S. Investors in offshore transactions in reliance on Regulation S. There has not been and will not be any public offering

of the H Shares in the United States.

Our Company is a Specialist Technology Company (as defined in Chapter 18C of the Listing Rules). The securities of Specialist Technology Companies carry high investment

risks including risks of share price volatility and inflated valuation due to the difficulty in valuing such companies. Investors should fully understand the investment risks of a

Specialist Technology Company and the risks disclosed by our Company before making their investment decisions.

ATTENTION

We have adopted a fully electronic application process for the Hong Kong Public Offering. We will not provide printed copies of this prospectus to the public in relation to the Hong

Kong Public Offering.

This prospectus is available at the website of the Hong Kong Stock Exchange at www.hkexnews.hk and our website at www.zhipuai.cn. If you require a printed copy of this

prospectus, you may download and print from the websites above.

December 30, 2025

IMPORTANT

Fully Electronic Application Process

- The Hong Kong Public Offering has transitioned to a fully electronic application process, eliminating the distribution of printed prospectus copies.

- Investors must access the prospectus digitally via the HKEXnews website or the company's official website at www.zhipuai.cn.

- Applications can only be submitted through two digital channels: the HK eIPO White Form service or the HKSCC EIPO channel via brokers.

- A strict minimum application of 100 Hong Kong Offer Shares is required, with further increments following specific tiered multiples.

- The maximum individual application is capped at 935,500 shares, representing 50% of the initial Hong Kong Offer Shares.

- Full payment or pre-funding is mandatory at the time of application, with costs ranging from approximately HK$11,737 to over HK$109 million.

We will not provide any physical channels to accept any application for the Hong Kong Offer Shares by the public.

IMPORTANT NOTICE TO INVESTORS

OF HONG KONG OFFER SHARES

FULLY ELECTRONIC APPLICATION PROCESS

We have adopted a fully electronic application process for the Hong Kong Public Offering

and below are the procedures for application. We will not provide printed copies of this

prospectus to the public in relation to the Hong Kong Public Offering.

This prospectus is available at the website of the Stock Exchange at www.hkexnews.hk

under the “HKEXnews > New Listings > New Listing Information” section, and our website at

www.zhipuai.cn. If you require a printed copy of this prospectus, you may download and print

from the website addresses above.

To apply for the Hong Kong Offer Shares, you may:

(1)

apply online through the HK eIPO White Form service through the designated website

www.hkeipo.hk; or

(2)

apply electronically through the HKSCC EIPO channel and cause HKSCC Nominees to apply

on your behalf by instructing your broker or custodian who is a HKSCC Participant to give

electronic application instructions via HKSCC’s FINI system to apply for the Hong Kong

Offer Shares on your behalf.

We will not provide any physical channels to accept any application for the Hong Kong Offer

Shares by the public. The contents of the electronic version of this prospectus are identical to the

printed document as registered with the Registrar of Companies in Hong Kong pursuant to Section

342C of the Companies (Winding Up and Miscellaneous Provisions) Ordinance.

If you are an intermediary, broker or agent, please remind your customers, clients or

principals, as applicable, that this prospectus is available online at the website addresses above. Please

refer to “How to Apply for Hong Kong Offer Shares” for further details of the procedures through

which you can apply for the Hong Kong Offer Shares electronically.

Your application through the HK eIPO White Form service or the HKSCC EIPO channel must

be made for a minimum of 100 Hong Kong Offer Shares and in multiples of that number of Hong

Kong Offer Shares as set out in the table below.

If you are applying through the HK eIPO White Form service, you may refer to the table below

for the amount payable for the number of H Shares you have selected. You must pay the respective

amount payable on application in full upon application for Hong Kong Offer Shares.

– ii –

IMPORTANT

If you are applying through the HKSCC EIPO channel, you are required to pre-fund your

application based on the amount specified by your broker or custodian, as determined based on the

applicable laws and regulations in Hong Kong.

No. of

Hong Kong

Offer Shares

applied for

Amount

payable(2) on

application/

successful

allotment

No. of

Hong Kong

Offer Shares

applied for

Amount

payable(2) on

application/

successful

allotment

No. of

Hong Kong

Offer Shares

applied for

Amount

payable(2) on

application/

successful

allotment

No. of

Hong Kong

Offer Shares

applied for

Amount

payable(2) on

application/

successful

allotment

HK$

HK$

HK$

HK$

100

11,737.19

2,500

293,429.69

30,000

3,521,156.31

600,000

70,423,126.20

200

23,474.37

3,000

352,115.63

40,000

4,694,875.08

700,000

82,160,313.90

300

35,211.56

3,500

410,801.57

50,000

5,868,593.86

800,000

93,897,501.60

400

46,948.75

4,000

469,487.51

60,000

7,042,312.62

935,500(1) 109,801,390.94

500

58,685.94

4,500

528,173.44

70,000

8,216,031.39

600

70,423.12

5,000

586,859.39

80,000

9,389,750.15

700

82,160.32

6,000

704,231.26

90,000 10,563,468.94

800

93,897.50

7,000

821,603.14

100,000 11,737,187.70

900 105,634.69

8,000

938,975.01

200,000 23,474,375.40

1,000 117,371.88

9,000 1,056,346.90

300,000 35,211,563.10

1,500 176,057.82

10,000 1,173,718.76

400,000 46,948,750.80

2,000 234,743.75

20,000 2,347,437.55

500,000 58,685,938.50

(1)

Maximum number of Hong Kong Offer Shares you may apply for and this is 50% of the Hong Kong Offer Shares

initially offered.

(2)

Hong Kong Offering Timetable

- The total payment for shares includes mandatory fees such as brokerage, SFC transaction levies, and Stock Exchange trading fees.

- The Hong Kong Public Offering is scheduled to commence on December 30, 2025, and conclude its application phase by January 5, 2026.

- Strict adherence to the specified number of shares is required, as non-compliant applications are subject to immediate rejection.

- Allocation results and interest levels will be disclosed across multiple digital platforms and a dedicated telephone enquiry line by January 7, 2026.

- Successful applicants will receive H Share certificates or have them deposited into the CCASS system by the final settlement date.

No application for any other number of Hong Kong Offer Shares will be considered and any such application is liable to be rejected.

The amount payable is inclusive of brokerage, SFC transaction levy, the Stock Exchange trading fee and AFRC

transaction levy. If your application is successful, brokerage will be paid to the Exchange Participants (as defined in

the Listing Rules) or to the HK eIPO White Form Service Provider (for applications made through the application

channel of the HK eIPO White Form service) while the SFC transaction levy, the Stock Exchange trading fee and

the AFRC transaction levy will be paid to the SFC, the Stock Exchange and the AFRC, respectively.

No application for any other number of Hong Kong Offer Shares will be considered and any such

application is liable to be rejected.

– iii –

EXPECTED TIMETABLE(1)

If there is any change in the following expected timetable of the Hong Kong Public Offering, we

will issue an announcement to be published on the websites of the Stock Exchange at

www.hkexnews.hk and our Company at www.zhipuai.cn.

Hong Kong Public Offering commences . . . . . . . . . .

9:00 a.m.

Tuesday, December 30, 2025

Latest time for completing applications under the HK

eIPO White Form service through the designated

website www.hkeipo.hk(2) . . . . . . . . . . . . . . . . . . .

11:30 a.m. on

Monday, January 5, 2026

Application lists of the Hong Kong Public Offering

open(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11:45 a.m. on

Monday, January 5, 2026

Latest time to (a) completing payments of HK eIPO

White Form applications by effecting internet

banking transfer(s) or PPS payment transfer(s) and

(b) giving electronic application instructions to

HKSCC(4)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

12:00 noon on

Monday, January 5, 2026

If you are instructing your broker or custodian who is a HKSCC Participant and will submit an

electronic application instructions on your behalf through HKSCC’s FINI system in accordance with your

instruction, you are advised to contact your broker or custodian for the earliest and latest time for giving

such instructions, as this may vary by broker or custodian.

