Read Write Own

Overview unavailable.

Building the Next Internet Era

- Chris Dixon's book 'Read Write Own' outlines a vision for the internet's next phase, centered on digital ownership and blockchain technology.

- The work traces the evolution of digital infrastructure from open protocol networks to the current dominance of centralized corporate networks.

- A central theme is the 'Attract-Extract Cycle,' which describes how corporate platforms eventually exploit the users and creators they initially courted.

- The author explores how tokens and blockchains can facilitate community-governed software, treating code like 'Lego bricks' through composability.

- The text argues that the most significant technological breakthroughs often start by appearing confusing, incomplete, or like mere toys to observers.

For any speculation which does not at first glance look crazy, there is no hope.

The Internet's Centralization Crisis

- The early internet was an open, permissionless platform where creators owned their work and operated under democratic governance.

- Starting in the mid-2000s, a small group of megacorporations gained control, with the top 1 percent of sites now dominating the vast majority of web traffic.

- The internet has transitioned from a decentralized network of equals to a permissioned system controlled by a handful of tech giants.

- Centralization has created negative externalities, including widespread user surveillance and an adversarial relationship between platforms and their users.

- Creators and startups now face significant risks because they depend on centralized platforms that can unilaterally change rules and seize audiences.

The network went from permissionless to permissioned.

The Tyranny of Gatekeepers

- Big Tech companies utilize widespread user surveillance and opaque privacy policies to exploit personal data for profit.

- Centralized platforms control public discourse and business success through non-transparent practices like deplatforming and shadowbanning.

- The current internet landscape forces startups and creators into a system of permission-seeking that incumbents use to thwart competition.

- Major social networks maintain nearly 100 percent take rates, extracting almost all revenue generated by the users and creators who provide the actual value.

- While networks are the primary engine of the internet, their private ownership concentrates power and wealth in the hands of a few corporate entities.

In business, permission becomes a pretense for tyranny.

The Big Tech Tax

- Big Tech corporations extract immense wealth by maintaining high take rates, often capturing nearly all the value created by independent users and creators.

- The mobile landscape is dominated by an Apple and Google duopoly that charges payment fees ten times higher than the industry standard.

- Social networks have historically crushed third-party developers by cutting off platform access, creating a quicksand environment that stifles startup innovation.

- Companies like Amazon and Google leverage their roles as essential infrastructure to unfairly promote their own products and undercut smaller competitors.

- This consolidation of power allows platforms to act as capricious gatekeepers, using restrictive policies to maintain dominance and eliminate consumer choice.

Developers know better than to lay foundations on quicksand.

Reclaiming the Centralized Internet

- Major tech platforms like Amazon and Apple utilize their market dominance to stifle competitors through high fees and exclusionary practices.

- The centralization of power is fundamentally transforming the internet from a decentralized network into a closed system that discourages innovation.

- Traditional government regulation may inadvertently strengthen incumbents by creating barriers to entry that smaller startups cannot afford to navigate.

- The software-based nature of the internet allows for it to be reshaped through new code, which acts as an encoding of human thought capable of rapid change.

Big Tech platforms have more than just a home field advantage. They get to rewrite the rules of the entire game for their sole benefit.

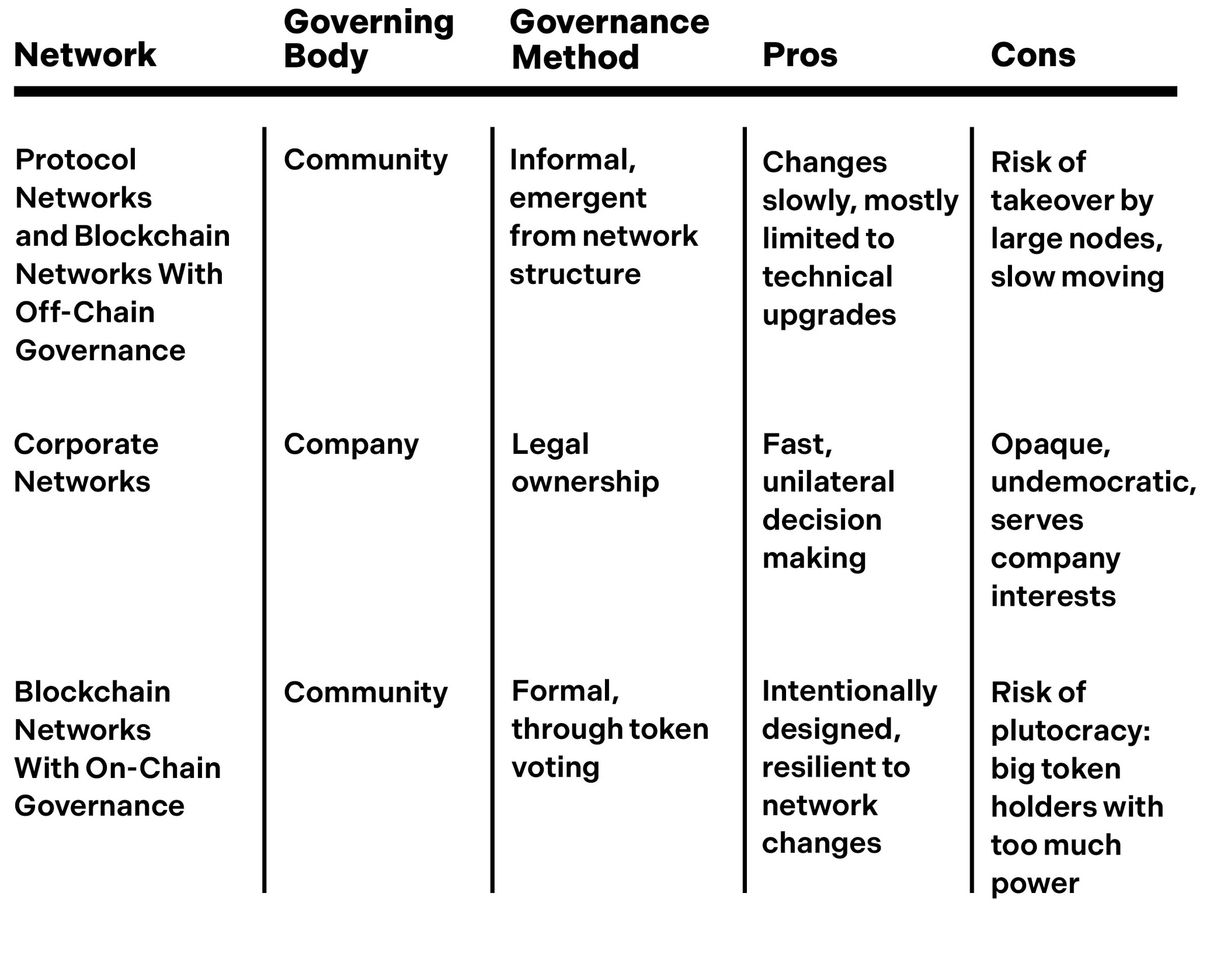

Evolution of Digital Networks

- Software is a uniquely expressive medium for human thought, functioning more like an art form than traditional engineering.

- The distribution of power and money on the internet is fundamentally determined by the architecture and design of its networks.

- Protocol networks represent open, democratic systems where control remains at the edges with the users and developers.

- Corporate networks operate as centralized 'walled gardens' where profits and power flow inward to the companies that own them.

- The history of the internet is divided into distinct eras: the 'read era' of open information and the 'read-write era' of corporate-led publishing.

Software is the encoding of human thought, just like writing or painting or cave drawings.

The Era of Digital Ownership

- The internet has evolved through three distinct architectures: the information-focused 'read' era, the publishing-driven 'read-write' era, and the emerging 'read-write-own' era.

- The current shift toward web3 and blockchains aims to democratize ownership, allowing users to become stakeholders with economic and governance power.

- Unlike traditional computers where hardware owners control the software, blockchains allow software to govern a network of hardware devices through inviolable rules.

- This inversion of power enables networks to make strong, software-enforced commitments to their users, counteracting the consolidation of Big Tech.

- Blockchain networks facilitate marketplaces and social connections with lower costs and increased user empowerment compared to corporate-controlled platforms.

Blockchains invert the hardware-software power relationship, like the internet before them.

The Casino and the Computer

- Blockchains enable strong behavioral commitments, creating networks that prioritize user empowerment over corporate interests and reduce transaction fees.

- The author likens blockchains to steel, arguing they provide a superior structural material for building more resilient and ambitious digital public works.

- A cultural divide exists between the 'casino,' focused on speculation and scandals, and the 'computer,' focused on building long-term internet infrastructure.

- While speculators dominate media headlines, the 'computer' group uses blockchain's financial mechanisms as a means to align incentives for genuine innovation.

- Meaningful technological progress in the blockchain space requires patience, often necessitating a decade-long horizon for development and value creation.

Asking “What problems do blockchains solve?” is like asking “What problems does steel solve over, say, wood?”

Computers Versus Casinos

- The author distinguishes between 'computer culture,' which focuses on long-term innovation and decade-long development cycles, and 'casino culture,' which prioritizes short-term speculation.

- True innovation in the software movement requires time to generate financial returns, often necessitating the long hold periods found in venture capital funds.

- Technology is fundamentally neutral; much like a hammer or nitrogen-based fertilizer, blockchains can be used to either build productive systems or fuel destructive speculation.

- The author aims to show how blockchain networks can empower users and revive the potential of open-source protocols that previously lost out to corporate-owned rivals.

- The book provides a roadmap for the internet's future by analyzing its history and the technical mechanisms that allow blockchains to solve urgent digital problems.

So, it’s the computer versus the casino battling it out to define the narrative for this software movement.

Network Design Is Destiny

- Blockchain networks serve as a critical tool for counterbalancing the consolidation of power by major internet corporations.

- The shift in global software development and the rise of AI threaten to accelerate the dominance of well-capitalized tech giants.

- The architecture of a network fundamentally dictates how wealth and power accumulate, effectively acting as an organizing framework for society.

- The distinction between digital 'bits' and physical 'atoms' is increasingly irrelevant because digital networks now shape every aspect of physical reality.

- The current transition in internet technology offers a rare opportunity for developers and users to reimagine and rebuild digital history.

This is a chance to create the internet you want, not the internet you inherited.

Fusion of Worlds

- Digital networks are often dismissed as frivolous, yet they profoundly influence physical realities including global politics, pandemics, and the worldview of individuals.

- Automation typically manifests as the transmutation of physical objects into digital networks, such as travel websites absorbing the tasks of human agents.

- The linguistic use of prefixes like 'e-' diminishes the perceived value of digital activities that have effectively become the new standard for commerce and communication.

- Unlike the industrial economy's focus on production costs, the internet economy derives power from network effects where value increases with every new connection.

- Future technologies like AI and the Internet of Things will further fuse the physical and digital by embedding sensors and actuators into everyday environments.

We wanted flying cars, instead we got Zoom.

The Logic of Networks

- Unlike industrial-age widgets, digital power is built through network effects where value increases with every new connection point.

- Mathematical models like Reed’s law suggest that social network value can scale exponentially, creating values far beyond traditional economic logic.

- Large tech companies guard their network advantages by making it costly for users to leave, which centralizes power and stifles innovation.

- Solving the problem of digital monopolies requires moving beyond mere regulation toward building new networks that are structurally resistant to centralization.

Network effects take small advantages and snowball them into avalanches.

The Evolution of Protocol Networks

- The author advocates for building decentralized networks that prevent power concentration by design rather than relying on corporate-led startups.

