Series 65 Study Guide

Overview unavailable.

Series 65 Examination Overview

- Provides background information on the Uniform Investment Adviser Law Examination structure and procedures.

- Details the role of NASAA and its associated model acts, rules, and policy statements.

- Outlines test specifications covering economic factors, business information, and investment vehicle characteristics.

- Includes sections on client investment strategies and legal regulations regarding unethical business practices.

Series 65 Examination Overview

- The Series 65 examination is a standardized test developed by NASAA to establish professional competency for investment adviser representatives.

- Successful completion of the exam or holding specific professional designations is typically a mandatory prerequisite for state licensure.

- The curriculum evaluates a candidate's grasp of general finance, economics, and investing principles alongside federal and state legal frameworks.

- Test questions are derived from major federal acts like the Investment Advisers Act of 1940 and specific state-level model rules and policies.

- While the exam covers a vast range of legal precedents, it specifically tests the 1956 version of the Uniform Securities Act rather than the 2002 version.

The Uniform Securities Act of 1956 was developed by the Uniform Law Commission. Since its original publication, NASAA has added its own amendments and commentary to the 1956 Act.

Series 65 Examination Mechanics

- The Series 65 examination is a criterion-based minimum competency test consisting of 140 multiple-choice questions administered over 180 minutes.

- Only 130 questions contribute to the final score, while 10 unscored pre-test questions are embedded to validate future examination material.

- A passing score requires 92 correct answers out of the 130 scored items to demonstrate professional competency as an investment adviser representative.

- To ensure integrity, a test development algorithm assembles unique examinations for each candidate based on specific difficulty and content parameters.

- NASAA maintains strict copyright over all test materials and prohibits any unauthorized reproduction or disclosure of specific examination questions.

Two individuals taking the Series 65 examination at the same time therefore will have different sets of test questions.

Series 65 Examination Protocols

- The Series 65 is a closed-book examination administered by FINRA with strict security measures enforced by NASAA.

- Candidates can register through an employer via Form U4 or independently through FINRA's Test Enrollment Services System.

- Upon registration, a 120-day testing window is opened for the candidate to schedule and complete their exam.

- Failing the exam triggers mandatory waiting periods, which escalate to 180 days after the third unsuccessful attempt.

- Passing the exam is only one component of the registration process and does not automatically grant the right to conduct securities business.

NASAA reserves the right to take appropriate action against any person who compromises or attempts to compromise the examination, either in whole or in part.

NASAA and Series 65 Specifications

- Passing the Series 65 examination does not automatically grant the right to conduct securities business without meeting specific state licensing requirements.

- The North American Securities Administrators Association (NASAA) is a non-profit organization that has protected investors for over a century.

- NASAA develops model acts and rules that only gain legal force once they are officially adopted by individual state jurisdictions.

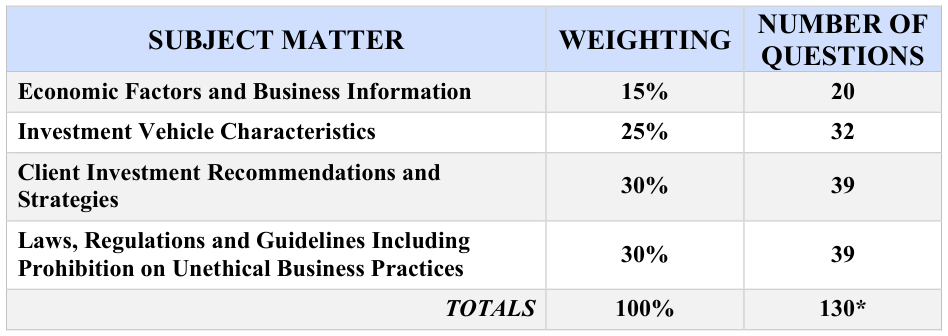

- The Series 65 exam consists of 130 scored questions covering economic factors, investment vehicles, client strategies, and legal regulations.

- The exam is heavily weighted toward laws, regulations, and ethical practices, which comprise 30% of the total score.