Application lists of the Hong Kong Public Offering

close(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

12:00 noon on

Monday, January 5, 2026

Announcement of the level of applications in the

Hong Kong Public Offering; the level of

indications of interest in the International Offering;

and the basis of allocation of the Hong Kong Offer

Shares to be published on the websites of our

Company at www.zhipuai.cn(5) and the Stock

Exchange at www.hkexnews.hk . . . . . . . . . . . . . . .

at or before

11:00 p.m. on

Wednesday, January 7, 2026

The results of allocations in the Hong Kong Public Offering (with successful applicants’ identification

document numbers, where appropriate) to be made available through a variety of channels, including:

• in the announcement to be posted on the websites

of our Company at www.zhipuai.cn(6) and the

Stock

Exchange

at

www.hkexnews.hk,

respectively . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

at or before

11:00 p.m. on

Wednesday, January 7, 2026

– iv –

EXPECTED TIMETABLE(1)

• the “Allotment Results” page on the designated results of

allocations

website

at

www.tricor.com.hk/ipo/result

or

www.hkeipo.hk/IPOResult . . . . . . . . . . . . . . . . . . . . . . . . . . . .

from 11:00 p.m. on

Wednesday, January 7, 2026 to 12:00

midnight on Tuesday, January 13, 2026

• from the allocation results telephone enquiry line by calling

+852 3691 8488 between 9:00 a.m. and 6:00 p.m. . . . . . . . . . . .

from Thursday, January 8, 2026 to

Tuesday, January 13, 2026

(except Saturday, Sunday and

Hong Kong public holidays)

H Share certificates in respect of wholly or partially successful

applications to be despatched or deposited into CCASS . . . . . . .

on or before(6)

Wednesday, January 7, 2026

HK eIPO White Form e-Auto Refund payment instructions/

Hong Kong Listing Timetable

- The document outlines the critical dates for the public offering, including the commencement of H Share trading on January 8, 2026.

- Strict deadlines are established for the HK eIPO White Form service, with application submissions closing at 11:30 a.m. and payments at 12:00 noon.

- Contingency plans are in place for severe weather, such as 'black' rainstorm warnings or tropical cyclone signals, which may delay the opening of application lists.

- H Share certificates only become valid evidence of title at 8:00 a.m. on the Listing Date, provided the Global Offering becomes unconditional.

- Refunds for unsuccessful or partially successful applications are scheduled for dispatch on or before the trading commencement date.

- Investors are warned that trading based on allocation details prior to the validation of share certificates is done entirely at their own risk.

Investors who trade the H Shares on the basis of publicly available allocation details prior to the receipt of H Share certificates or prior to the H Share certificates becoming valid evidence of title do so entirely at their own risk.

refund checks in respect of wholly or partially successful

applications (if applicable) or wholly or partially unsuccessful

applications to be despatched . . . . . . . . . . . . . . . . . . . . . . . . . . . .

on or before(7)(8)

Thursday, January 8, 2026

Dealings in the H Shares on the Main Board of the Stock

Exchange to commence at

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9:00 a.m. on

Thursday, January 8, 2026

Notes:

(1)

All dates and times refer to Hong Kong local dates and times, except as otherwise stated.

(2)

You will not be permitted to submit your application under the HK eIPO White Form service through the designated website at

www.hkeipo.hk after 11:30 a.m. on the last day for submitting applications. If you have already submitted your application and

obtained an application reference number from the designated website prior to 11:30 a.m., you will be permitted to continue the

application process (by completing payment of the application monies) until 12:00 noon on the last day for submitting

applications, when the application lists close.

(3)

If there is/are a “black” rainstorm warning signal, a tropical cyclone warning signal number 8 or above and/or Extreme

Conditions in force in Hong Kong at any time between 9:00 a.m. and 12:00 noon on Monday, January 5, 2026, the application

lists will not open or close on that day. See the section headed “How to Apply for Hong Kong Offer Shares—E. Severe Weather

Arrangements” for further details.

(4)

Applicants who apply for Hong Kong Offer Shares by giving electronic application instructions to HKSCC via HKSCC’s

FINI system should refer to the section headed “How to Apply for Hong Kong Offer Shares—A. Applications for Hong Kong

Offer Shares—2. Application Channels”.

(5)

None of the websites or any of the information contained on the websites forms part of this prospectus.

(6)

The H Share certificates will only become valid evidence of title at 8:00 a.m. on the Listing Date provided that the Global

Offering has become unconditional in all respects. Investors who trade the H Shares on the basis of publicly available allocation

details prior to the receipt of H Share certificates or prior to the H Share certificates becoming valid evidence of title do so

entirely at their own risk.

(7)

HK eIPO White Form e-Auto Refund payment instructions/refund checks will be issued in respect of wholly or partially

unsuccessful applications pursuant to the Hong Kong Public Offering and in respect of wholly or partially successful applicants.

Part of the applicant’s identification document number, or, if the application is made by joint applicants, part of the identification

document number of the first-named applicant, provided by the applicant(s) may be printed on the refund check, if any. Such

– v –

EXPECTED TIMETABLE(1)

data would also be transferred to a third party for refund purposes. Banks may require verification of an applicant’s

identification document number before encashment of the refund check. Inaccurate completion of an applicant’s identification

document number may invalidate or delay encashment of the refund check.

(8)

Share Collection and Refund Procedures

- Applicants for 500,000 or more shares via HK eIPO White Form must collect certificates in person at the Far East Finance Centre.

- Individual applicants are strictly prohibited from authorizing third parties to collect certificates on their behalf.

- Refunds are processed via e-Auto Refund for single bank account users, while multiple bank account users receive physical checks by post.

- Small-scale applicants (under 500,000 shares) will receive all documentation via ordinary post at their own risk.

- The Global Offering is contingent upon becoming unconditional; if terminated, the company will issue a formal announcement.

- This prospectus is legally restricted to the Hong Kong Public Offering and does not constitute an offer in any other jurisdiction.

Applicants being individuals who are eligible for personal collection may not authorize any other person to collect on their behalf.

Applicants who have applied on the HK eIPO White Form service for 500,000 or more Hong Kong Offer Shares may collect

H Share certificates in person from our H Share Registrar, Tricor Investor Services Limited, at 17/F, Far East Finance Centre,

16 Harcourt Road, Hong Kong from 9:00 a.m. to 1:00 p.m. on Thursday, January 8, 2026 or any other places or date as notified

by us as the date of despatch/collection of H Share certificates/HK eIPO White Form e-Auto Refund payment instructions/

refund checks. Applicants being individuals who are eligible for personal collection may not authorize any other person to

collect on their behalf. Individuals must produce evidence of identity acceptable to our H Share Registrar at the time of

collection.

Applicants who have applied for Hong Kong Offer Shares through HKSCC EIPO channel should refer to “How to Apply for

Hong Kong Offer Shares—D. Despatch/Collection of H Share Certificates and Refund of Application Monies” for details.

Applicants who have applied through the HK eIPO White Form service and paid their applications monies through single bank

accounts may have refund monies (if any) despatched to the bank account in the form of HK eIPO White Form e-Auto Refund

payment instructions. Applicants who have applied through the HK eIPO White Form service and paid their application

monies through multiple bank accounts may have refund monies (if any) despatched to the address as specified in their

application instructions in the form of refund checks in favor of the applicant (or, in the case of joint applications, the first-

named applicant) by ordinary post at their own risk.

The H Share certificates and/or refund checks for applicants who have applied for less than 500,000 Hong Kong Offer Shares

and any uncollected H Share certificates will be despatched by ordinary post, at the applicants’ risk, to the addresses specified in

the relevant applications.

Further information is set out in the section headed “How to Apply for Hong Kong Offer Shares—D. Despatch/Collection of

H Share Certificates and Refund of Application Monies.”

The above expected timetable is a summary only. For details of the structure of the Global Offering,

including its conditions, and the procedures for applications for Hong Kong Offer Shares, see “Structure of

the Global Offering” and “How to Apply for Hong Kong Offer Shares,” respectively.

If the Global Offering does not become unconditional or is terminated in accordance with its terms, the

Global Offering will not proceed. In such a case, our Company will make an announcement as soon as

practicable thereafter.

– vi –

CONTENTS

IMPORTANT NOTICE TO PROSPECTIVE INVESTORS

This prospectus is issued by our Company solely in connection with the Hong Kong Public

Offering and does not constitute an offer to sell or a solicitation of an offer to buy any security other

than the Hong Kong Offer Shares offered by this prospectus pursuant to the Hong Kong Public

Offering. This prospectus may not be used for the purpose of, and does not constitute, an offer or a

solicitation of an offer to subscribe for or buy any security in any other jurisdiction or in any other

circumstances. No action has been taken to permit a public offering of the Offer Shares or the

distribution of this prospectus in any jurisdiction other than Hong Kong. The distribution of this

prospectus and the offering and sale of the Offer Shares in other jurisdictions are subject to

restrictions and may not be made except as permitted under the applicable securities laws of such

jurisdictions pursuant to registration with or authorization by the relevant securities regulatory

Prospectus Disclaimers and Contents

- Investors are strictly cautioned to rely only on the information explicitly provided within the prospectus document.

- The company disclaims any responsibility for unauthorized information or representations made by third parties, including underwriters and directors.

- Official digital content on the company's website is explicitly excluded from forming part of the legal prospectus.

- The document outlines a comprehensive structure covering risk factors, regulatory overviews, and detailed financial information.