- The early internet, specifically ARPANET, was shaped by an academic culture that valued open access, meritocracy, and user-led governance.

- Permissionless protocols are compared to natural languages because they require broad consensus to function and allow diverse participants to communicate.

- Early digital pioneers envisioned cyberspace as a radically open environment that could transcend physical-world prejudices like race and economic status.

- Unlike centralized platforms, original web protocols like HTTP and HTML created a decentralized 'space' for information without a singular controlling organization.

We are creating a world that all may enter without privilege or prejudice accorded by race, economic power, military force, or station of birth.

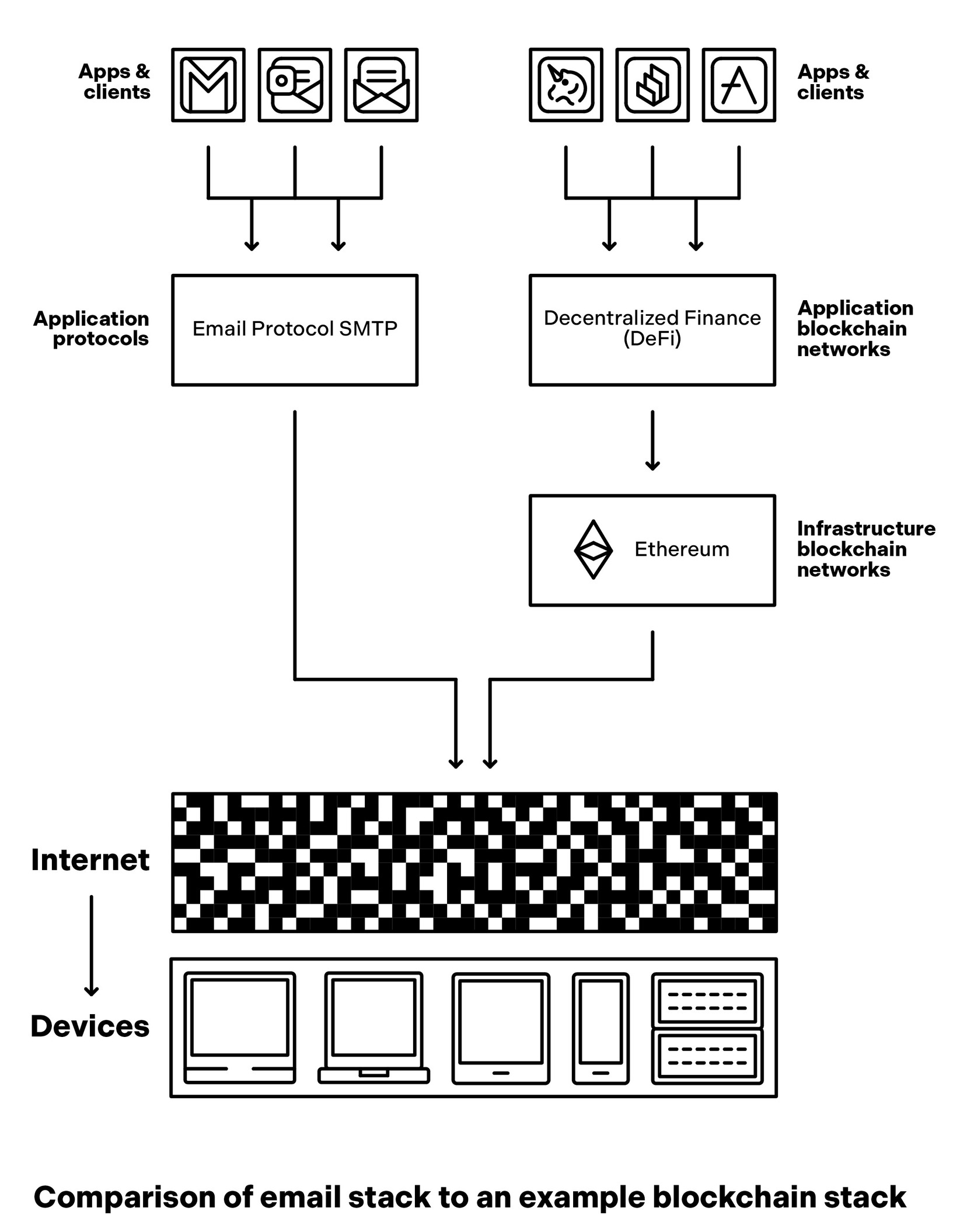

The Internet Protocol Stack

- The internet functions through a layered stack of protocols that require consensus to operate, much like the evolution of human languages.

- The networking layer, defined by Internet Protocol (IP) in 1983, enables hardware devices to communicate by formatting and routing data packets.

- The application layer allows user interaction through protocols like SMTP for email and HTTP for the web, which succeeded due to their open and simple designs.

- Users access these protocol networks through clients or portals, such as web browsers, which act as the interface for participating in the underlying network.

- The internet's core architecture was designed to be decentralized and resilient, allowing the system to function even if nodes are destroyed during a catastrophe.

Just as the LP was invented for connoisseurs and audiophiles but spawned an entire industry , electronic mail grew first among the elite community of computer scientists on the ARPANET , then later bloomed like plankton across the Internet.

The History of Internet Naming

- While the internet's architecture is decentralized for resilience, its naming system functions as a centralized 'source of truth' to map human-friendly labels to IP addresses.

- Before DNS, the entire network relied on a single file called HOSTS.TXT, which had to be manually updated and redistributed every time a new node joined the network.

- Paul Mockapetris created the Domain Name System in 1983 to solve the scaling issues of manual recordkeeping by creating a hierarchical, distributed naming system.

- Early DNS governance was overseen by Jon Postel, who was famously described as the 'god' of the internet before control transitioned to the nonprofit ICANN.

- Modern DNS lookups involve a complex chain of resolvers and root servers that translate domain names into numerical addresses in a fraction of a second.

If the Net does have a god, he is probably Jon Postel.

The Power of Digital Names

- The Domain Name System (DNS) allows users to own their identities and control the mapping to IP addresses, creating a system of digital property rights.

- This architecture provides mobility, enabling users to switch service providers without losing their network connections or breaking inbound web links.

- Centralized networks like Twitter and Facebook maintain control by owning user handles, which allows them to gatekeep relationships and manipulate visibility.

- The design of DNS forces businesses to remain competitive and honest, as they cannot rely on network effects to lock in their customers.

- Corporate 'data download' features are often hollow because they return raw data but strip away the social connections that give that data value.

Your only choice is to stay, or leave and start from scratch somewhere else.

Digital Ownership and Networks

- Centralized social networks trap users by controlling identity mappings, making data download features mere gestures rather than true portability.

- Unlike open web protocols, corporate platforms operate as separate networks that discard the principles of democratic governance and permissionless innovation.

- The Domain Name System (DNS) grants users digital property rights, creating an ownership model that has fostered decades of infrastructure investment.

- To remain universal, core network protocols stay unopinionated about content, leaving moderation to be handled by services at the network edges.

- While digital ownership can trigger speculative markets, its primary value lies in giving users control over their names and connections.

These “data download” features are feints. They gesture toward openness and freedom, but they do nothing to increase user choices.

The Power of Protocols

- Protocol networks grant users ownership of their identities and connections, fostering a user-centric digital environment.

- Network effects in protocols benefit the collective community rather than being captured by a single corporate entity.

- The absence of "take rates" and central intermediaries provides strong assurances for developers to invest time and capital.

- Open protocol systems function like highway infrastructure, where predictable accessibility stimulates private investment and growth.

- Corporate platforms currently capture trillions in value that would be distributed to creators if the systems were built on protocols.

The difference between a protocol network like email and a corporate network like Twitter is that email’ s network effect accrues to a community instead of a company .

The Power of Protocols

- Corporate networks centralize trillions in market value that would be distributed to creators and developers if these platforms were open protocols.

- The resurgence of email newsletters demonstrates the value of protocol-based networks where creators own their audience relationships and can switch services without losing subscribers.

- Centralized platforms like Facebook have historically stifled competition by revoking API access, as evidenced by Mark Zuckerberg's personal decision to cripple the video app Vine.

- Open protocols incentivize external innovation and venture capital to solve systemic issues like spam and search, whereas corporate networks must rely solely on internal resources.

- Permissionless innovation allows entrepreneurs to build essential tools and security software without seeking approval from a central gatekeeper or platform owner.

“Yup, go for it,” he told another exec. The move crippled Vine’s growth, and Twitter discontinued the service in 2017 after years of neglect.

Protocols vs. Corporate Platforms

- Protocol networks allow developers to build and capture value without seeking permission from a central authority.

- Corporate networks are historically shunned by founders and venture capitalists because they are susceptible to sudden rule changes and rent extraction.

- Early protocols like email and the web succeeded by growing in a collaborative environment before the rise of massive centralized competitors.

- RSS, once a strong decentralized competitor to social media, was eventually overtaken by Twitter’s centralized but feature-rich model.

- A system is only genuinely open if users can participate without involving a specific, central governing institution.

No higher power could take away what we made.

The Decline of Open Protocols

- Twitter transitioned from an open network participant to the internet's first core service controlled by a single for-profit gatekeeper.

- The decline of the RSS protocol was marked by corporate moves like the shutdown of Google Reader and Twitter's removal of RSS support.

- RSS failed to compete because it lacked a centralized database to facilitate user-friendly features like content discovery and analytics.

- The technical complexity of managing domains and servers created a high barrier to entry for RSS compared to streamlined corporate services.

- Early decentralized social networks failed because they lacked a mechanism to link users and define relationships without a central authority.

At some point Twitter will need to make lots of money to justify their valuation.

Protocol Funding vs. Corporate Capital

- Early open-source social networks failed to scale because they lacked a decentralized database capable of mapping complex human relationships.

- Corporate platforms dominated the market by leveraging massive venture capital to hire developers and subsidize hosting while open protocols relied on donations.

- Non-profit efforts to create neutral social graphs struggled with coordination challenges that for-profit companies could simply bypass.

- The Heartbleed vulnerability exposed the dangers of the internet's reliance on critical open-source software maintained by a handful of underfunded volunteers.

- Technology monopolies selectively fund open-source projects like Linux that serve their interests but avoid supporting protocols that encourage competition.

RSS was just a loosely connected group of developers with no access to capital beyond voluntary donations. It was never a fair fight.

Skeuomorphic and Native Technologies

- Corporations avoid funding new protocol networks because their primary business strategy is to capture and monopolize user bases.

- Early protocol networks like email and the web succeeded because they were established before corporate alternatives became dominant.

- Skeuomorphism involves designing digital tools to mimic familiar physical objects, helping people transition more easily to new technologies.

- The most significant impacts of a new medium are realized when it moves beyond imitation to enable entirely new forms of human interaction.

When Johannes Gutenberg, inventor of the movable-type printing press, published his namesake Bible in the fifteenth century, he made it look like a handmade manuscript copy.

The Internet's Native Renaissance

- Early digital design relied on skeuomorphism, using familiar physical metaphors like trash cans and bookshelves to help users adapt to new computer interfaces.

- The 1990s internet, known as the 'read era,' functioned primarily as a one-way publishing system consisting of digital brochures and catalogs.

- Following the dot-com bubble burst in 2000, mainstream consensus was skeptical of the internet's future, with many users questioning the need for high-speed broadband.

- A shift toward 'internet-native' design in the mid-2000s introduced dynamic, interoperable services like blogging and social networking.