NASAA’s model acts, model rules and statements of policy thus do not have legal force or effect standing on their own.

Series 65 Exam Structure

- The Series 65 examination consists of 140 total questions, though only 130 are scored toward the candidate's final result.

- The exam is weighted heavily toward laws, regulations, and client strategies, which together comprise 60% of the scored content.

- Candidates are expected to understand legal principles and concepts even when a question does not explicitly name a specific rule or statute.

- The 'Economic Factors' section covers a broad range of topics including global geopolitics, financial reporting, and complex analytical methods like net present value.

- NASAA maintains a strict neutrality by not endorsing any specific third-party study materials or preparation services.

Candidates thus are expected to know the concepts and legal principles enumerated below without necessarily being prompted as to which concept or principle is being tested.

Series 65 Investment Vehicles

- The Series 65 examination dedicates 25% of its content to the specific features and characteristics of various investment vehicles.

- A wide array of securities is covered, ranging from traditional cash equivalents and fixed income to complex derivatives and alternative investments.

- The curriculum includes detailed valuation methods for equity, such as technical and fundamental analysis alongside discounted cash flow models.

- Pooled investments like mutual funds, ETFs, and REITs are analyzed based on their fee structures, share classes, and liquidity profiles.

- The text outlines the transition into client recommendations, which accounts for 30% of the exam and focuses on different business and individual entities.

Thirty-two questions in every Series 65 examination (25%) will test features or characteristics or various types of investment vehicles.

Series 65 Investment Strategies

- The Series 65 examination devotes thirty percent of its content to client investment recommendations and strategies.

- Candidates must understand diverse client profiles, ranging from individual natural persons to complex business entities and charities.

- The curriculum covers advanced portfolio management techniques including sector rotation, dollar-cost averaging, and high frequency trading.

- A significant portion of the exam focuses on the legal and ethical standards governing investment advisers and their professional conduct.

- The syllabus includes detailed knowledge of tax considerations, retirement plans, and estate planning techniques like trusts and wills.

Techniques ( e.g., diversification, sector rotation, dollar -cost averaging, puts, calls, leveraging, volatility management , inverse strategies, high frequency trading )

Series 65 Professional Conduct Standards

- The Series 65 examination dedicates 30% of its content to laws, regulations, and the prohibition of unethical business practices.

- Candidates must master the specific definitions and registration requirements for investment advisers, representatives, broker-dealers, and agents.

- The curriculum covers the legal framework for securities registration, including federal exemptions and state-level antifraud authority.

- A significant portion of the exam focuses on communication standards, including social media usage and unlawful representations regarding registration.

- Ethical practices and fiduciary obligations are strictly tested, specifically regarding client fund custody, compensation structures, and 'pay to play' rules.

Thirty-nine questions in every Series 65 examination (30%) will test standards for professional conduct by investment advisers and investment adviser representatives.

Investment Adviser Regulatory Framework

- The text outlines rigorous compensation standards including performance-based fees, soft dollars, and 'pay to play' disclosures.

- Strict protocols govern the handling of client funds, securities custody, and the legal obligations of prudent investor standards.

- Extensive ethical guidelines address conflicts of interest, market manipulation, and the protection of vulnerable adults from financial exploitation.

- Operational resilience is mandated through cybersecurity regulations, data privacy protections, and formal business continuity plans.

- The document serves as a comprehensive syllabus for the Uniform Investment Adviser Law Examination, emphasizing the complexity of the subject matter.

This document is intended to be an overview of the Uniform Investment Adviser Law Examination, which will contain specific and challenging questions in these subjects.

Series 65 Examination Overview

The Uniform Securities Act of 1956 was developed by the Uniform Law Commission. Since its original publication, NASAA has added its own amendments and commentary to the 1956 Act.

Investment Adviser Regulatory Framework

- Ethical guidelines address conflicts of interest, market manipulation, and protecting vulnerable adults from financial exploitation.

- Operational resilience is covered through cybersecurity rules, data privacy protections, and business continuity plans.

This document is intended to be an overview of the Uniform Investment Adviser Law Examination, which will contain specific and challenging questions in these subjects.