- A significant portion of the document is dedicated to the business operations, history, and corporate structure of Zhipu AI.

Information contained on our website, located at www.zhipuai.cn, does not form part of this prospectus.

authorities or an exemption therefrom.

You should rely only on the information contained in this prospectus to make your

investment decision. We have not authorized anyone to provide you with information that is

different from what is contained in this prospectus. Any information or representation not made in

this prospectus must not be relied on by you as having been authorized by us, the Sole Sponsor,

Sponsor-Overall Coordinator, the Overall Coordinators, the Joint Global Coordinators, the Joint

Bookrunners, the Joint Lead Managers, the Capital Market Intermediaries, any of the

Underwriters, any of our or their respective directors, officers or representatives, or any other

person or party involved in the Global Offering. Information contained on our website, located at

www.zhipuai.cn, does not form part of this prospectus.

Page

EXPECTED TIMETABLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

iv

CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

vii

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

DEFINITIONS AND ACRONYMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

24

GLOSSARY OF TECHNICAL TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

36

FORWARD-LOOKING STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

39

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

40

WAIVERS FROM STRICT COMPLIANCE WITH THE REQUIREMENTS UNDER THE

LISTING RULES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

67

INFORMATION ABOUT THIS PROSPECTUS AND THE GLOBAL OFFERING . . . . . . . . .

72

DIRECTORS, SUPERVISOR AND PARTIES INVOLVED IN THE GLOBAL

OFFERING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

75

CORPORATE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

80

INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

82

REGULATORY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

95

– vii –

CONTENTS

Page

HISTORY, DEVELOPMENT AND CORPORATE STRUCTURE . . . . . . . . . . . . . . . . . . . . . . .

113

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

145

DIRECTORS, SUPERVISOR AND SENIOR MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . .

223

RELATIONSHIP WITH OUR CONTROLLING SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . .

235

SUBSTANTIAL SHAREHOLDERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

238

SHARE CAPITAL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

242

FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

245

CORNERSTONE INVESTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

291

FUTURE PLANS AND USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

299

UNDERWRITING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

302

Global Offering and AI Leadership

- The document outlines the structure and legal appendices for a specialist technology company's initial public offering on the Hong Kong Stock Exchange.

- The company is seeking a listing under Chapter 18C of the Listing Rules, a specific pathway for technology companies that do not meet standard financial requirements.

- Founded in 2019, the firm is a leading Chinese AI developer focused on Artificial General Intelligence (AGI) and the Model-as-a-Service (MaaS) platform.

- The company launched GLM, China’s first proprietary pre-trained large model framework, and open-sourced a 100 billion-scale model in 2022.

- Market data shows significant growth with a revenue CAGR of over 130% between 2022 and 2024, capturing a 6.6% market share in China's general-purpose large model sector.

In particular, we are a specialist technology company seeking to list on the Main Board of the Hong Kong Stock Exchange under Chapter 18C of the Listing Rules because we are unable to meet the requirements under Rule 8.05(1), (2) or (3) of the Listing Rules.

STRUCTURE OF THE GLOBAL OFFERING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

313

HOW TO APPLY FOR HONG KONG OFFER SHARES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

321

APPENDIX I

ACCOUNTANTS’ REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

I-1

APPENDIX II

UNAUDITED PRO FORMA FINANCIAL INFORMATION . . . . . . . . . . . .

II-1

APPENDIX III

TAXATION AND FOREIGN EXCHANGE . . . . . . . . . . . . . . . . . . . . . . . . . .

III-1

APPENDIX IV

SUMMARY OF PRINCIPAL LEGAL AND REGULATORY

PROVISIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

IV-1

APPENDIX V

SUMMARY OF ARTICLES OF ASSOCIATION . . . . . . . . . . . . . . . . . . . . .

V-1

APPENDIX VI

STATUTORY AND GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . .

VI-1

APPENDIX VII

DOCUMENTS DELIVERED TO THE REGISTRAR OF COMPANIES

AND DOCUMENTS ON DISPLAY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

VII-1

– viii –

SUMMARY

This summary aims to give you an overview of the information contained in this prospectus. As

this is a summary, it does not contain all the information that may be important to you. You should

read this prospectus in its entirety before you decide to invest in the Offer Shares. In particular, we are

a specialist technology company seeking to list on the Main Board of the Hong Kong Stock Exchange

under Chapter 18C of the Listing Rules because we are unable to meet the requirements under Rule

8.05(1), (2) or (3) of the Listing Rules. There are unique challenges, risks and uncertainties associated

with investing in companies such as us. Your investment decision should be made in light of these

considerations.

There are risks associated with any investment. Some of the particular risks in investing in the

Offer Shares are set out in “Risk Factors” of this prospectus. You should read that section carefully

before you decide to invest in the Offer Shares. Your investment decision should be made in light of

these considerations.

OVERVIEW

Who We Are

We are a leading AI company in China, dedicated to developing general-purpose large models. We

were founded in 2019 on the bold idea of pursuing innovation toward artificial general intelligence (AGI) in

China. We have solidly delivered advanced technology across the full spectrum of AI research and steadily

scaled up its commercial application to achieve fast growth in revenue. In 2021, we launched GLM

framework, China’s first proprietary pre-trained large model framework, and debuted our Model-as-a-

Service (MaaS) product development and commercialization platform, through which we provide our large

model services. In 2022, we open-sourced our first 100 billion–scale model (GLM-130B). We operate in the

large language model (LLM) market, a sub-segment of the broader AI market. We offer general-purpose

large model services to institutional customers, including private enterprises and public sector entities, as

well as individual users, including individual end-users and individual developers. Our models had

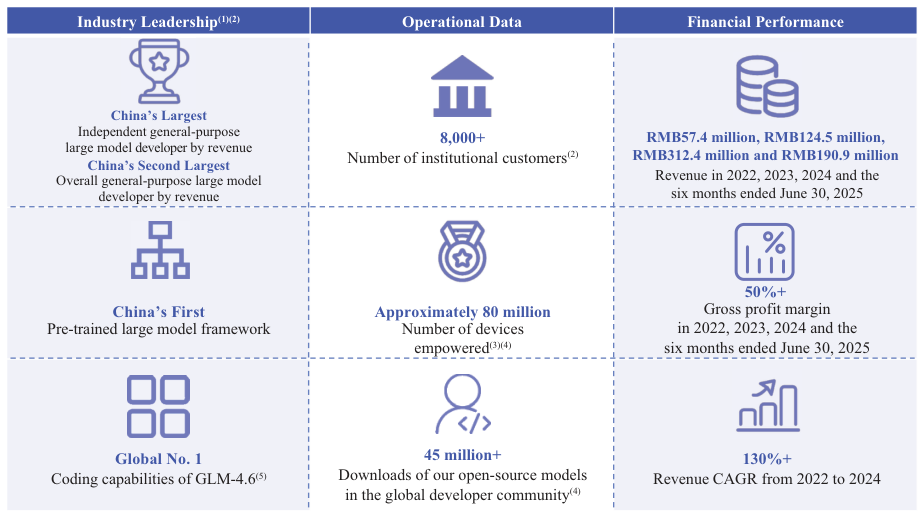

empowered over eight thousand institutional customers as of June 30, 2025 and approximately 80 million

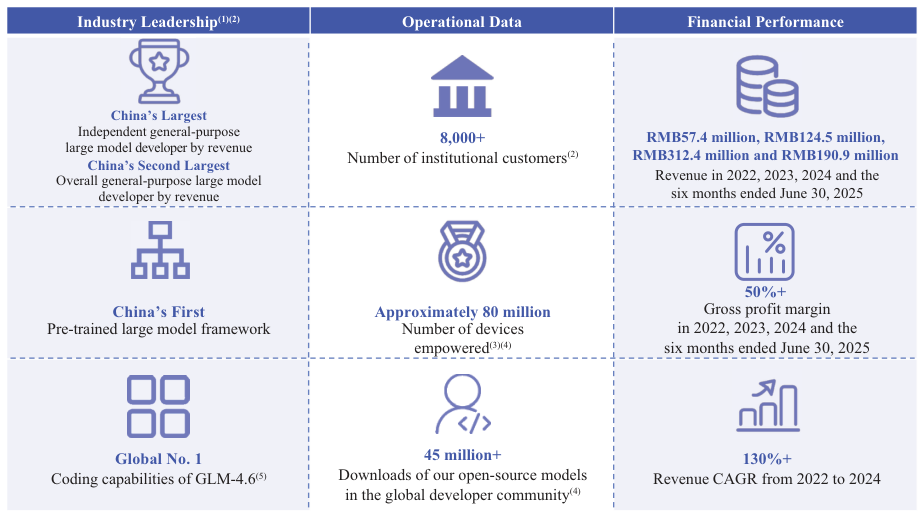

devices as of the Latest Practicable Date. According to Frost & Sullivan, we ranked first among China’s

independent developers and second among all developers of general-purpose large models with a market

share of 6.6% in terms of revenue in 2024.