- The transition to a two-way system empowered ordinary people to write to and publish on the web as easily as they could read it.

Most people logged on via dial-up modems—slow landline connections that plunked and plodded along at speeds people today would regard as excruciating.

The Read-Write Era

- Web 2.0 transformed the internet from a passive, read-only medium into a two-way system where ordinary users could publish content as easily as they consumed it.

- The era marked a shift toward corporate network models, where a central authority maintains complete control over services, access, and financial flows.

- Unlike open protocols, centralized corporate networks allowed developers to iterate quickly and secure venture capital by promising the ownership of a network.

- Early successes like eBay demonstrated that network-effect businesses were often more profitable and scalable than inventory-based models like Amazon's initial structure.

- The rise of YouTube illustrated the victory of social video networks over open protocols, enabling anyone with an internet connection to broadcast to the world.

Users, software developers, and other participants are pushed to the network’s edges, where they are subject to the central corporation’s whims.

The Hook and the Network

- Early video startups evolved from supporting existing media providers to building centralized social video platforms like YouTube.

- The 'come for the tool, stay for the network' strategy attracts users with a free utility before transitioning them into a platform-specific network.

- YouTube and Instagram both used free, high-quality tools to solve expensive problems for creators, eventually making cross-platform sharing obsolete.

- Corporate networks have a significant advantage over open protocols because they can subsidize massive infrastructure costs in exchange for eventual network ownership.

- Google's acquisition of YouTube provided the necessary financial war chest and legal protection to transform a costly tool into a massive economic asset.

The treasuries of donation-based projects pale in comparison to the war chests of Big Tech giants.

The Corporate Frenemy Cycle

- Protocol networks struggle to compete with corporate giants because they lack the massive financial subsidies and war chests required to host and scale global services.

- While traditional competitors offer substitute products, corporate platforms and their content creators act as complements that reinforce each other's value.

- Complements exist in a state of constant tension, often engaging in zero-sum battles to capture the largest portion of a customer's total spending.

- Network effects create a paradox where platforms need third-party developers to grow but eventually feel compelled to stifle them to reclaim revenue.

- The history of Big Tech, such as Microsoft in the 1990s, illustrates how platforms strategically move against their own most successful partners.

Indeed, some of the most ferocious competition in business occurs between bedfellows.

Corporate Platform Extraction

- Platform owners prioritize a fragmented ecosystem of complements to maximize their own value and minimize the bargaining power of third parties.

- Microsoft established a precedent for this by bundling free native apps to undermine successful third-party developers on the Windows operating system.

- Social networks frequently use a 'bait and switch' strategy by decreasing organic reach once creators have become economically dependent on the platform.

- This tactic forces creators and advertisers to purchase sponsored content to reach the audiences they previously built for free.

- The trend of squeezing complements is a logical outcome of profit optimization that ensures the survival of the platform owner.

The tension between these goals almost always causes the relationship between corporate networks and their complements to snap.

The Death of Open Networks

- Social networks prioritize profit optimization, leading them to extract value from the creators and advertisers who were initially encouraged to join.

- Platforms frequently use a bait and switch tactic, inviting third-party developers to build apps and then later cutting them off or acquiring them to eliminate competition.

- The transition from open to closed ecosystems began in earnest around 2010 as major players like Facebook and Google engaged in what was termed data protectionism.

- The author shares a personal lesson from his startup, Hunch, which had to be sold partly because the open data it relied on from Twitter was becoming unavailable.

- The predatory behavior of platforms is compared to the Greek Titan Cronos, who consumed his own children to prevent them from eventually challenging his power.

Twitter was acting, Stone added, like “the mythological Greek Titan Cronos, [who] began eating each of his children as they were born.”

The Trap of Platform Risk

- Corporate networks transitioned from open interoperability to 'data protectionism,' trapping user data to prevent competition and protect their social graphs.

- The concept of 'platform risk' emerged as a deterrent for developers and investors, as platforms began to limit or cannibalize the third-party apps built on their foundations.

- Closed networks struggle to solve systemic issues like spam because they lack the external 'cavalry' of innovators who historically supported open protocols like email.

- The life cycle of a corporate network follows an S-curve, moving from a friendly recruitment phase to a hostile, zero-sum relationship with its own developers as growth slows.

- Using Metcalfe's Law, the text illustrates why dominant networks eventually refuse to interoperate, as the relative value gain decreases as they grow larger.

Building on a corporate network was like building on a broken foundation.

The Attract-Extract Cycle

- Metcalfe's Law illustrates that smaller networks gain significantly more value from interoperating than larger ones, creating a natural disincentive for dominant platforms to cooperate.

- The 'attract-extract cycle' describes a pattern where platforms initially foster cooperation to grow, only to pivot toward competition once they achieve maximum leverage.

- Facebook's severed partnership with Zynga serves as a primary example of a platform dismantling a successful partner to protect its own revenue and prevent potential competition.

- Entrepreneurs and developers are increasingly wary of building on corporate networks because the inherent logic of the model leads to a 'bait-and-switch' strategy.

- In contrast to closed corporate platforms, open protocols like email and the web continue to drive massive innovation because they remain community-owned and predictable.

- The systemic misalignment between a corporate network's interests and its participants ultimately stifles global innovation and results in a poorer user experience.

The moment a platform has maximum leverage is the same moment it makes sense to do an about-face.

The Corporate Network Dilemma

- Corporate networks face a fundamental misalignment where company profit motives eventually degrade the user experience.

- Decisions regarding algorithmic rankings and deplatforming are often managed in black boxes, causing significant user frustration.

- Protocol networks like email offer transparent, democratic governance that puts power and stakeholdership into the hands of the community.

- While corporate platforms provided the features and funding to scale the web to billions, they often trap users in an attract-extract cycle.

- Newer protocol-based architectures struggle to survive because the corporate model has become too effective at colonizing new competition.

Corporate networks colonize and overtake new protocol networks like kudzu.

The Platform-App Loop

- Corporate networks eventually succumb to an attract-extract cycle that prioritizes profit-driven logic over the needs of creators and builders.

- Blockchains represent a new network architecture that automates the center of a business model rather than the workers at the periphery.

- The rapid advancement of computing is fueled by Moore's Law, which allows for exponential increases in hardware power and transistor density.

- Economic growth in technology is driven by a feedback loop where applications make platforms more valuable, leading to further reinvestment in the platform.

- This compounding cycle of improvement applies to both corporate-owned platforms like Windows and community-owned protocols like the web.

Instead of putting the taxi driver out of a job, blockchain puts Uber out of a job and lets the taxi drivers work with the customer directly.

Computing Cycles and Innovation Paths

- The platform-app feedback loop creates growth cycles by alternating investment between infrastructure and applications across both corporate and community platforms.

- Historical data suggests computing cycles occur every ten to fifteen years, driven by Moore's law and the time required for research to mature.

- AI and new hardware devices are current consensus bets for the next cycle, whereas blockchains remain a non-consensus bet dismissed by much of the establishment.

- New technologies emerge either 'inside out' from established institutions with high capital or 'outside in' from independent developer communities.

Together these trends combined to bring us the magical handheld supercomputers that are ubiquitous today yet which most science fiction failed to imagine.

Innovation from the Fringes

- Inside-out technologies are predictable products of institutions that require high capital and formal training.

- Outside-in technologies are hatched on the fringes by hobbyists and are often dismissed as toylike or unserious.

- Because software is an art form, groundbreaking innovations often emerge from unconventional spaces like garages and dorm rooms.

- Hobbies act as a leading indicator of future industries because they represent what smart people choose to build when unconstrained by financial goals.

- Success in outside-in tech frequently involves exponential growth that starts from humble, half-baked beginnings like the early web.

I like to say that what the smartest people do on the weekends is what everyone else will do during the week in ten years.

Blockchains as New Computers

- The interests of hobbyists and engineers often predict future mainstream trends because they work on interesting problems without the constraint of near-term financial goals.

- Technology development oscillates between inside-out movements led by incumbents and outside-in movements driven by hackers and independent developers.

- Blockchains represent a classic outside-in technology, currently ignored or dismissed by major tech companies but championed by the open-source community.

- Satoshi Nakamoto's 2008 paper introduced the blockchain as a way to enable secure transactions through cryptographic proof rather than reliance on a trusted third party.

- Conceptually, a computer is a state machine—an abstraction defined by its ability to store information and its means to modify that information via programs.

I like to say that what the smartest people do on the weekends is what everyone else will do during the week in ten years.

Blockchains as Virtual Computers

- Blockchains are software-based virtual computers that function as state machines layered over a network of physical devices.

- These systems utilize an analogy where nouns represent state or memory and verbs represent the code that manipulates that data.

- Trust is established through mathematical guarantees involving cryptography and game theory rather than a central authority.

- Validators achieve consensus by verifying transaction signatures and randomly selecting a bundle to define the computer's next state.

- The decentralized structure is inherently resilient to manipulation because participants can detect and outvote anyone attempting to cheat.

As you’ll hear me repeat, anything you can dream up, you can code, which is why I compare coding to creative activities like fiction writing.

Blockchains as Global Computers

- Blockchains maintain a single version of history through a consensus process where validators vote on the validity of state transitions.

- While Bitcoin's internal programming is intentionally limited, general-purpose blockchains like Ethereum allow developers to build complex, expressive applications.

- The evolution of blockchain technology is compared to the introduction of the app store, transforming a simple ledger into a permissionless global computer.

- Native digital currencies serve as a critical incentive mechanism, rewarding honest validators for providing the computing power necessary to secure the network.

- The core philosophy of blockchain is to create a permissionless system that bypasses elitist intermediaries and provides equal access to all users.

Blockchains are not databases; they’re full-fledged computers.

Decentralized Trust and Transparency

- Satoshi Nakamoto designed Bitcoin to be permissionless to bypass the elitist gatekeeping inherent in traditional banking systems.

- Proof of work and proof of stake are mechanisms designed to secure open networks against bad actors by imposing either energy costs or financial risk.

- Proof of stake is a more sustainable and efficient evolution of blockchain technology that addresses the environmental concerns associated with high energy consumption.

- The popular perception of blockchain as a tool for anonymity is a misconception; most major networks are entirely public and easily traceable by authorities.

- The extreme transparency of blockchain ledgers could actually prevent mainstream adoption if users feel uncomfortable exposing sensitive personal and financial information.

This inaccuracy is common, for example, in TV and movies that depict criminals using cryptocurrency to secretly transfer money . It’s also dead wrong.

The Mechanics of Blockchain Security

- While often perceived as anonymous, blockchains are innately transparent and can expose sensitive data like salaries and medical bills, which may hinder broader adoption.

- The term 'crypto' refers to the use of public key cryptography for authentication and signing rather than the encryption of data for privacy.

- Public and private key pairs form the security foundation, allowing users to mathematically sign transactions that are nearly impossible to forge.

- A 'trustless' network functions without a central authority by using consensus processes and financial incentives to ensure validators remain honest.

- Blockchain security is bolstered by the high cost of attacks and the ability for participants to 'hard fork' the network to undo malicious actions.

The signature is analogous to signing a check or legal document in the offline world, but it uses math to prevent forgery instead of handwriting.

Blockchain's Inherent Security Model

- Blockchains utilize calibrated economic rewards to create a self-policing system where participants trust decentralized logic over individual honesty.

- Traditional perimeter security models are inherently flawed because they focus on protecting a single "wall" around data, which attackers can easily bypass through a single gap.

- Unlike corporate databases that store vulnerable login credentials, blockchains require signed transactions and have no central point of failure to break into.

- The blockchain approach unbundles security from general business functions, allowing specialized custodians to manage data protection rather than non-expert institutions like hospitals or car dealers.

- True blockchain hacks are exceedingly rare; most reported thefts are actually attacks on third-party institutions or individuals through methods like phishing.

The model is like putting a wall around a fort that’s stocked with gold and then trying to protect only the wall. It doesn’ t work.

The Virtues of Blockchains

- Most alleged blockchain hacks target external institutions or individuals through phishing rather than the underlying network protocols themselves.

- Major networks like Bitcoin and Ethereum act as the world's largest bug bounty programs, having withstood countless attacks due to the prohibitive cost of a 51 percent breach.

- Blockchains provide a democratic and transparent framework that ensures equal access and public auditability for all participants.

- The technology's most critical feature is its ability to make strong commitments, ensuring code executes exactly as designed without human intervention.

- By putting code in charge, blockchains provide a more reliable alternative to traditional corporate computers governed by one-sided Terms of Service agreements.

These blockchains are, in effect, the world’s biggest bug bounty programs.

Blockchains and Hard Commitments

- Unlike traditional systems where companies control the software, blockchains allow the software to be in charge, resisting external manipulation.

- Applications built on top of blockchains inherit security guarantees that allow them to make binding commitments about their future behavior.

- Critics often misinterpret the intentional constraints of blockchain technology as technical weaknesses rather than structural strengths.

- Corporate promises are inherently unreliable because companies can unilaterally change terms of service or shut down products to suit their interests.

- The value of digital currencies like Bitcoin relies on immutable rules that prevent double-spending and ensure scarcity, which no corporation can credibly provide.

It’s hard for people accustomed to free rein to appreciate that computers could improve on a dimension that is designed, in part, to undermine their authority .

Multiplayer Social Technologies

- Corporate commitments are inherently unreliable because businesses prioritize fiduciary duty over service agreements or user promises.

- Blockchains enable social technologies that facilitate coordination and commitments between parties without pre-existing trust relationships.

- The failure of internal corporate blockchains suggests the technology's primary value lies in public, large-scale networks rather than isolated enterprise use.

- New blockchain-based networks promise fairer governance and shared financial upside for sectors like social media, gaming, and creative arts.

- Managing the complexity of internet-scale software requires encapsulation to ensure that logical interdependencies remain manageable for billions of users.

Fiduciary duty trumps other concerns.

Encapsulation and Digital Tokens

- Software complexity is managed through encapsulation, a technique that hides intricate logical dependencies behind user-friendly interfaces like an electrical outlet.

- Encapsulated code functions like Lego bricks, enabling developers to reuse and combine basic components into larger structures without needing to understand every line of code.

- Blockchain tokens are technical abstractions that simplify complex code into units of ownership, making them easy to manipulate and program.

- Tokens allow for the ownership of anything representable in code, ranging from virtual game items and music to physical assets like real estate.

- Unlike traditional digital environments where items are effectively rented, blockchain-based tokens provide genuine control by utilizing permanent technical commitments.

Outlets unlock the electrical grid and give humans superpowers without anyone having to understand what’s happening on either side of the socket.

The Illusion of Digital Ownership

- In traditional games and social networks, digital goods are merely rented because platforms can unilaterally change terms or revoke access.

- Blockchains shift power from corporate entities to immutable code, enabling true ownership through the mechanism of tokens.

- The current 'read-write-own' era of the internet is defined by tokens, building on previous eras centered around websites and posts.

- Tokens function as expansive building blocks, categorized into fungible units for currency and non-fungible units for unique assets.

- A revolutionary aspect of blockchains is their ability to let software directly hold and control money, rather than just referencing external bank ledgers.

Almost invariably, games eventually fade away or shut down, and along with them their virtual goods blink out of existence.

The Nature of Tokens

- Tokens allow software to directly hold and control value, a fundamental shift from traditional financial systems that only manage references to money held in banks.

- While frequently associated with libertarian politics, blockchain technologies are politically neutral software primitives with a wide variety of potential uses.

- Dollar-pegged stablecoins likely reinforce the global supremacy of the U.S. dollar by meeting the strong market demand for internet-native versions of the currency.

- There are multiple models for stablecoins, ranging from fiat-backed tokens like USDC to algorithmic systems like Maker, which vary in their stability and collateral management.

- The industry often prefers the term 'tokens' because it describes the technology's abstract and generalizable nature more accurately than 'coins' or 'cryptocurrency'.

Money that is held and controlled by software is a new idea that didn’ t exist before blockchains.

The Utility of Tokens

- Fungible tokens serve as 'fuel' for blockchain networks, reviving the pay-as-you-go model of mainframe computing from previous decades.

- Non-fungible tokens (NFTs) act as digital deeds for physical assets like real estate or digital assets like music, art, and code.

- The value of an NFT is often derived from a complex mix of scarcity and social signals rather than direct utility or copyright ownership.

- Beyond simple ownership, NFTs provide digital utility through creator royalties, gaming abilities, and token-gated access to exclusive communities.

- Major brands like Nike and Tiffany use NFTs as 'digital twins' that allow physical products to be represented and used within digital environments.

For users, the NFTs act as a digital twin of the physical object, breaking down the barrie r between the on- and offline worlds.

The Shift to Digital Ownership

- NFTs act as digital twins and identifiers, allowing users to carry their assets and social connections across different platforms and applications.

- Digital wallets serve as persistent inventories and primary interfaces for the blockchain, functioning similarly to how web browsers operate for the internet.

- Treasuries and DAOs enable groups to coordinate and programmatically manage assets, acting as 'multiplayer reserves' governed by software rules.

- Blockchain technology flips the script on digital ownership by transferring control from centralized services like Amazon or Apple to individual users.

- Unlike current models where companies can revoke access to digital purchases at will, tokens provide users with true ownership, portability, and resale capabilities.

If token s are like cells, then treasuries are like full-blown organisms.

The Crisis of Digital Ownership

- Most digital purchases, such as e-books and movies, are actually licensed content that companies can revoke at any time, preventing resale or transfer.

- Corporate networks are compared to theme parks where a single owner dictates all policies, contrasting with the agency found in the physical world.

- Ownership is a key driver of innovation, providing the freedom to remix and repurpose assets into new business models without seeking corporate permission.

- Digital ownership fosters persistent identity and asset portability, similar to how individuals carry their clothes and names across different physical locations.

- While digital tokens currently seem like a niche interest for early adopters, they represent a fundamental shift toward widespread digital ownership.

Imagine if the clothes you bought could be worn only in the venue you bought them in.

The Toy Theory of Disruption

- Disruptive technologies often start by serving a small niche of enthusiasts and are dismissed as toys due to their initial limited functionality.

- Incumbents frequently miss major trends because they are incentivized to focus on high-margin customers and legacy products rather than low-end alternatives.

- Clayton Christensen’s theory suggests that technologies become disruptive when they improve exponentially faster than actual user needs, eventually displacing established leaders.

- To distinguish true disruptors from passing fads, one must look for exponential forces like network effects and software composability that create compounding growth.

Time and again, a sling and rock beat a lumbering swordsman.

The Nature of Disruption

- Exponential growth in software stems from compounding forces like network effects and code composability, which allow developers to build on existing work.

- Disruptive technologies are defined by their misalignment with incumbent business models, making them difficult for established leaders to adopt or even recognize.

- Current advancements like AI and VR are classified as sustaining technologies because they reinforce the data and computing advantages of Big Tech giants.

- The historical dismissal of blockchain and tokens by major corporations suggests that these technologies possess the classic hallmarks of a disruptive force.

Incumbents missing disruptive innovation is what makes it disruptive.

The Evolution of Blockchain Networks

- Tokens function as a new computing primitive, offering programmability and composability that enable diverse applications from social networks to virtual economies.

- Skeptics often overlook the power of network effects, much like those who previously dismissed websites and social media posts as insignificant.

- Using urban planning as an analogy, the text argues that healthy digital networks require a balance between public shared spaces and private commercial incentives.

- Blockchain networks serve as a necessary alternative to corporate-owned platforms, aiming to restore community control and the 'read-write-own' era of the internet.

A city owned by a private company would, in contrast, be a soulless simulacrum.

The Promise of Blockchain Networks

- Corporate networks prioritize owner interests over users, often leading to the crowding out of alternatives and restricted opportunities.

- Blockchain networks provide a new alternative by placing immutable software at the core of the network rather than relying on hardware owners.

- Historically, network designs were limited by the fear that nodes could 'turn evil,' necessitating either weak protocols or centralized corporate control.

- The inversion of the hardware-software relationship allows for rich, expressive network designs with built-in consensus and economic incentives.

- These networks span a layered architecture, encompassing both base infrastructure like Ethereum and specific applications like decentralized finance.

Recall that blockchains put software in charge, inverting the traditional relationship between hardware and software.

Scaling the Blockchain Stack

- Blockchain networks are organized into layers, ranging from general-purpose infrastructure like Ethereum to specialized application networks like DeFi protocols.

- Recent improvements in scaling technology have significantly lowered transaction fees and increased throughput, moving blockchains toward internet-scale capabilities.

- Performance metrics have jumped from the 7-15 transactions per second seen in early networks to hundreds of thousands in newer systems like Aptos and Sui.

- Layer two 'rollups' increase processing power by shifting heavy computation off-chain while using advanced cryptography to verify results on the main network.

- A platform-app feedback loop drives investment, where new infrastructure enables new applications that in turn necessitate further infrastructure improvements.

Imagine paying a few dollars every time you want to upload a post or click “like”—it would be impractical.