– 1 –

SUMMARY

We achieved significant growth in revenue during the Track Record Period. In 2022, 2023 and 2024,

our revenue was RMB57.4 million, RMB124.5 million and RMB312.4 million, respectively, representing a

CAGR of over 130%. For the six months ended June 30, 2024 and 2025, our revenue was RMB44.9 million

and RMB190.9 million, respectively.

Industry Leadership(1)(2)

Operational Data

Financial Performance

Global No. 1

RMB57.4 million, RMB124.5 million,

China's Leading MaaS Platform

- The company ranks as China's largest independent general-purpose large model developer by revenue as of 2025.

- Their business model centers on a Model-as-a-Service (MaaS) platform offering language, multimodal, agent, and coding models.

- The platform demonstrates significant growth with a revenue CAGR exceeding 130% from 2022 to 2024.

- Global reach is evidenced by over 45 million downloads of open-source models and empowerment of approximately 80 million devices.

- The MaaS architecture is built on three pillars: a comprehensive model portfolio, scalable applications, and easy infrastructure adaptability.

- The GLM-4.6 model achieved top-tier global rankings for coding capabilities on the CodeArena evaluation platform in late 2025.

Through this product development and commercialization platform, we deliver intelligence to institutional customers, developers and individual customers in the most suitable, sensible and scalable way despite great heterogeneity in computing infrastructure, devices and applications.

RMB312.4 million and RMB190.9 million

China’s First

130%+

45 million+

Approximately 80 million

50%+

China’s Largest

China’s Second Largest

8,000+

Independent general-purpose

large model developer by revenue

Overall general-purpose large model

developer by revenue

Number of institutional customers(2)

Revenue in 2022, 2023, 2024 and the

six months ended June 30, 2025

Gross profit margin

in 2022, 2023, 2024 and the

six months ended June 30, 2025

Revenue CAGR from 2022 to 2024

Downloads of our open-source models

in the global developer community(4)

Number of devices

empowered(3)(4)

Coding capabilities of GLM-4.6(5)

Pre-trained large model framework

Notes:

(1)

According to Frost & Sullivan.

(2)

As of June 30, 2025.

(3)

Including smart phones, personal computers and smart vehicles.

(4)

As of the Latest Practicable Date.

(5)

Ranked in November 2025 by CodeArena, the latest industry-recognized global evaluation platform designed to assess models’ coding

capabilities.

– 2 –

SUMMARY

OUR BUSINESS MODEL: THE MAAS PLATFORM

As we commercialize our technology to seize the tremendous market opportunity presented by

advanced AI, we organize our offerings around our all-in-one MaaS platform. Our MaaS platform primarily

offers four types of models: language models, multimodal models, agent models and coding models, as well

as integrated tools for model fine-tuning, deployment and agent development. The key features of our MaaS

platform are comprehensiveness in model capabilities, scalability across broad application scenarios and

adaptability

with

diverse

computing

infrastructure.

Through

this

product

development

and

commercialization platform, we deliver intelligence to institutional customers, developers and individual

customers in the most suitable, sensible and scalable way despite great heterogeneity in computing

infrastructure, devices and applications.

Internet

Financial

Services

Technology

Smart

Devices

Healthcare

Retail

Scalable

Applications

Comprehensive

Portfolio

Model

Easy

Infra

Adaptability

Compatibility with

Computing Resources

Standardized API Access

MaaS

Language Model

Agent Model

Multimodal Model

Coding Model

Computing Power Support

……

Flexible Custom

Model Deployment

MaaS in the

loop

Safe and Accessible

Our MaaS platform comprises the following three levels:

•

Comprehensive model portfolio. We have built a comprehensive portfolio of advanced AI models,

showcasing

industry-leading

performance

in

language,

multimodal,

agentic

and

coding

capabilities. From our broad and capable repertoire, customers and developers can always find the

most suitable solution for their specific needs.

•

Scalable applications. Our models and agents are designed for seamless functionality across

diverse hardware, application scenarios and business workflows. They are capable of handling

complex tasks, enabling AI-native, multimodal and holistic dialogs, and performing deep

reasoning. For example, our models and agents can assist institutional customers in streamlining

business workflows, processing and analyzing operating data at a massive scale and supporting

decision-making. In addition, our MaaS platform provides an agent workspace, which

encompasses a variety of agent templates and scenario-based solutions. Through this agent

workspace, our customers can swiftly customize agents through streamlined model fine-tuning,

incremental model training and prompt engineering.

•

Easy infra adaptability. In collaboration with our computing infrastructure partners, we co-design

an advanced computing infrastructure that enables our MaaS platform to deliver integrated

computing, networking, training communications and inference acceleration capabilities. The

MaaS Deployment and Model Architecture

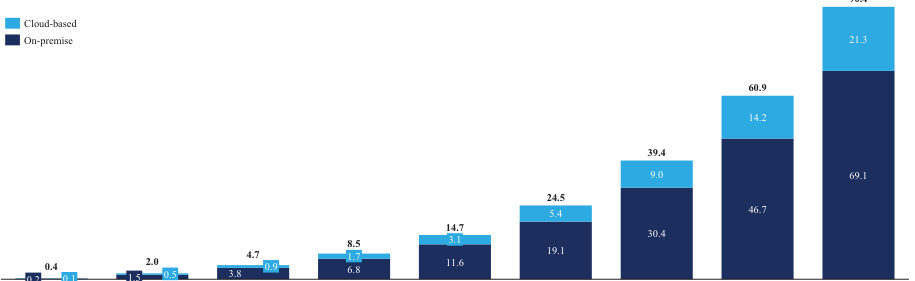

- The Model-as-a-Service (MaaS) platform supports a wide range of model sizes from 1.5 billion to 230 billion parameters for diverse hardware.

- On-premise deployment provides organizations with greater control over data security and performance optimization for specialized domains.

- Cloud-based deployment offers agility and cost-effectiveness by eliminating the need for local infrastructure and utilizing usage-based pricing.

- The AI development strategy focuses on three core human faculties: deep thinking, cognition, and tool use.

- The GLM series foundation models serve as the base for specialized reflection, multimodal, agent, and coding models.

- Revenue recognition varies by deployment type, occurring at delivery for on-premise solutions and over the contract term for cloud services.

To teach machines to think like humans, we must empower AI with three core human faculties: deep thinking, cognition and tool use.

collaboration also enables our models to offer broad adaptability, supporting model sizes ranging

from 1.5 billion to 230 billion parameters and large-scale, real-time deployment across clouds and

chipsets. In particular, such adaptability allows our models to scale across mass-use devices such

as mobile phones, personal computers and smart vehicles and benefit vast numbers of end

consumers.

– 3 –

SUMMARY

Our MaaS platform offers flexible custom model deployment options to meet the diverse needs of

businesses while maintaining efficiency, scalability and data security. We primarily offer two deployment

approaches—on-premise and cloud-based deployment:

•

For on-premise deployment, our models are hosted within the customer’s own infrastructure. This

approach allows organizations to utilize their proprietary or sensitive data to tailor AI models to

their specific domains. On-premise deployment offers greater control over performance

optimization and infrastructure configuration, making it suitable for complex or highly specialized

application scenarios.

•

For cloud-based deployment, our models are hosted on a scalable and reliable cloud

infrastructure.

This

approach

is

sensible

for

businesses

seeking

agility

and

ease

of

implementation. By utilizing the cloud, customers eliminate the need for costly local

infrastructure, allowing them to deploy AI solutions quickly and cost effectively.

For on-premise deployment, we recognize revenue at the point in time when the large model and

related services are delivered to the customer’s designated location and accepted by the customer. For

cloud-based deployment, we recognize revenue over the contract term. Specifically, for subscription-based

contracts, we generally recognize revenue ratably over the contract term; for usage-based contracts, we

recognize revenue based on the customer’s utilization of the resources when the services are rendered to the

customers. For details of our revenue recognition policies, see “Financial Information—Material

Accounting Policies and Estimates—Material Accounting Policy Information—Revenue Recognition.”