The Blockchain Goldilocks Zone

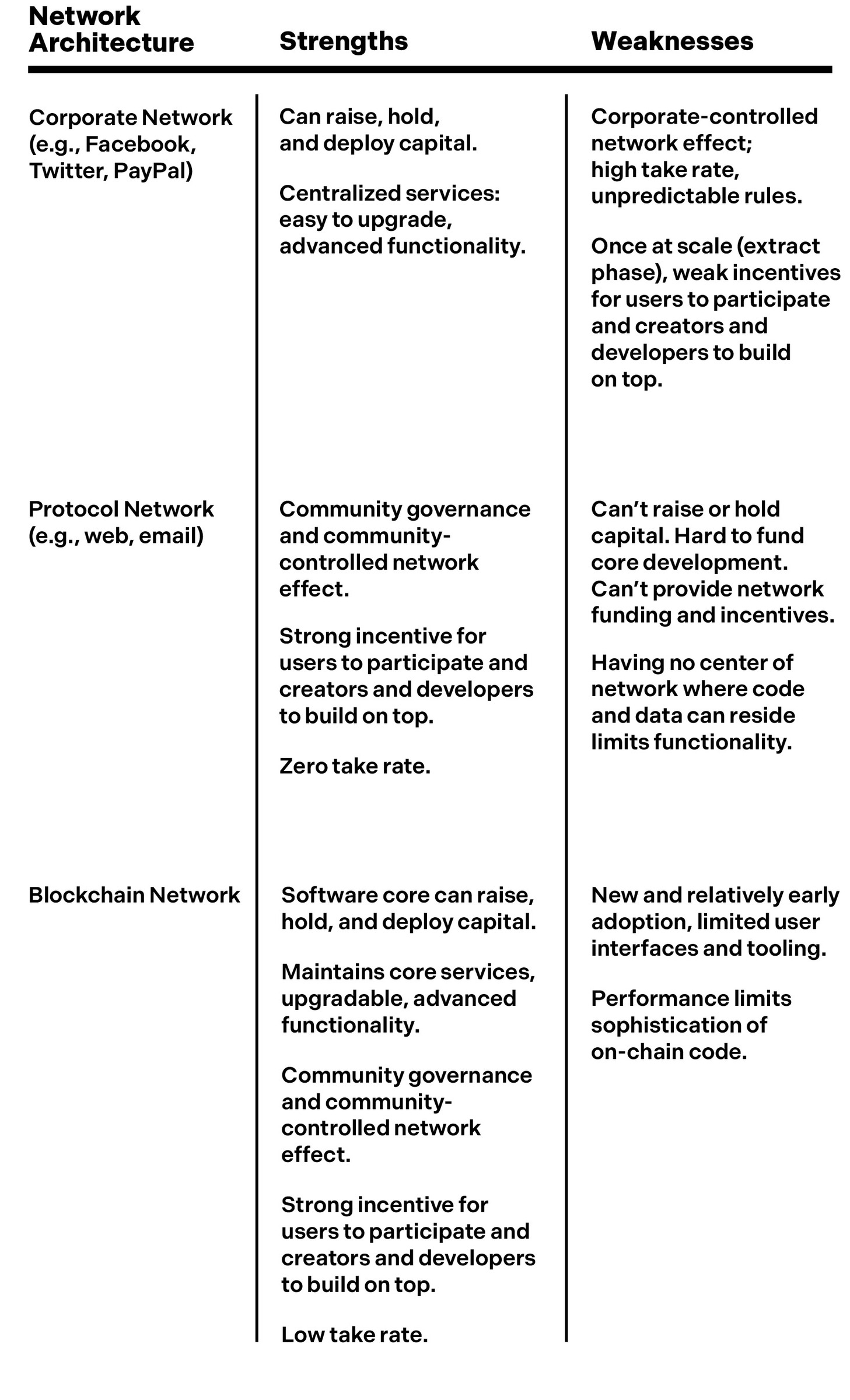

- Maturing infrastructure like rollups is abstracting away complexity, allowing developers to focus on user experience rather than esoteric scaling issues.

- Blockchain networks combine the core service capabilities of corporate models with the community governance and predictability of protocol networks.

- Unlike corporate entities, blockchain networks have hard-capped pricing power, which prevents them from arbitrarily raising take rates and encourages ecosystem growth.

- These networks inhabit a 'Goldilocks zone' where the core system is large enough to support basic services but not so big as to monopolize the network.

- Blockchain architecture achieves a unique balance by being logically centralized through code while remaining organizationally decentralized through its participants.

Blockchain networks inhabit the “Goldilocks zone.” They consist of small core systems surrounded by rich ecosystems of creators, software developers, users, and other participant s.

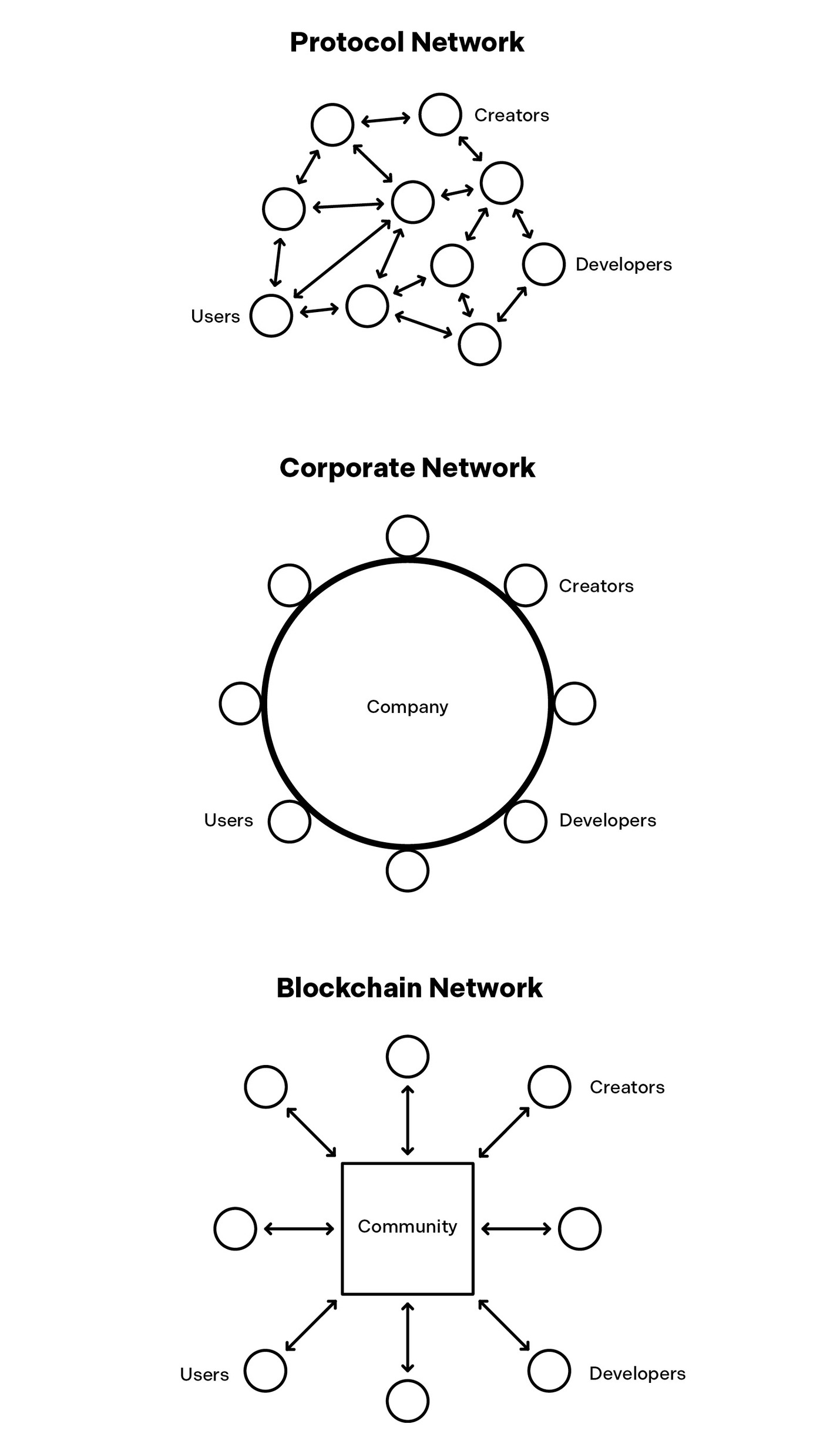

Principles of Blockchain Networks

- Blockchains establish a canonical state through software rules that cannot be overridden by hardware owners or individuals.

- Unlike corporate networks that often trap users in an 'attract-extract' pattern, blockchain networks distribute control among stakeholders like users and creators.

- Most blockchain projects begin with a centralized founding team and transition to community governance through a process called progressive decentralization.

- Effective network design involves keeping the core software minimal while shifting the bulk of development and decision-making to the community.

- DAOs serve as the financial and governing core of these networks, operating through self-executing code and token-based consensus.

Blockchains allow rules to be encoded in software that can be overridden by neither the hardware nor the people who own the hardware.

Blockchain as Digital Cities

- DAOs use on-chain code to self-execute governance decisions and hold funds without relying on external institutions.

- The development of a blockchain is compared to urban planning, where tokens represent land grants that incentivize early residents and developers.

- Property rights and predictable governance are essential for encouraging entrepreneurs to invest their time and money into a digital ecosystem.

- Blockchain networks shift software development from a top-down corporate model to a bottom-up, crowdsourced model similar to Wikipedia.

- This collaborative structure ensures that the interests of the city and its residents are mutually dependent and aligned for growth.

Think Zen. The project belongs to no one and to everyone.

Software's Economic Evolution

- Blockchain networks align incentives to foster inclusive communities where stakeholders collectively guide and share in network value.

- Bill Gates shifted the tech industry's focus from hardware to software by exploiting network effects and platform-application feedback loops.

- The open-source movement challenged corporate dominance by establishing a worldwide community that shares source code in cyberspace.

- The commoditization of software led the tech industry to move up the stack, transitioning into the modern software as a service (SaaS) model.

- The early read-write era of the internet saw a surge in APIs and mash-ups, creating temporary hope for universal interoperability.

Think Zen. The project belongs to no one and to everyone.

The Fall of the Open Web

- During the early Web 2.0 era, the internet was characterized by a spirit of interoperability where developers freely remixed services using APIs.

- The rise of smartphones and the iPhone catalyzed a platform shift that favored corporate networks over open protocol networks.

- Following the attract-extract cycle, dominant platforms eventually prioritized corporate extraction over participant benefits, leading to the closure of open APIs.

- The open web's decline resulted in a concentrated internet where user time is largely spent within a few massive corporate silos like Facebook.

- Interoperability survives primarily in the PC gaming sector, where modding culture allows users to remix games and has even birthed hits like League of Legends.

APIs withered, interoperability fizzled, and the open internet got packed away into silos.

The Art of Software Composition

- Modding has evolved from a niche hobby into a mainstream driver of gaming culture, spawning massive hits like League of Legends and Counter-Strike.

- Open-source software transitioned from a radical 1980s ideology into the foundational technology powering most modern phones and data centers.

- The concept of composability allows software to be built like Lego bricks, enabling developers to assemble complex systems from smaller pieces.

- Platforms like GitHub host a global branching tree of billions of interconnected ideas, facilitating collaboration between millions of strangers.

The collective set of code repositories make up a branching tree of billions of interconnected ideas created by millions of people, most of whom have never met, yet who work collaboratively to advance the global store of knowledge.

Software's Compounding Power

- Platforms like GitHub enable a global collaboration where developers build upon a branching tree of billions of interconnected ideas.

- Composability acts as software's version of compounding interest, where code created once can be reused infinitely to drive exponential productivity.

- This model leverages encapsulation and the wisdom of crowds, allowing developers to integrate complex expertise without needing to understand every underlying detail.

- The advancement of composable services is currently stalled by the lack of sustainable business models and the closed-off nature of corporate networks.

The collective set of code repositories make up a branching tree of billions of interconnected ideas created by millions of people, most of whom have never met, yet who work colla boratively to advance the global store of knowledge.

Reclaiming Software Composability

- Open-source services often struggle to scale because they lack a sustainable business model to fund infrastructure costs like bandwidth and hosting.

- Corporate networks have stifled software innovation by transitioning from open interoperability to restrictive models that prioritize data extraction over developer support.

- While business-to-business APIs like Stripe provide utility, they remain permissioned and closed-source, meaning providers can change rules and fees at will.

- Blockchain networks offer a solution by providing software-encoded assurances that services will remain open, remixable, and autonomous in perpetuity.

- By using tokens to fund global hosting costs, blockchains create a self-sustaining financial model that removes reliance on corporate gatekeepers.

Blockchain networks turn “Don ’t be evil” into “Can’ t be evil.”

Cathedrals, Bazaars, and Margins

- Blockchain architecture shifts the ethical paradigm from "don't be evil" to "can't be evil" by providing immutable guarantees of openness.

- The text contrasts centralized "cathedral" software development with the "bazaar" model, which relies on a self-correcting spontaneous order from a diverse community.

- Blockchain networks allow for massive software reuse and remixes, enabling them to rival the scale and efficiency of large corporate networks.

- Jeff Bezos’s strategy of minimizing margins to seize market share highlights a deflationary business model that blockchains are poised to inherit and evolve.

- By slashing overhead costs like their internet predecessors, blockchains act as a disruptive force against established incumbents with high take rates.

In the first model, popularized by closed-source companies like Microsoft, software is "built like cathedrals, carefully crafted by individual wizards or small bands of mages working in splendid isolation."

The Trap of Take Rates

- Internet disruptors historically succeeded by slashing costs, a strategy blockchains now extend by targeting the high take rates of corporate networks.

- Dominant social networks leverage lock-in from network effects to extract maximum value, often keeping up to 99 percent of advertising revenue.

- Unlike YouTube's revenue-share model, many platforms use fixed 'creator funds' that create a zero-sum environment where platform success reduces individual creator earnings.

- Beyond monetary fees, these networks extract personal data from users and exercise strict control over third-party ecosystems, such as Apple's 30 percent App Store cut.

The web and email are the last free havens on mobile phones.

Dynamics of Network Take Rates

- Apple maintains a high 30 percent take rate by leveraging its captive network, forcing developers to use web-based payment workarounds or pursue legal action.

- Payment networks like Visa and PayPal keep fees low through competition and interchangeable services, often returning value to consumers via incentives.

- Marketplaces for physical goods like eBay and Etsy have moderate take rates because sellers own their inventory, which lowers switching costs compared to digital platforms.

- Protocol networks like email and the web lack a central intermediary, keeping effective take rates low by forcing providers to charge based on infrastructure costs.

- Corporate networks often hide their true take rates by manipulating algorithms to reduce organic reach, effectively forcing participants to purchase advertising to maintain their audience.

The web and email are the last free havens on mobile phones.

Corporate Extraction vs. Blockchain Efficiency

- Corporate networks artificially inflate their take rates by throttling organic reach, forcing creators and sellers to pay for advertisements to reach their own audiences.

- During the 'extract phase,' dominant platforms like Google and Amazon prioritize sponsored content and their own products over the organic links that built their initial utility.

- High gross margins in Big Tech companies often result in bloated bureaucracies and wasteful spending rather than being reinvested into the network participants.

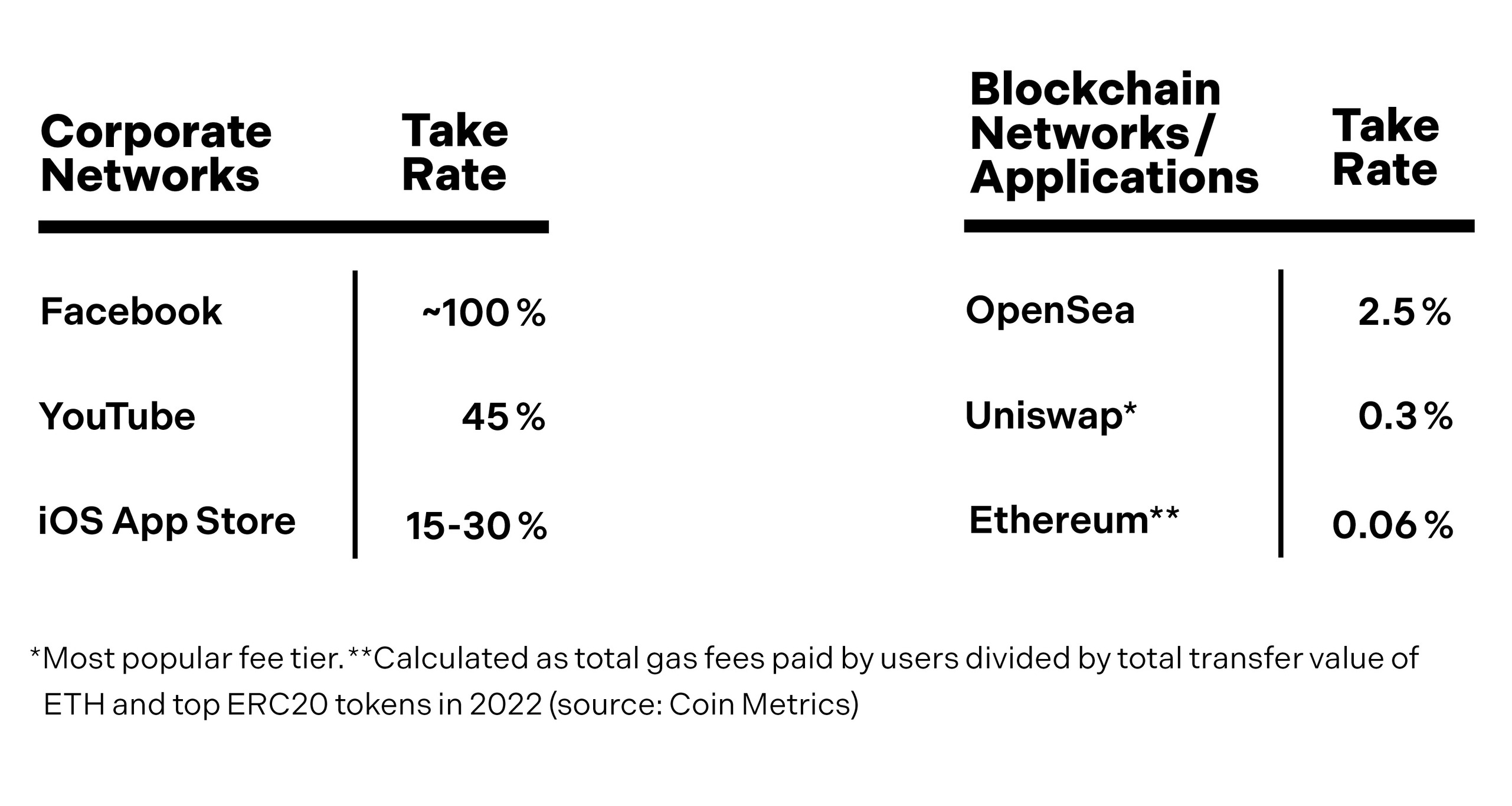

- Blockchain networks disrupt rent-seeking intermediaries by maintaining significantly lower take rates, often ranging from less than 1 percent to 2.5 percent.

- The low fees of blockchain networks are secured by code-enforced commitments and community control, preventing the arbitrary rule changes common in corporate networks.

Where bean counters see fat margins, entrepreneurs should see blood.

Blockchain Networks and Decentralization

- Blockchain networks maintain low take rates through code-enforced commitments and the community's power to vote on changes.

- The open-source nature of blockchain allows for 'forking,' providing a constant competitive pressure that keeps costs close to maintenance levels.

- A significant risk of recentralization exists if users gravitate toward high-convenience, corporate-owned front-ends that re-introduce pricing power.

- Successful decentralized networks must fund high-quality user experiences to prevent the fate of protocols like RSS, which lacked sustainable funding.

- By ensuring users own their digital identities and goods, blockchains enable a credible threat of switching that prevents application-level lock-in.

Applications are unable to acquire pricing leverage if users can easily switch from one application to another.

Blockchain Ownership and Profit Shifts

- Blockchain-based ownership of digital identity and goods reduces platform lock-in by making it easy for users to switch services at any time.

- The competition between NFT marketplaces like OpenSea and Blur demonstrates that blockchain interoperability compels lower take rates, a trend rarely seen in corporate networks.

- Low take rates and fixed protocol rules provide a stable environment for developers, who often fear being undermined by centralized corporate intermediaries.

- According to the law of conservation of attractive profits, commoditizing one layer of a tech stack shifts the profit potential to other layers, much like squeezing a balloon.

The theory is that commoditizing a layer in a tech stack is like squeezing a balloon.

Conserving Attractive Profits

- The 'law of conservation of attractive profits' suggests that when one layer of a tech stack is commoditized, profits shift to other layers rather than disappearing.

- Companies use a 'commoditize your complement' strategy to ensure their primary revenue sources remain unblocked by gatekeepers in other layers.

- Google created products like Android and Chrome as a calculated move to reduce platform risk and prevent competitors from capturing search revenue.

- Apple's ability to charge Google billions to be the default search engine on Safari illustrates the zero-sum nature of profit capture within a stack.

- Intel's support for open-source Linux follows the same logic, reducing Microsoft's influence to ensure hardware sales remain profitable.

The overall profits are conserved but shift from layer to layer .

Thick vs. Thin Networks

- Corporate networks function as thick layers that centralize profits, squeezing value away from the creators and developers who build on top of them.

- Blockchain and protocol networks are designed as thin layers, allowing value to flow outward to the edges where users and developers reside.

- The author argues that social networks should function like roads—basic, reliable utilities that facilitate a thick layer of innovation around them.

- The current corporate model forces startups to build entirely new proprietary infrastructures rather than innovating on top of open, interoperable protocols.

- The historical success of the internet is credited to the thin nature of HTTP, which allowed for decades of explosive innovation at the application level.

Network effects that result in lock-in force creators to work for free and developers to behave as they are told.

Tokens vs Corporate Take Rates

- Centralized social and financial networks act as thick layers that capture excessive value and stifle innovation by forcing startups to build proprietary infrastructure.

- Blockchain technology reshapes this economic model by creating thin layers, which reduces costs in sectors like payments and lending while empowering creators.

- Historical protocols like email flourished because they were ignored by corporations, but modern decentralized projects face intense competition for developer talent.

- Unlike traditional protocols that rely on volunteers, blockchain networks use token incentives as a sustainable mechanism to fund software development and attract top-tier talent.

- Token incentives serve as a 'carrot' to balance the 'stick' of high take rates, making decentralized networks competitive with corporate compensation models.

The Net grew like a weed between the cracks in the monolithic steel-and-glass empire of traditional commerce.

Token-Driven Network Development

- Blockchain networks utilize native tokens as a built-in mechanism to compensate developers, distinguishing them from protocol networks that rely on volunteers.

- By offering tokens that represent ownership and governance rights, these networks transform external contributors into invested stakeholders.

- The transition from corporate models to blockchain models shifts internal software development to an open, market-based system of external tasks.

- Token incentives foster global competition, allowing users to choose from a variety of software options rather than being limited to a single corporate provider.

- As networks mature and launch, original developers relinquish control to ensure the platform remains permissionless and treats all participants equally.

Jobs held captive in corporate networks become external, market-based tasks in blockchain networks.

Incentivizing Network Growth

- Blockchain networks utilize decentralized token grants to fund development, ensuring that no single app developer holds privilege over others.

- Corporate networks typically centralize wealth among a few founders and investors, often leaving the early contributors who built the platform's value behind.

- By granting tokens to early users, blockchain networks provide a level playing field to compete with the massive capital of corporate software development.