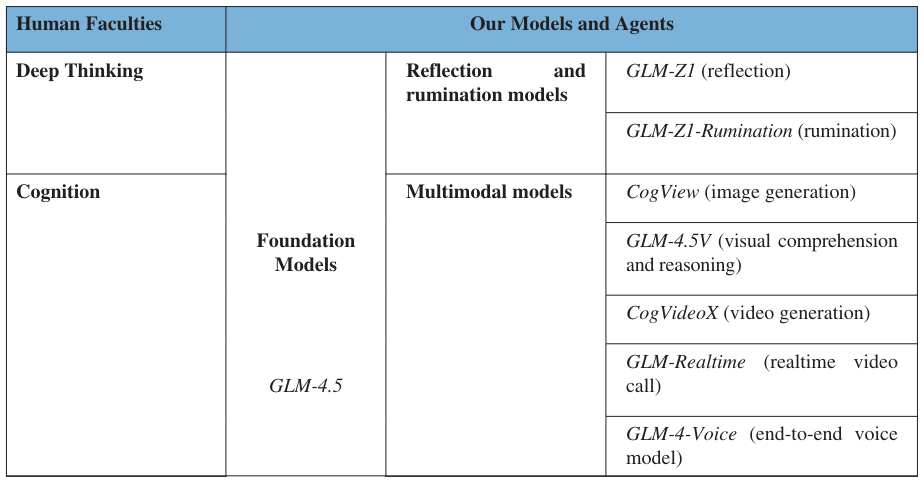

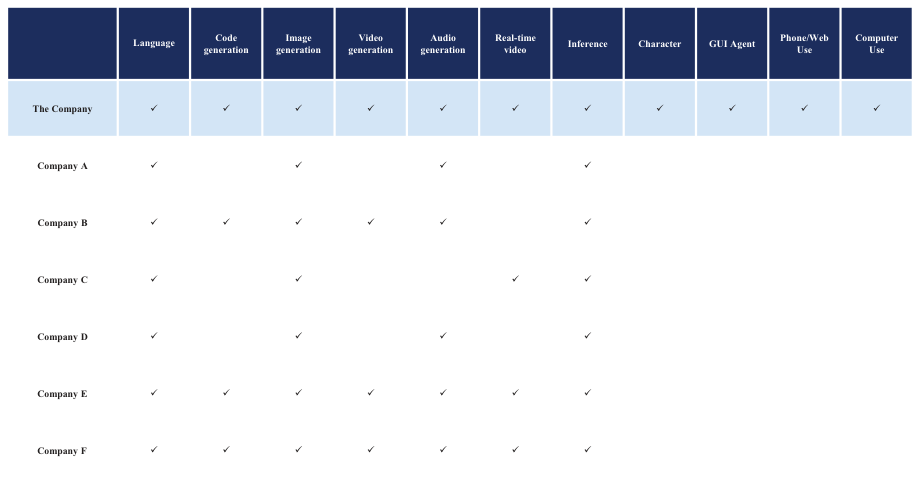

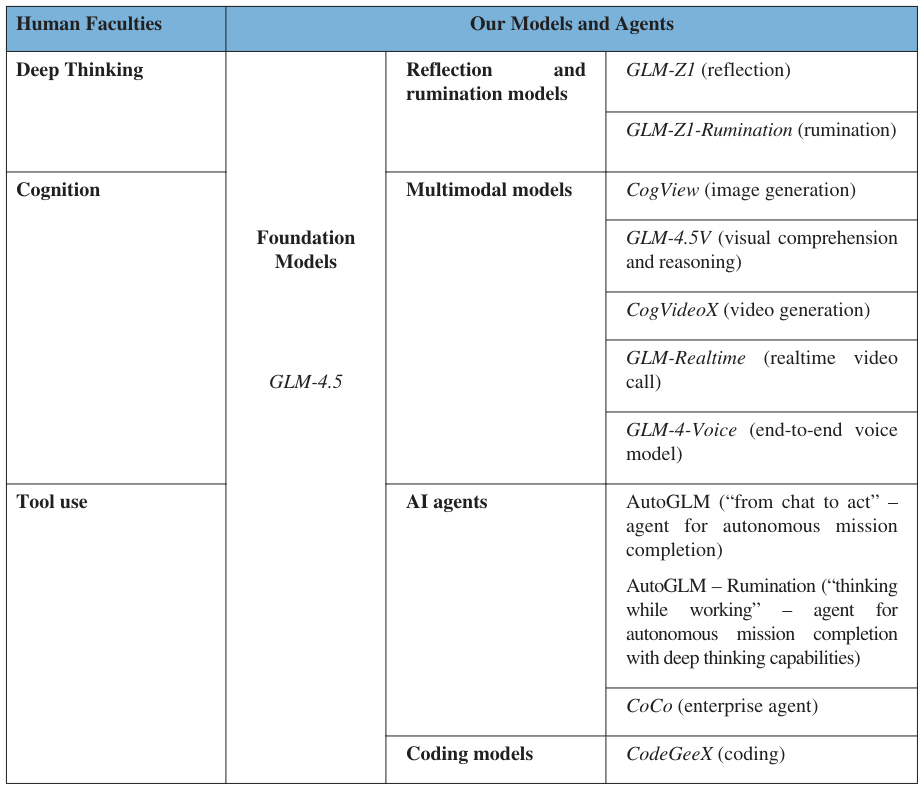

OUR MODELS AND AGENTS

To teach machines to think like humans, we must empower AI with three core human faculties: deep

thinking, cognition and tool use. We have developed our AI models accordingly, which can be grouped into

three corresponding categories: reflection and rumination models, multimodal models and agent models.

We have also developed coding models, which generate code autonomously and enhance programming

efficiency. All four categories are developed upon our GLM series of foundation models. Foundation

models and reflection and rumination models belong to the broader category of language models.

The following chart sets forth our select models and AI agents in our current portfolio:

Human Faculties

Our Models and Agents

Deep Thinking

Reflection

and

rumination models

GLM-Z1 (reflection)

GLM-Z1-Rumination (rumination)

Cognition

Multimodal models

CogView (image generation)

Foundation

Models

GLM-4.5V (visual comprehension

and reasoning)

CogVideoX (video generation)

GLM-4.5

GLM-Realtime

(realtime

video

call)

GLM-4-Voice (end-to-end voice

model)

– 4 –

SUMMARY

Human Faculties

Our Models and Agents

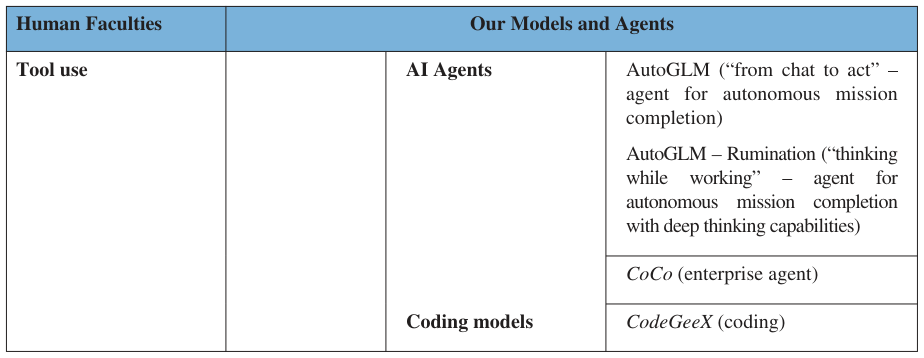

Tool use

AI Agents

AutoGLM (“from chat to act” –

agent for autonomous mission

completion)

AutoGLM – Rumination (“thinking

while

working”

–

agent

for

autonomous

mission

completion

with deep thinking capabilities)

CoCo (enterprise agent)

Coding models

CodeGeeX (coding)

Foundation Models

Foundation models are pre-trained LLMs that serve as the foundation for the development of a variety

of specialized models. GLM-4.5 is our flagship foundation model, which we open-sourced upon launch.

Through multi-stage training and comprehensive post-training with fine-tuning and reinforcement learning,

GLM-4.5 Performance and Benchmarks

- GLM-4.5 is a 355-billion-parameter model that excels in agentic, reasoning, and coding tasks while supporting multi-modal extensions.

- The model ranked first among global open-source models and first in China across twelve industry-standard benchmark tests in July 2025.

- GLM-4.5 achieved the world's second-lowest hallucination rate in RAG evaluations, indicating high reliability in avoiding non-existent answers.

- Market adoption is significant, with token consumption on OpenRouter consistently ranking among the top ten globally and top three for Chinese companies.

- The product line includes specialized versions like GLM-4.5-Air for efficiency and the GLM-Z1 series for 'deep thinking' and complex reasoning.

Reflection and rumination models spend additional time “deep thinking” before generating an answer, which makes them better for complex reasoning tasks.

GLM-4.5 achieves strong performance across agentic, reasoning and coding tasks. GLM-4.5 also supports

multi-modal extensions and large context processing, allowing it to interpret high-level prompts and

autonomously generate practical solutions. GLM-4.5 has a model scale of 355 billion parameters and we

have also developed GLM-4.5-Air, a lightweight version with 106 billion parameters.

GLM-4.5 achieves the following leading positions, according to Frost & Sullivan:

•

Benchmark tests. Based on an evaluation across twelve industry-standard benchmark tests1 in July

2025, GLM-4.5 ranked third globally, first in China and first among global open-source models.

GLM-4.5 achieved a comprehensive score of 63.2 under these twelve benchmarks, compared with

scores ranging from 46.3 to 65.0 for industry peer models.

•

Global leaderboards. GLM-4.5 ranked fifth globally on Chatbot Arena and WebDev Arena in

September 2025, which are industry-recognized global leaderboards that rank the overall

capabilities and coding capabilities of large models, respectively.

•

Token consumption volume. Since the launch of GLM-4.5 and up to early December 2025, our

token consumption volume on OpenRouter, a leading global platform that provides API access to

a wide range of large models, had consistently ranked among the top ten globally and the top

three

among

Chinese

companies.

This

sustained

performance

underscores

the

strong

competitiveness and market recognition of GLM-4.5, demonstrating its advanced efficiency,

scalability and real-world applicability.

•

Popularity rankings. Within only 48 hours of its initial launch, GLM-4.5 ranked first globally on

the trending board of Hugging Face, the world’s largest platform for open-source models.

1 Benchmark tests are structured, standardized evaluations that measure LLMs’ capabilities across a range of tasks. The twelve industry-

standard benchmark tests we used to evaluate GLM-4.5 include three categories: (i) agentic benchmarks, including TAU-Bench, BFCL V3

and BrowseComp. GLM-4.5 achieved a comprehensive score of 58.1 under these agentic benchmarks, compared with scores ranging from

45.0 to 61.1 for industry peer models; (ii) reasoning benchmarks, including MMLU-Pro, AIME 24, MATH-500, SciCode, GPQA, HLE and

LCB (2407-2501). GLM-4.5 achieved a comprehensive score of 68.8 under these reasoning benchmarks, compared with scores ranging

from 63.5 to 74.2 for industry peer models; and (iii) coding benchmarks, including SWE-Bench Verified and Terminal-Bench. GLM-4.5

achieved a comprehensive score of 50.9 under these coding benchmarks, compared with scores ranging from 36.7 to 55.5 for industry peer

models.

– 5 –

SUMMARY

•

Hallucination rate. In September 2025, GLM-4.5 had the world’s second-lowest and China’s

lowest hallucination rate, according to the LLM Hallucination Leaderboard for Retrieval-

Augmented Generation (RAG). This benchmark evaluates large models based on how frequently

they produce non-existent answers (i.e., hallucinations) in response to intentionally misleading

questions.

In September 2025, we released GLM-4.6, a further updated version of our foundational model which

primarily features enhanced coding capabilities. In November 2025, GLM-4.6 ranked first globally on

CodeArena, the latest industry-recognized global evaluation platform designed to assess models’ coding

capabilities.

Reflection and Rumination Models

Reflection and rumination models spend additional time “deep thinking” before generating an answer,

which makes them better for complex reasoning tasks. Building upon our foundation model, we built our

reflection model (GLM-Z1) and rumination model (GLM-Z1-Rumination).

GLM-Z1 is a reflection model designed to tackle problems with certainty, aiming for more precise and

accurate solutions. It was developed based on the foundation model through extended reinforcement

learning and further training on tasks including mathematics, coding and logic.

Evolution of Agentic AI

- GLM-Z1-Rumination introduces iterative, deep-thinking capabilities designed to solve open-ended problems through external information gathering.

- The multimodal suite spans image, video, and voice generation, including GLM-Realtime for live video interactions.

- AutoGLM marks a shift from conversational AI to 'acting' AI, capable of autonomously controlling digital devices via graphical user interfaces.

- AutoGLM 2.0 operates on the cloud, allowing the AI to complete tasks across mobile apps and websites without interrupting the user's local device usage.

- The company leverages its position as the first in China to develop 100-billion-parameter models to build a comprehensive Model-as-a-Service (MaaS) platform.

- Strategic focus remains on scaling general-purpose R&D and fostering a vibrant open-source ecosystem to drive commercialization.

AutoGLM represents a major step forward in the evolution of our AI universe—from “chat” to “act,” bridging the gap between conversation-based AI and real-world task execution.

GLM-Z1-Rumination is designed to address problems with uncertainty, especially open-ended,

exploratory questions that require gathering and processing external information iteratively. Compared with

GLM-Z1, GLM-Z1-Rumination is capable of deeper and longer thinking and using tools to solve more

open-ended and complex problems.

Multimodal Models

Multimodal models are capable of processing and integrating information from various modalities,

such as text, images, audio and video. We have developed various multimodal models serving different

functionalities, such as CogView (image generation), GLM-4.5V (visual comprehension and reasoning),

CogVideoX (video generation), GLM-Realtime (realtime video call) and GLM-4-Voice (voice model).

AI Agents

AI agents combine reasoning, planning and tool-use capabilities, and can autonomously perform multi-

step tasks without constant human input.

Our foundation agent model is AutoGLM. AutoGLM represents a major step forward in the evolution

of our AI universe—from “chat” to “act,” bridging the gap between conversation-based AI and real-world

task execution. Designed as a foundation agent tailored for autonomous control of digital devices through

graphical user interfaces (GUIs), AutoGLM transforms human-like reasoning into concrete actions.

AutoGLM achieved SOTA performance under AgentBench, an agentic AI benchmark recognized by the

2024 AI Index published by Stanford University.

In August 2025, we released an updated version of AutoGLM (also known as “AutoGLM 2.0”), which

is powered by our then latest foundation model GLM-4.5 and visual comprehension and reasoning model

GLM-4.5V. This updated version enables AutoGLM to simulate human actions across a broader range of

mobile applications and websites. It can autonomously complete requested tasks on the cloud without

occupying the user’s mobile phone or computer, allowing users to continue using their own devices without

interruption.

– 6 –

SUMMARY

AutoGLM Rumination is an advanced version of AutoGLM. It is an autonomous AI agent designed to

explore open-ended questions and take action based on its findings. AutoGLM Rumination features

“thinking

while

working”—it

leverages

outstanding

reasoning

capabilities

powered

by

the

GLM-Z1-Rumination

model

while

incorporating

AutoGLM’s

interactive

operational

capabilities.

AutoGLM Rumination can handle complex tasks involving deep reasoning, iterative research and producing

actionable outcomes.

We have also developed CoCo, a sophisticated enterprise AI agent designed to deliver intelligent

automation across corporate environments.

Coding Models

CodeGeeX is a powerful coding model designed to enhance programming efficiency and streamline

workflows. It enables developers to automatically generate code based on natural language descriptions or

complete unfinished lines or blocks of code, significantly improving productivity.

As of the Latest Practicable Date, the select models and agents set forth above had been

commercialized.

OUR STRENGTHS

•

First AI company in China to have self-developed large models at a scale of over 100 billion

parameters;

•

Comprehensive large model portfolio;

•

Deep academic roots as cornerstone for technological leadership;

•

All-in-one MaaS platform maximizing model commercialization;

•

Vibrant ecosystem fostered by open-source strategy and agentic agenda; and

•

Management and advisory team with extensive research and industry experience.

See “Business—Our Strengths.”

OUR STRATEGIES

•

Strengthen our R&D capabilities in general-purpose large models;

•

Optimize our MaaS platform; and

•

Attract and retain the best minds.

See “Business—Our Strategies.”

SPECIALIST TECHNOLOGY INDUSTRY

AI Sector Compliance and Growth

- The company is officially classified as a Specialist Technology Industry provider under the Artificial Intelligence subcategory of Next-generation Information Technology.

- Their core offerings include multimodal large models capable of processing text, images, audio, and video through billions of parameters.

- Commercial applications span diverse sectors including municipal transportation management, financial services, and large-scale document analysis for internet firms.