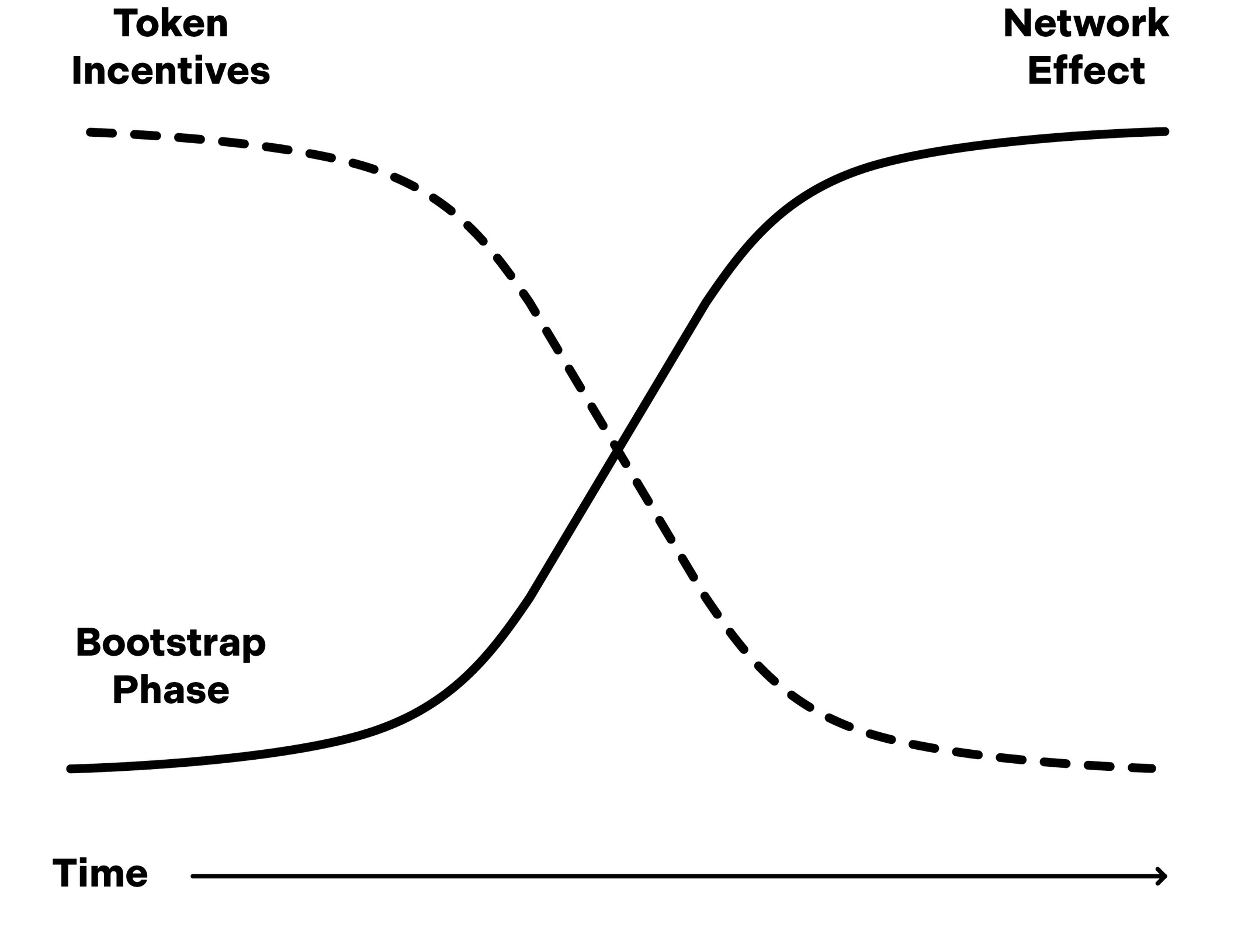

- This inclusive model solves the 'cold start' problem by rewarding early risk-takers who contribute to the network before its intrinsic value is established.

- As a network achieves scale and its effects become self-sustaining, token incentives naturally decrease in necessity.

Just look at the video creators who built YouTube, the social groups who built Facebook, the influencers who built Instagram, the homeowners who built Airbnb, the drivers who built Uber—the list goes on.

Solving the Bootstrap Problem

- Building networks is difficult due to the 'bootstrap' problem, where a lack of early participants makes the service initially useless.

- While corporations once used financial subsidies to grow, token incentives now offer a decentralized way to attract early adopters.

- The Helium project demonstrated that tokens can build complex physical infrastructure, like a nationwide telecom network, through grassroots participation.

- By rewarding early contributors with tokens, new projects can overcome the 'rich-get-richer' dynamic of centralized corporate platforms.

- This token-led growth model is being applied to diverse fields including artificial intelligence, computer storage, and green energy infrastructure.

Network effects cut both ways: they can accelerate growth, but they can also handicap it.

Tokens as Self-Marketing

- The mobile app landscape is currently dominated by decade-old incumbents, making it increasingly difficult for new startups to break into established user routines.

- Startups are often forced to pay Big Tech gatekeepers for advertising, leading to high acquisition costs that frequently result in negative profit margins.

- Tokens offer an alternative growth strategy by transforming users into stakeholders who are financially and emotionally motivated to evangelize the network.

- This ownership model facilitates authentic peer-to-peer marketing through community activities like blogging, coding, and organizing meetups.

- Major blockchain networks such as Bitcoin and Ethereum have achieved massive scale without traditional marketing budgets by relying on these organic viral loops.

They sing praises and shout from the desktops.

Tokens and Community Ownership

- Blockchain networks leverage tokens to drive grassroots evangelism, often achieving massive scale without traditional advertising budgets.

- The text compares token holders to homeowners who are incentivized to build and promote their cities because they have a financial stake and a say in governance.

- Dogecoin serves as a primary case study, demonstrating how a parody project can maintain a multi-billion dollar valuation through community passion alone.

- Unlike corporate networks that capture all value, token-based systems allow users to share in the upside and control of the platforms they help build.

- While memecoins can be speculative or risky, their longevity highlights the powerful psychological and economic effect of making users owners.

To its users, Dogecoin may be a silly network, but at least it’s their silly network.

The Rise of User-Ownership

- Memecoins like Dogecoin demonstrate that ownership creates powerful, lasting community engagement that traditional corporate networks often lack.

- Decentralized exchanges like Uniswap have pioneered large-scale token distributions, granting early users significant financial upside and governance rights.

- While corporate giants like Facebook and YouTube profit from user-generated content, they typically exclude those users from participating in the network's financial success.

- Blockchain networks fundamentally shift the ownership paradigm by distributing the majority of tokens to the community based on their contributions.

- Despite minor efforts by companies like Airbnb and Uber to offer equity, their programs represent only a fraction of the ownership scale seen in blockchain models.

And yet in most corporate networks, users are treated as second-class citizens at best, or as a product to be served up to real customers, like advertisers, at worst.

Tokenomics and Community Ownership

- Ownership in blockchain networks is broadly distributed to contributors via incentives, whereas corporate networks remain centralized.

- Tokens act as a mechanism to fulfill the original internet's decentralized vision, offering users commitments and open APIs that corporations lack.

- Tokenomics integrates traditional economic concepts with internet protocols to design sustainable incentive systems for blockchain participants.

- The development of blockchain economies is heavily influenced by video games like Eve Online, which features complex monetary policies and professional oversight.

- Sustainable network growth is achieved by carefully balancing the supply and demand of native tokens to maintain value and attract users.

While memecoin mutations, like Dogecoin, may seem like a joke, they show how users are embracing all sorts of tokens—some silly, some serious—in search of community, to fill the void left by corporate networks.

Balancing Blockchain Economies

- Blockchain networks utilize tokenomic designs inspired by video game economies to balance supply and demand.

- The metaphor of 'faucets' and 'sinks' helps designers visualize how tokens flow into and out of the network's ecosystem.