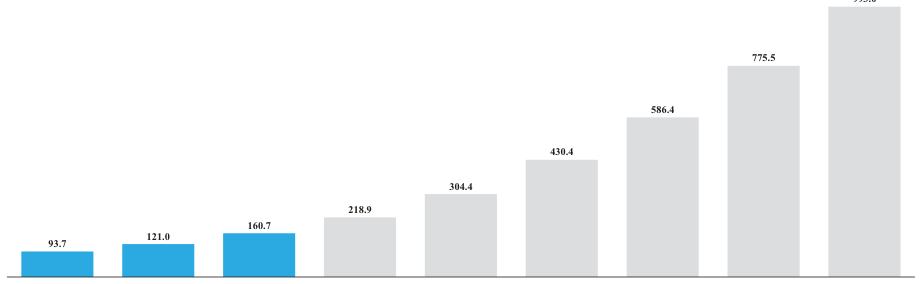

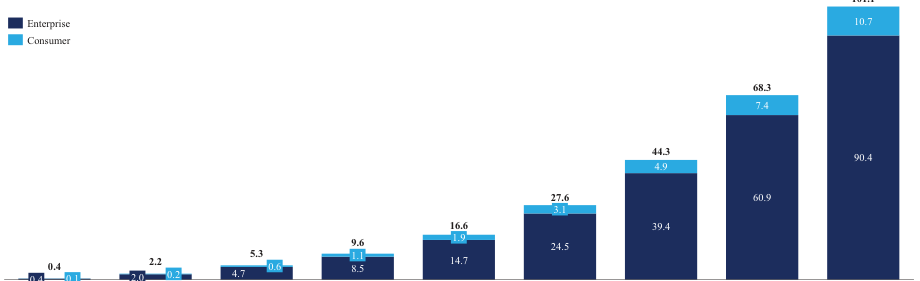

- The China Large Language Model (LLM) market is projected to experience explosive growth, rising from RMB5.3 billion in 2024 to RMB101.1 billion by 2030.

- Institutional and enterprise customers are identified as the primary drivers of this market, expected to maintain a 63.7% compound annual growth rate.

- The regulatory landscape currently requires no specific approvals for the company's specialist technology products as of the latest practicable date.

A large model is a complex set of algorithms that identify and leverage patterns from vast amounts of data by iteratively adjusting billions of parameters to increase accuracy.

Our industry consultant, Frost & Sullivan, confirms and our Directors are of the view that we fall

within an acceptable sector of a Specialist Technology Industry, namely, Artificial Intelligence under Next-

generation Information Technology as defined under Chapter 18C of the Listing Rules.

– 7 –

SUMMARY

The following table sets forth an analysis of how our offerings fall within the acceptable sector:

Specialist

Technology

Products

Acceptable

Sector

Acceptable Sector –

Subcategories

Functions and Applicability Analysis

Each of our models

and agents

See “—Our Models

and Agents” above

Next generation

Information

technology—Artificial

Intelligence

AI-powered

algorithm

programming:

image recognition,

audio-visual

learning, natural

language

processing,

machine learning

and deep learning

A large model is a complex set of

algorithms that identify and leverage

patterns from vast amounts of data by

iteratively

adjusting

billions

of

parameters to increase accuracy. Such

algorithms enable our models to achieve

functions

such

as

image

recognition,

audio-visual learning, natural language

processing, machine learning and deep

learning. For example, our multimodal

models

can

process

and

integrate

information

from

various

modalities,

including text, images, audio and video.

AI solutions:

the design

and provision of

AI solutions used in

different industry

verticals.

Our models constitute the foundation for

AI

solutions

to

a

broad

range

of

industries,

such

as

technology

and

internet, public service and traditional

corporate sectors (e.g., financial services,

manufacturing and energy). For example,

for the technology and internet sector, our

large models help our customers review

documents and analyze operating data on

a massive scale. For the public service

sector, we developed large models for

municipal

public

transportation

management

that

enable

accurate

monitoring of bus traffic flow and real-

time

estimation

of

arrival.

See

“Business—Our Commercial Use Cases”

for more use cases demonstrating the

applications

of

our

AI

solutions

in

different industry verticals.

Based on the following analysis and the view of the Directors and Frost & Sullivan, the Sole Sponsor

is of the view that the models and agents offered by the Group as described in this prospectus fall within an

acceptable sector of a Specialist Technology Industry, namely, Artificial Intelligence under Next Generation

Information Technology as defined under Chapter 18C of the Listing Rules. As of the Latest Practicable

Date, no regulatory approval had been required for our Specialist Technology Products.

INDUSTRY OVERVIEW AND COMPETITIVE LANDSCAPE

As a large model company, we operate in the LLM market, a subset of the AI market. LLM

development has experienced great leaps forward in recent years, especially since 2022. The most cutting-

edge research is currently conducted in the United States and China, with a number of leading players

having emerged in each country.

In terms of revenue, the size of the LLM market in China was RMB5.3 billion in 2024, with

institutional customers contributing RMB4.7 billion and individual customers contributing RMB0.6 billion.

With the continued advancement of LLM technologies and growing demand from both institutional and

– 8 –

SUMMARY

individual consumers, the market is estimated to grow to RMB101.1 billion by 2030, representing a CAGR

of 63.5% from 2024 to 2030. With institutional customers remaining as the main growth driver, the

enterprise LLM market in China is estimated to reach RMB90.4 billion by 2030, representing a CAGR of

63.7% from 2024 to 2030.

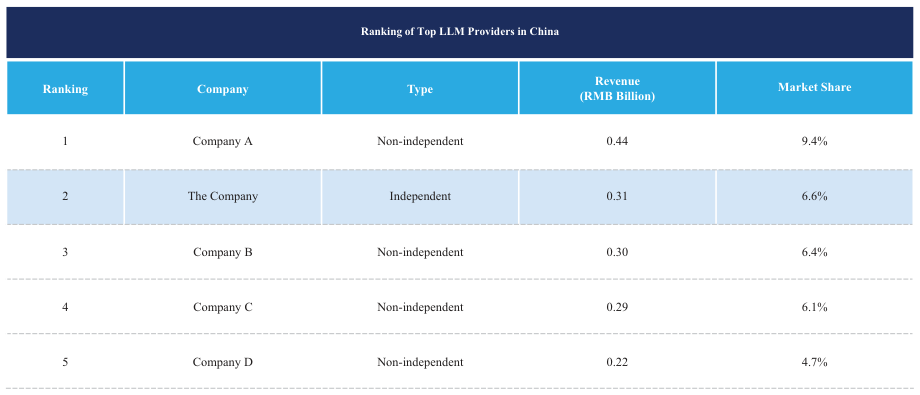

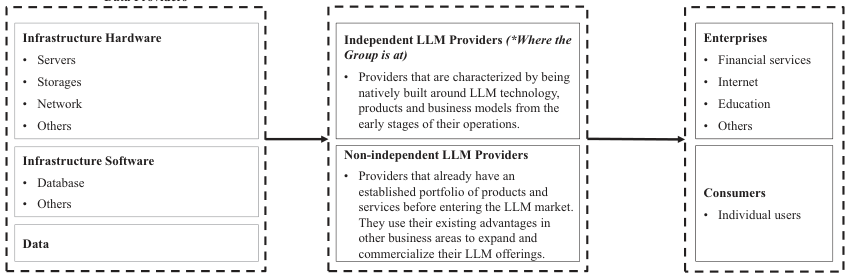

Participants in the LLM market in China can be divided into independent providers and non-

independent providers. Independent providers are characterized by being natively built around LLM

Competitive Dynamics in China's LLM Market

- The Chinese LLM market is divided between 'non-independent' technology giants and 'independent' pure-play providers.

- Tech giants leverage massive existing user bases and diversified business lines to promote their AI products rapidly.

- Enterprise clients often prefer independent providers to avoid direct competition with tech giants or falling into their spheres of influence.

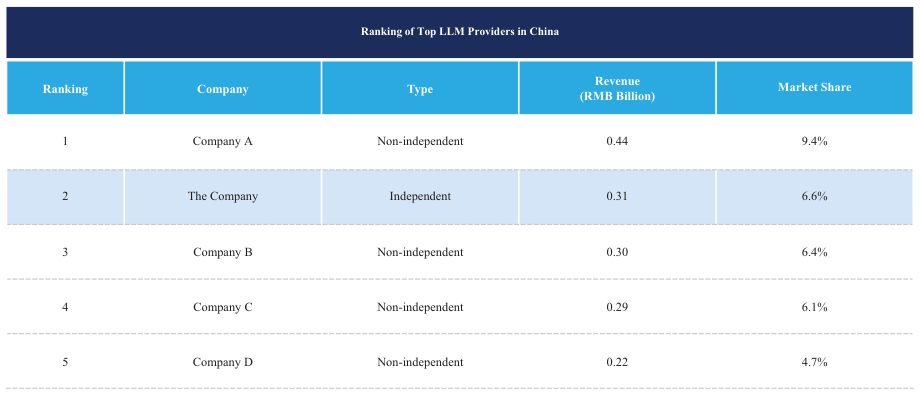

- Market data from 2024 shows a mix of independent and non-independent firms among the top five revenue earners, with the leader holding a 14.9% market share.

- The featured company emphasizes a research-driven culture, employing 657 R&D specialists focused on natural language processing and multimodal analysis.

- Intellectual property protection is a core strategic pillar, evidenced by 86 registered patents and hundreds of pending applications.

Also, enterprise clients in certain industries can be sensitive about falling or appearing to fall into spheres of influence by certain technology giants and are more inclined to adopt AI solutions from “pure-play” providers.

technology, products and business models from the early stages of their operations; and non-independent

providers are typically technology giants that branch into the AI area. Independent providers face very

different competitive dynamics as compared with those of non-independent providers. For example,

leveraging their pre-existing, diversified business lines, non-independent providers have accumulated

massive user bases, which facilitates the promotion of their LLM products. On the other hand, however,

enterprise clients may be disinclined to select an LLM product offered by a technology giant if it operates

business lines that compete directly with the client’s own business. Also, enterprise clients in certain

industries can be sensitive about falling or appearing to fall into spheres of influence by certain technology

giants and are more inclined to adopt AI solutions from “pure-play” providers.

Ranking of Top LLM Providers in China, in terms of revenue (2024)

Ranking of Top LLM Providers in China

e

p

y

T

y

n

a

p

m

o

C

Ranking

Revenue

(RMB Billion)

Market Share

1

%

4.9

4

4.0

tn

e

d

n

e

p

e

d

ni-

n

o

N

A

y

n

a

p

m

o

C

2

%

6.6

1

3.0

tn

e

d

n

e

p

e

d

n

I

y

n

a

p

m

o

C

e

h

T

3

%

4.6

0

3.0

tn

e

d

n

e

p

e

d

ni-

n

o

N

B

y

n

a

p

m

o

C

4

%

1.6

9

2.0

tn

e

d

n

e

p

e

d

ni-

n

o

N

C

y

n

a

p

m

o

C

5

%

7.4

2

2.0

tn

e

d

n

e

p

e

d

ni-

n

o

N

D

y

n

a

p

m

o

C

Notes:

1)

Company A, founded in 1999, is a public company listed on Shenzhen Stock Exchange.

2)

Company B, founded in 1999, is a public company listed on both the Hong Kong Stock Exchange and the New York Stock

Exchange.

3)

Company C, founded in 2014, is a public company listed on the Hong Kong Stock Exchange.

4)

Company D, founded in 2000, is a public company listed on both Hong Kong Stock Exchange and NASDAQ.

Source: Frost & Sullivan

– 9 –

SUMMARY

RESEARCH AND DEVELOPMENT

We are, at the core, a company of data scientists and engineers, with R&D ingrained in every aspect of

what we do. On a daily basis, we are intensely focused on elevating the intelligence of our foundation

models; improving and developing useful and cost-effective AI agents for ever more industry verticals and

other use cases; and collaborate with business partners to design and improve our computing infrastructure

that enables our MaaS platform to deliver comprehensive capabilities. We achieve these through, first and

foremost, our people, as well as our robust technology infrastructure and rigorous R&D processes.

As of June 30, 2025, we had a R&D team of 657 members with background and experience in the

relevant fields such as natural language processing, advanced decision-making in complex systems and

multimodal semantic analysis. See “Business—Research and Development—Talent.”

INTELLECTUAL PROPERTY

Our intellectual property is critical to our innovation which underpins our success. We seek to protect

our intellectual property through a combination of patents, copyrights, trademarks, domain names, trade

secrets, confidentiality agreements and other measures. As of the Latest Practicable Date, we had 86

registered patents in China, among which 84 were invention patents, and 232 patent applications in China.

As of the same date, we had 160 copyrights, 314 trademarks and 59 domain names in China.

We have designed and adopted comprehensive measures to protect our intellectual property. We enter

into employment agreements with confidentiality, non-compete covenants and intellectual property

LLM Market Competition and Growth

- The company secures intellectual property through strict ownership clauses with employees and consultants, reporting no material infringement disputes to date.

- The Large Language Model (LLM) market is characterized by intense competition based on technical capabilities, ecosystem building, and talent acquisition.

- Revenue has demonstrated explosive growth with a CAGR exceeding 130%, rising from RMB57.4 million in 2022 to RMB312.4 million in 2024.

- Significant net losses have occurred alongside revenue growth, primarily driven by massive investments in research and development which reached RMB2,195.4 million in 2024.

- The path to profitability relies on leveraging the expanding Chinese LLM market, iterating AI models, and broadening customer reach to achieve operating leverage.

- Future sustainability is predicated on the belief that revenue growth will eventually outpace the high costs of R&D and infrastructure.

Our losses during the Track Record Period were primarily due to our significant investments in research and development.

ownership clauses with our employees, certain consultants and advisors. They acknowledge that the

intellectual property developed by them in connection with their employment with us, including our in-

house developed content, is our property. During the Track Record Period and up to the Latest Practicable

Date, we had not been subject to any material disputes or claims for infringement of third parties’

trademarks, licenses and other intellectual property rights.

COMPETITION

As a large model company, we operate in what is known as the LLM market, a subset of the AI

market. The LLM market is highly competitive. According to Frost & Sullivan, LLM vendors compete

based on factors including (i) technical capabilities such as self-developed LLM pre-training framework and

model customization and optimization, (ii) flexible business models and delivery strategies, (iii) ecosystem

building capabilities and (iv) talent with deep technical backgrounds and extensive experience. We compete

with both independent and non-independent LLM vendors, both within China and internationally. We may

also in the future face competition from new entrants that will increase the competition. Principal

competitive factors important to us include scope, performance and safety of our service offerings, user

experience, our R&D capabilities and our talents. For additional details regarding the competitive landscape

of the industry in which we operate, see “Industry Overview” and “Business—Competition.”

BUSINESS SUSTAINABILITY

Our Historical Performance

We achieved strong growth in revenue during the Track Record Period. Our revenues grew from

RMB57.4 million in 2022 to RMB124.5 million in 2023 and further to RMB312.4 million in 2024 with a

CAGR of over 130%. Our revenue also grew significantly from RMB44.9 million in the six months ended

June 30, 2024 to RMB190.9 million in June 30, 2025.

While we achieved sustained business growth, we had loss for the year of RMB143.7 million,

RMB788.0 million, RMB2,958.0 million, RMB1,235.6 million and RMB2,357.9 million in 2022, 2023,

– 10 –

SUMMARY

2024 and the six months ended June 30, 2024 and 2025, respectively. Our losses during the Track Record

Period were primarily due to our significant investments in research and development. Our R&D expenses

increased from RMB84.4 million in 2022 to RMB528.9 million in 2023 and further to RMB2,195.4 million

in 2024. Our R&D expenses increased by 85.6% from RMB859.2 million in the six months ended June 30,

2024 to RMB1,594.7 million in June 30, 2025.

Path to Profitability

While the absolute amount of our net losses increased during the Track Record Period, we expect to

turn around our net loss position through increase in revenue and enhancement in operating efficiency.

Continuous Revenue Growth

Revenue growth is key to achieving profitability. We have built a robust portfolio of AI models and

agents to empower a broad range of industries and address unique challenges and optimize workflows in

each industry. Leveraging the significant market potential of the LLM market, as well as our technological

leadership, we are well positioned to upgrade our AI models and agents in response to emerging market

opportunities and continue to achieve revenue growth. The growth in our revenue will gradually cover the

relevant costs and expenses and thereby reduce our net losses in general. We plan to increase our revenue

by (i) leveraging the growth potential of the LLM market in China; (ii) continuously promote iteration and

upgrade of AI models and agents; (iii) broadening our customer reach; and (iv) expanding our solutions use

for new industry sectors.

Improving Operating Leverage

Operational Efficiency and Stakeholder Dynamics

- The company is prioritizing profitability through optimized R&D efficiency and the iteration of its foundation models via its MaaS platform.

- Operational management strategies include simplifying workflows, controlling administrative expenses, and adopting data-driven marketing approaches.

- Customer concentration is high but declining, with the top five customers accounting for 40.0% of revenue in mid-2025 compared to 61.5% in 2023.

- The supply chain relies heavily on providers of computing hardware, data cleansing services, and large model evaluation support.

- A group of controlling shareholders, including several doctors and investment entities, maintains a collective interest of approximately 33.03%.

- The company asserts its business model is sustainable based on historical growth and strategic cloud-based deployment.

With our deep academic roots as cornerstone for technological leadership, we are constantly making technological advancements and iterations of our foundation models, boosting our profitability.

Improvement of our operating efficiency is also a significant factor to achieve profitability. We plan to

optimize R&D efficiency and improve operational management effectiveness. Since our inception, we have

invested significantly in R&D and our MaaS platform. With our deep academic roots as cornerstone for

technological leadership, we are constantly making technological advancements and iterations of our

foundation models, boosting our profitability. We have also adopted measures to control general and

administration expenses and improving operational efficiency. We have simplified workflows and

optimized resource allocation to ensuring that operational needs are met in a cost-effective manner. In

addition, we have adopted a focused approach to selling and marketing activities to further improve the

efficiency of related expenses. By directing resources and efforts toward cloud-based deployment and