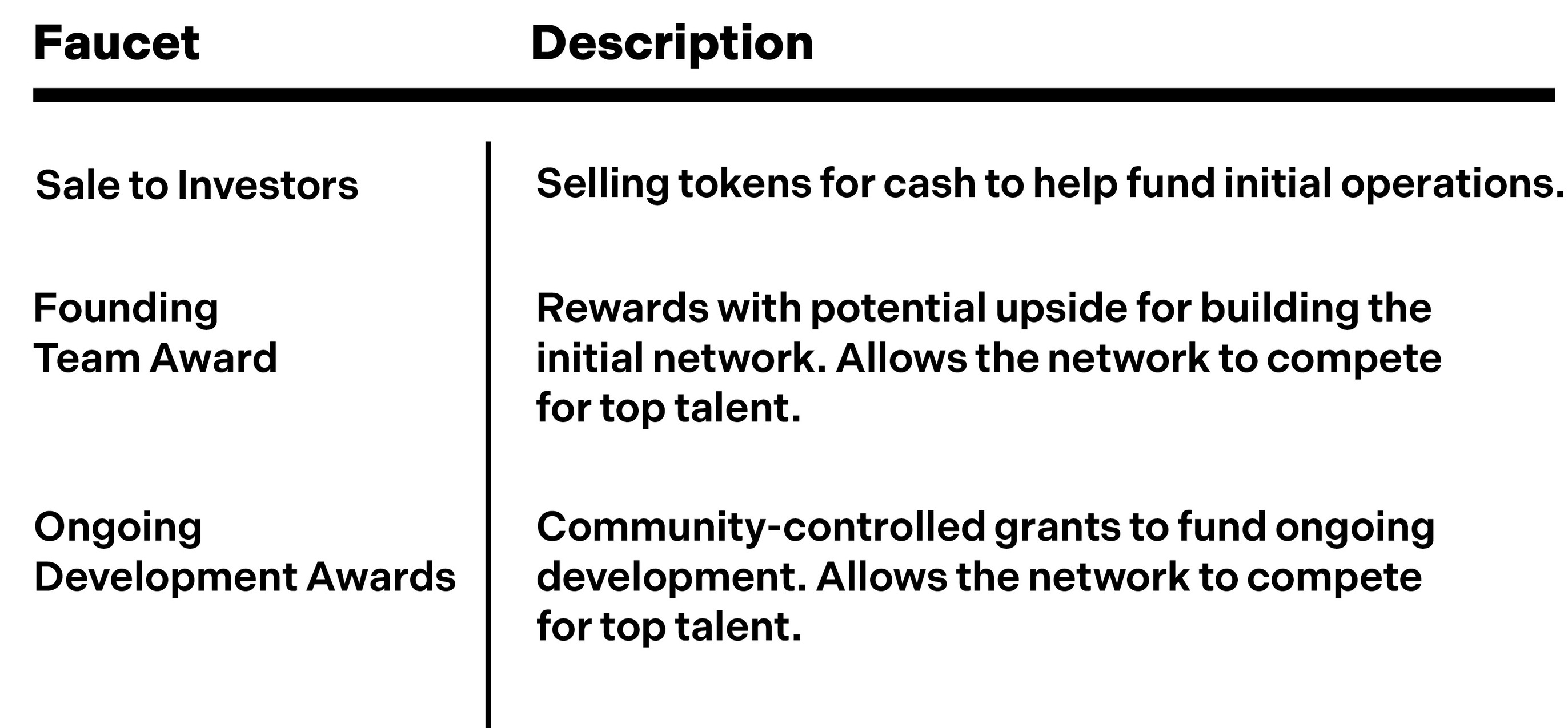

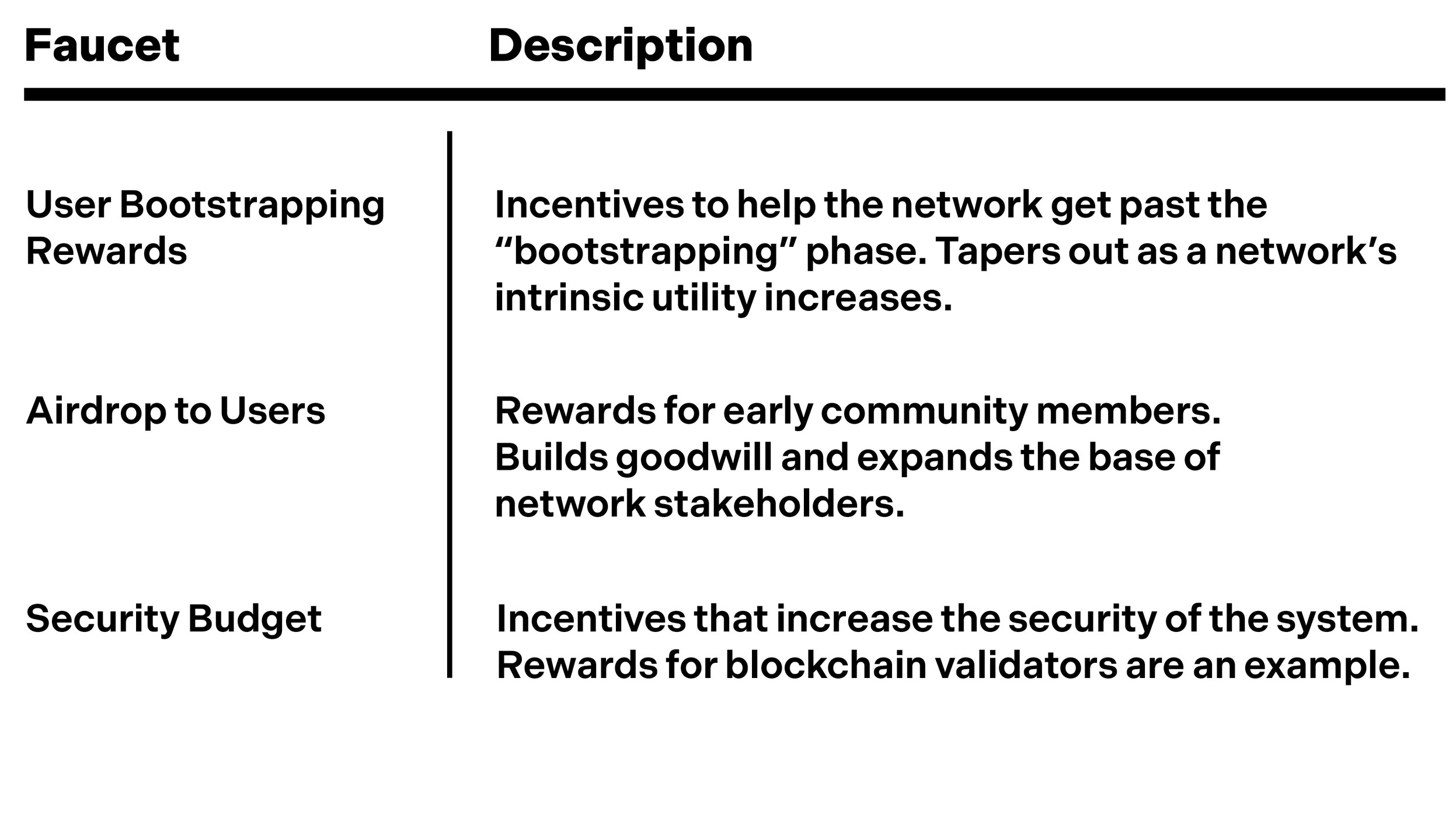

- Faucets serve as powerful incentives, similar to land grants, to attract developers and overcome the initial bootstrap problem.

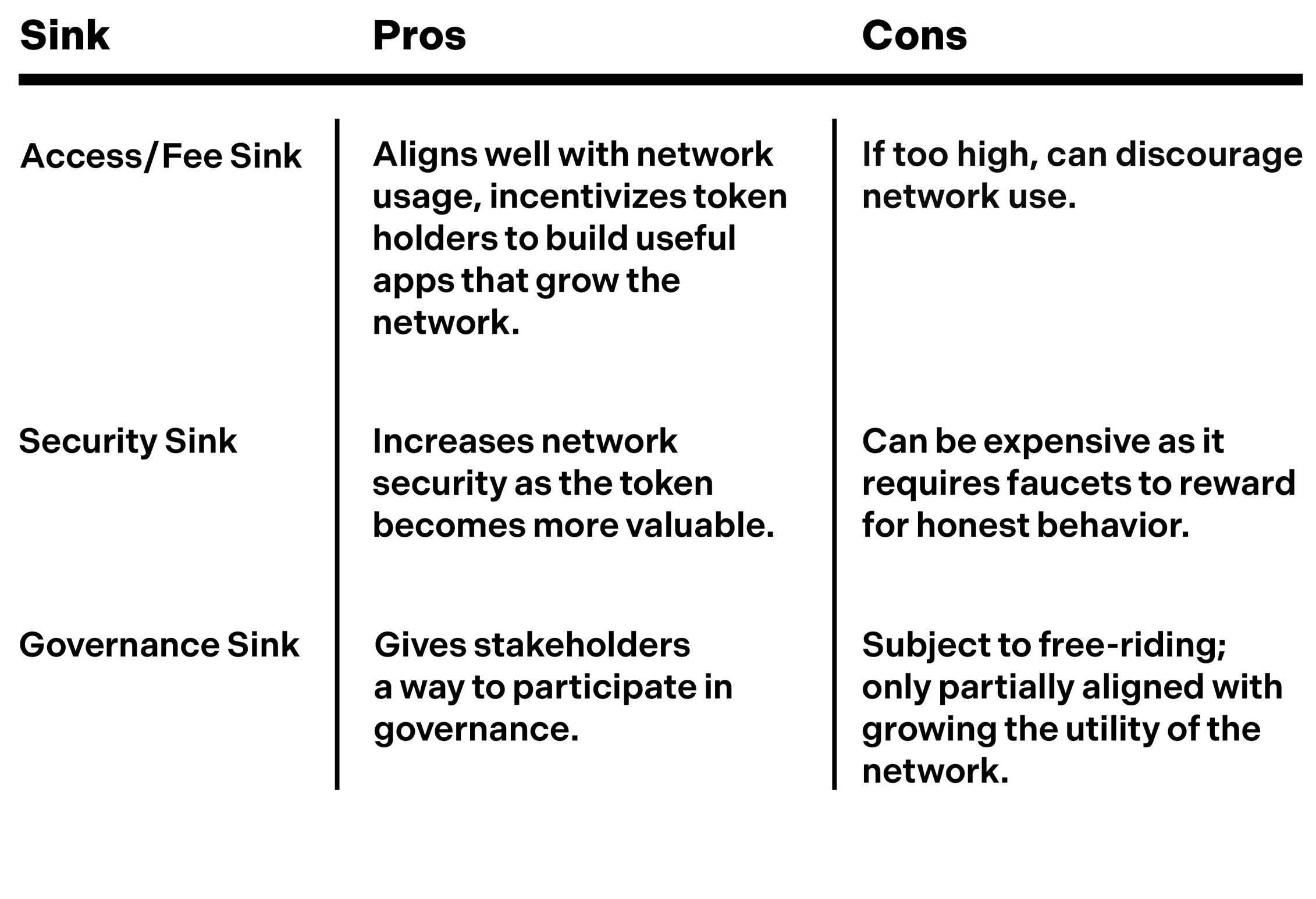

- Sinks, such as access fees or token burning, align a token's price with the actual usage and popularity of the network.

- Ethereum uses 'gas' fees to manage compute demand, burning a portion of these tokens to reduce supply and potentially increase value.

A common metaphor for thinking about the design of token economies is to imagine tokens as water that flows through the plumbing of a house.

Token Economics and Sinks

- Access sinks, such as Ethereum's 'gas' fees, reduce token supply by burning a portion of transaction costs, which can theoretically increase the price of the native token.

- Security sinks reward users for 'staking' or locking up tokens to validate the network, creating a balance between network security and potential inflation from reward faucets.

- Governance sinks attempt to drive token demand by granting users voting power over network changes, though they often struggle with the free-rider problem of voter apathy.

- Effective economic designs link sinks to network usage, creating a virtuous cycle where increased activity drains the token supply and funds further development.

- The health of a blockchain community is often reflected in its discussions, where an obsession with token price indicates a 'casino culture' rather than a focus on technology.

Paying excessive attention to prices is a bad sign—a hallmark of casino culture.

Valuing Token Economies

- Token design determines whether a community becomes a speculative 'casino' or a constructive hub for technological improvement.

- Critics often dismiss blockchain by focusing on the worst actors, ignoring historical precedents like the skepticism faced by early railroads and the internet.

- The inherent flexibility of software allows for any imaginable economic model to be encoded, enabling sustainable supply and demand structures.

- Ethereum demonstrates healthy tokenomics by using transaction fees to burn tokens, creating a system analogous to corporate cash flow.

- By analyzing transparent 'faucets' and 'sinks,' investors can value blockchain networks using traditional metrics such as price-to-earnings ratios.

The railroad wasn’t worthless just because many unviable railroad companies fed early stock market mania.

Valuing Tokens and Market Cycles

- Blockchain tokens can be evaluated using standard financial metrics, such as price-to-earnings ratios and cash flow analysis.

- The value of a network token relies on its economic design and whether its 'faucets and sinks' successfully convert popularity into sustained demand.

- Comparing blockchain networks to real estate illustrates how access fees generate a fundamental value similar to rental property income.

- Technological revolutions typically follow a predictable cycle involving an initial speculative frenzy, a market crash, and a subsequent deployment phase.

- While skeptics may doubt specific platforms, tokens are best understood as functional assets for virtual economies rather than speculative 'magic beans'.

Tokens are not magic beans. They are assets used to power virtual economies, and they can be valued using traditional financial methods.

The Price-Innovation Cycle

- The hype cycle framework illustrates how new technologies transition from financial bubbles and disillusionment into periods of sustainable productive growth.

- Blockchain networks experience intense speculative cycles because their core innovation—digital ownership—inherently enables trading and market activity.

- The 'price-innovation cycle' suggests that market peaks attract builders who remain in the industry after a crash, incubating the next wave of advancement.

- Historical precedents like the dot-com boom demonstrate that speculative manias provide the capital necessary to build the infrastructure for future technological phases.

- Speculation tends to subside as investors learn to value new technologies based on fundamental principles rather than pure excitement.

Any skeptic who dismissed dot-coms as magic beans would have missed out on the successes of Google, Amazon, and others.

Investment and Digital Governance

- Major technological shifts, from railroads to blockchains, require massive capital inflows to build the infrastructure necessary for widespread adoption.

- Blockchain markets are expected to move from speculative popularity to long-term stability driven by fundamental supply and demand.

- Internet protocols operate as a bottom-up democracy where developers and users effectively "vote" on standards through their participation.

- Global internet governance is managed by a patchwork of nonprofit organizations that rely on consensus and recommendations rather than government-led edicts.

To quote an old Wall Street adage attributed to Benjamin Graham, the father of value investing: markets are a voting machine in the short term and a weighing machine in the long term.

Protocol Governance vs. Corporate Control

- Internet governance bodies prioritize consensus and recommendations over formal edicts, fostering a collaborative dialogue between diverse stakeholders.

- Regulation focuses on the behavior of people and applications rather than the underlying protocols, ensuring the core technology remains neutral and flexible.

- Corporate networks are described as dictatorships where management holds absolute power to make unilateral, often opaque decisions at the expense of users.

- Recent shifts in platform ownership highlight the risks of centralized control, where the livelihoods of creators depend on the changing views of whoever owns the company.

We reject: kings, presidents, and voting. We believe in: rough consensus and running code.

Governing Digital Networks

- There is a growing consensus that critical internet networks should not be controlled by the changing whims of individual owners or corporate leadership.